Advertisement

- United States

- /

- Insurance

- /

- NasdaqGS:ERIE

The recent US$273m market cap decrease is likely to have disappointed insiders invested in Erie Indemnity Company (NASDAQ:ERIE)

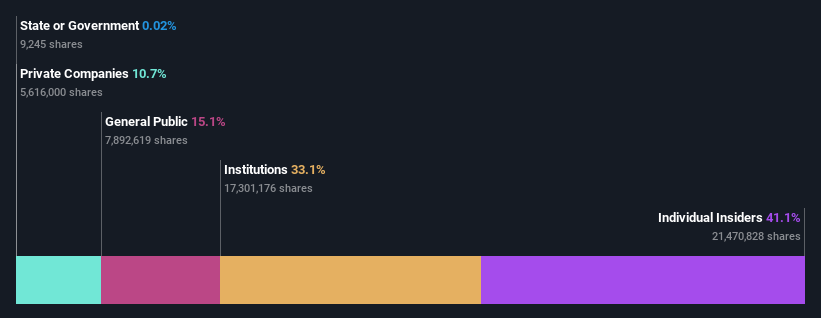

To get a sense of who is truly in control of Erie Indemnity Company (NASDAQ:ERIE), it is important to understand the ownership structure of the business. We can see that individual insiders own the lion's share in the company with 41% ownership. In other words, the group stands to gain the most (or lose the most) from their investment into the company.

As a result, insiders as a group endured the highest losses after market cap fell by US$273m.

Let's delve deeper into each type of owner of Erie Indemnity, beginning with the chart below.

View our latest analysis for Erie Indemnity

What Does The Institutional Ownership Tell Us About Erie Indemnity?

Many institutions measure their performance against an index that approximates the local market. So they usually pay more attention to companies that are included in major indices.

We can see that Erie Indemnity does have institutional investors; and they hold a good portion of the company's stock. This suggests some credibility amongst professional investors. But we can't rely on that fact alone since institutions make bad investments sometimes, just like everyone does. It is not uncommon to see a big share price drop if two large institutional investors try to sell out of a stock at the same time. So it is worth checking the past earnings trajectory of Erie Indemnity, (below). Of course, keep in mind that there are other factors to consider, too.

We note that hedge funds don't have a meaningful investment in Erie Indemnity. The company's largest shareholder is Thomas Hagen, with ownership of 33%. Meanwhile, the second and third largest shareholders, hold 11% and 9.4%, of the shares outstanding, respectively.

A more detailed study of the shareholder registry showed us that 3 of the top shareholders have a considerable amount of ownership in the company, via their 53% stake.

While it makes sense to study institutional ownership data for a company, it also makes sense to study analyst sentiments to know which way the wind is blowing. There is a little analyst coverage of the stock, but not much. So there is room for it to gain more coverage.

Insider Ownership Of Erie Indemnity

The definition of company insiders can be subjective and does vary between jurisdictions. Our data reflects individual insiders, capturing board members at the very least. Company management run the business, but the CEO will answer to the board, even if he or she is a member of it.

I generally consider insider ownership to be a good thing. However, on some occasions it makes it more difficult for other shareholders to hold the board accountable for decisions.

Our most recent data indicates that insiders own a reasonable proportion of Erie Indemnity Company. Insiders own US$3.1b worth of shares in the US$7.6b company. That's quite meaningful. Most would be pleased to see the board is investing alongside them. You may wish to access this free chart showing recent trading by insiders.

General Public Ownership

The general public-- including retail investors -- own 15% stake in the company, and hence can't easily be ignored. While this group can't necessarily call the shots, it can certainly have a real influence on how the company is run.

Private Company Ownership

It seems that Private Companies own 11%, of the Erie Indemnity stock. Private companies may be related parties. Sometimes insiders have an interest in a public company through a holding in a private company, rather than in their own capacity as an individual. While it's hard to draw any broad stroke conclusions, it is worth noting as an area for further research.

Next Steps:

I find it very interesting to look at who exactly owns a company. But to truly gain insight, we need to consider other information, too. For instance, we've identified 2 warning signs for Erie Indemnity that you should be aware of.

But ultimately it is the future, not the past, that will determine how well the owners of this business will do. Therefore we think it advisable to take a look at this free report showing whether analysts are predicting a brighter future.

NB: Figures in this article are calculated using data from the last twelve months, which refer to the 12-month period ending on the last date of the month the financial statement is dated. This may not be consistent with full year annual report figures.

Valuation is complex, but we're here to simplify it.

Discover if Erie Indemnity might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:ERIE

Erie Indemnity

Operates as a managing attorney-in-fact for the subscribers at the Erie Insurance Exchange in the United States.

Flawless balance sheet established dividend payer.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Giftify ·

Giftify ($GIFT): A Small-Cap Incentives Platform with More ScaleThan Its Valuation Suggests

Fair Value:US$2.550.4% undervalued

9 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

TR

tripledub on Meta Platforms ·

The $135 Billion Bet That Should Make Every Shareholder Nervous

Fair Value:US$58016.3% overvalued

24 followersusers have followed this narrative

3 commentsusers have commented on this narrative

22 likesusers have liked this narrative

TH

TheBestInvestor on Lockheed Martin ·

Orbit + Aero + Defense

Fair Value:US$673.8817.6% undervalued

14 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on Steppe Gold ·

A case for Steppe Gold, bear case CAD $4, base case CAD $15, bull case CAD $25

Fair Value:CA$2594.1% undervalued

19 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

Recently Updated Narratives

DO

Double_Bubbler on EnSilica ·

Why EnSilica is Worth Possibly 13x its Current Price

Fair Value:UK£586.8% undervalued

123 followersusers have followed this narrative

17 commentsusers have commented on this narrative

0 likesusers have liked this narrative

FA

FA_Trader on UUE Holdings Berhad ·

UUE’s latest QR shows a much stronger finish, with quarterly earnings bouncing back sharply

Fair Value:RM 0.8347.6% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

FA

FA_Trader on Systech Bhd ·

Systech: New Managing Director appointment may strengthen execution and sharpen the group’s next phase

Fair Value:RM 0.7272.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TR

tripledub on Microsoft ·

Everyone's Terrified Microsoft Will Keep Spending. I'm Terrified They'll Stop.

Fair Value:US$3959.6% overvalued

52 followersusers have followed this narrative

3 commentsusers have commented on this narrative

43 likesusers have liked this narrative

KI

Kingman1152 on NVIDIA ·

NVIDIA will see a profit margin surge of 55% in the next 5 years

Fair Value:US$305.233.7% undervalued

64 followersusers have followed this narrative

1 commentusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$579.5725.3% undervalued

1383 followersusers have followed this narrative

2 commentsusers have commented on this narrative

11 likesusers have liked this narrative

Trending Discussion

TA

Taurustunez88 on Dangote Sugar Refinery ·

With the N500b rights issue, I believe Dangote sugar refinery’s loss due to FX pressures will be dra...

1

|0