Advertisement

- United States

- /

- Personal Products

- /

- OTCPK:REVR.Q

Revlon (NYSE:REV) Will Be Looking To Turn Around Its Returns

When we're researching a company, it's sometimes hard to find the warning signs, but there are some financial metrics that can help spot trouble early. Businesses in decline often have two underlying trends, firstly, a declining return on capital employed (ROCE) and a declining base of capital employed. This combination can tell you that not only is the company investing less, it's earning less on what it does invest. And from a first read, things don't look too good at Revlon (NYSE:REV), so let's see why.

Understanding Return On Capital Employed (ROCE)

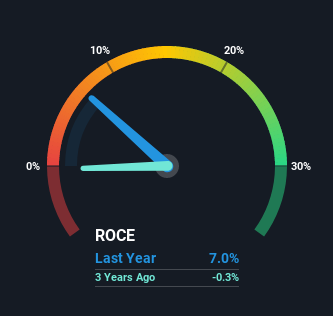

For those who don't know, ROCE is a measure of a company's yearly pre-tax profit (its return), relative to the capital employed in the business. Analysts use this formula to calculate it for Revlon:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.07 = US$115m ÷ (US$2.4b - US$811m) (Based on the trailing twelve months to September 2021).

Thus, Revlon has an ROCE of 7.0%. Ultimately, that's a low return and it under-performs the Personal Products industry average of 20%.

Check out our latest analysis for Revlon

In the above chart we have measured Revlon's prior ROCE against its prior performance, but the future is arguably more important. If you're interested, you can view the analysts predictions in our free report on analyst forecasts for the company.

So How Is Revlon's ROCE Trending?

The trend of returns that Revlon is generating are raising some concerns. To be more specific, today's ROCE was 12% five years ago but has since fallen to 7.0%. In addition to that, Revlon is now employing 31% less capital than it was five years ago. The fact that both are shrinking is an indication that the business is going through some tough times. Typically businesses that exhibit these characteristics aren't the ones that tend to multiply over the long term, because statistically speaking, they've already gone through the growth phase of their life cycle.

The Key Takeaway

In summary, it's unfortunate that Revlon is shrinking its capital base and also generating lower returns. Investors haven't taken kindly to these developments, since the stock has declined 70% from where it was five years ago. That being the case, unless the underlying trends revert to a more positive trajectory, we'd consider looking elsewhere.

If you want to know some of the risks facing Revlon we've found 3 warning signs (1 is potentially serious!) that you should be aware of before investing here.

While Revlon may not currently earn the highest returns, we've compiled a list of companies that currently earn more than 25% return on equity. Check out this free list here.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OTCPK:REVR.Q

Revlon

Revlon, Inc. develops, manufactures, markets, distributes, and sells beauty and personal care products worldwide.

Slightly overvalued with weak fundamentals.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor