- United States

- /

- Auto

- /

- NasdaqGS:LI

Top 3 US Growth Companies With High Insider Ownership

Reviewed by Simply Wall St

As U.S. stocks wrapped up a volatile August with gains across major indexes, investor sentiment has been buoyed by easing inflation and the prospect of interest rate cuts from the Federal Reserve. In this environment, companies with strong growth potential and high insider ownership can be particularly appealing to investors, as they often signal confidence from those who know the business best.

Top 10 Growth Companies With High Insider Ownership In The United States

| Name | Insider Ownership | Earnings Growth |

| Atlas Energy Solutions (NYSE:AESI) | 29.1% | 42.1% |

| GigaCloud Technology (NasdaqGM:GCT) | 25.7% | 24.3% |

| Victory Capital Holdings (NasdaqGS:VCTR) | 10.2% | 32.3% |

| Hims & Hers Health (NYSE:HIMS) | 13.7% | 40.7% |

| Super Micro Computer (NasdaqGS:SMCI) | 25.7% | 27.1% |

| On Holding (NYSE:ONON) | 28.4% | 24.4% |

| Credo Technology Group Holding (NasdaqGS:CRDO) | 14.1% | 60.9% |

| BBB Foods (NYSE:TBBB) | 22.9% | 66.5% |

| Carlyle Group (NasdaqGS:CG) | 29.5% | 22% |

| EHang Holdings (NasdaqGM:EH) | 32.8% | 78.8% |

We'll examine a selection from our screener results.

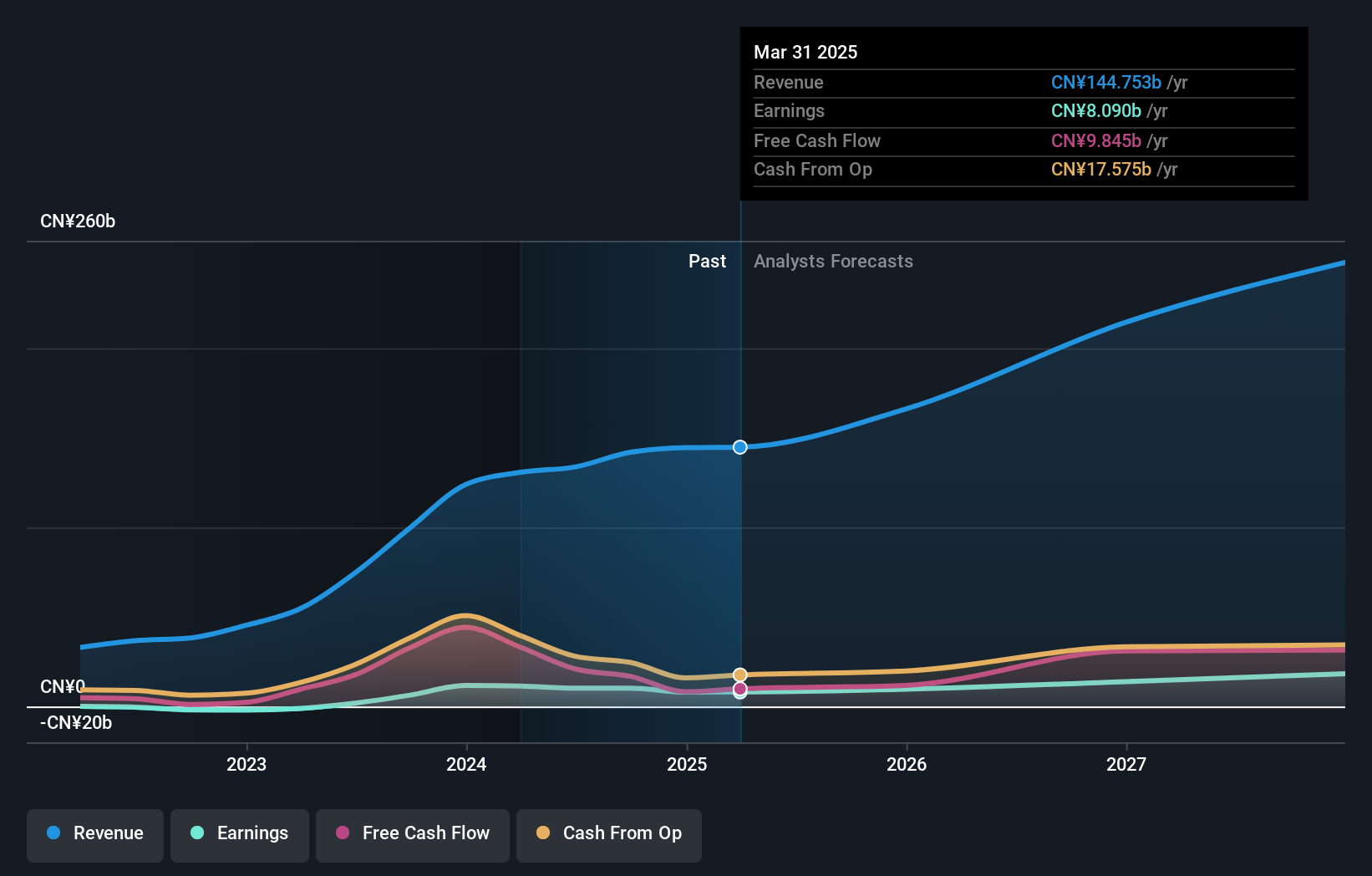

Li Auto (NasdaqGS:LI)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Li Auto Inc. operates in the energy vehicle market in the People’s Republic of China and has a market cap of $20.65 billion.

Operations: The company generates revenue primarily from its auto manufacturing segment, which reported CN¥133.72 billion.

Insider Ownership: 29.3%

Earnings Growth Forecast: 23.3% p.a.

Li Auto, a growth company with high insider ownership, has shown impressive vehicle delivery numbers, reaching 288,103 deliveries in 2024 and projecting strong Q3 revenue between US$5.4 billion and US$5.8 billion. Despite facing legal challenges and a dip in net income for Q2 2024 to CNY 1.10 billion from CNY 2.29 billion last year, the company’s earnings are forecasted to grow significantly at an annual rate of 23.3%.

- Click here to discover the nuances of Li Auto with our detailed analytical future growth report.

- Insights from our recent valuation report point to the potential undervaluation of Li Auto shares in the market.

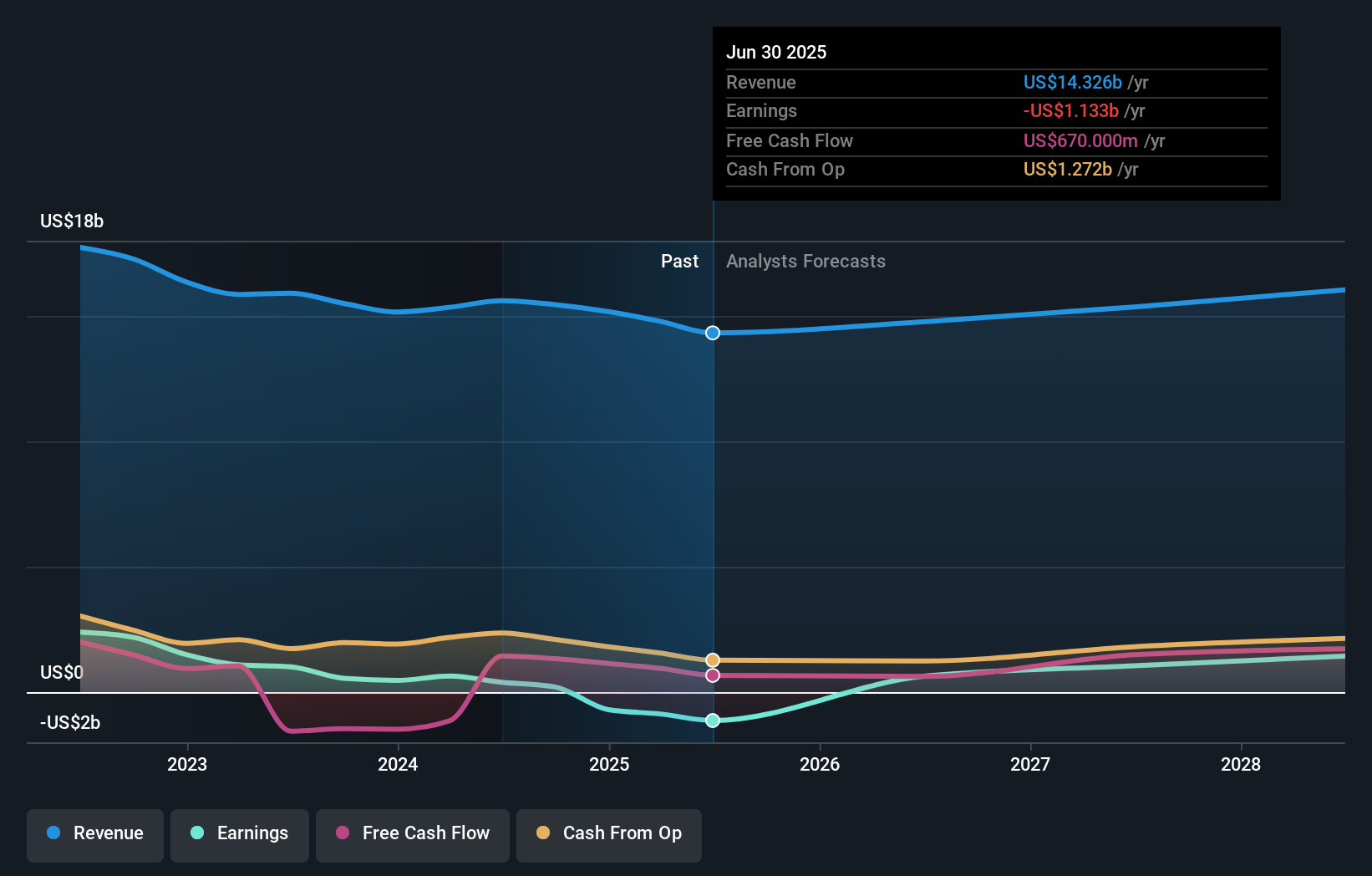

Estée Lauder Companies (NYSE:EL)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: The Estée Lauder Companies Inc. manufactures, markets, and sells skin care, makeup, fragrance, and hair care products worldwide with a market cap of approximately $32.88 billion.

Operations: The company's revenue segments include skin care ($7.91 billion), makeup ($4.47 billion), fragrance ($2.49 billion), and hair care ($629 million).

Insider Ownership: 12.7%

Earnings Growth Forecast: 28.0% p.a.

Estée Lauder Companies, with substantial insider ownership, faces mixed financial performance. Recent earnings reported a drop in net income to US$390 million from US$1.01 billion last year and a decline in basic EPS to US$1.09 from US$2.81. Despite high debt levels and lower profit margins, the company's earnings are forecasted to grow at an annual rate of 28%, outpacing the market average of 15%. The CEO's upcoming retirement adds another layer of uncertainty amid ongoing restructuring efforts.

- Unlock comprehensive insights into our analysis of Estée Lauder Companies stock in this growth report.

- Upon reviewing our latest valuation report, Estée Lauder Companies' share price might be too optimistic.

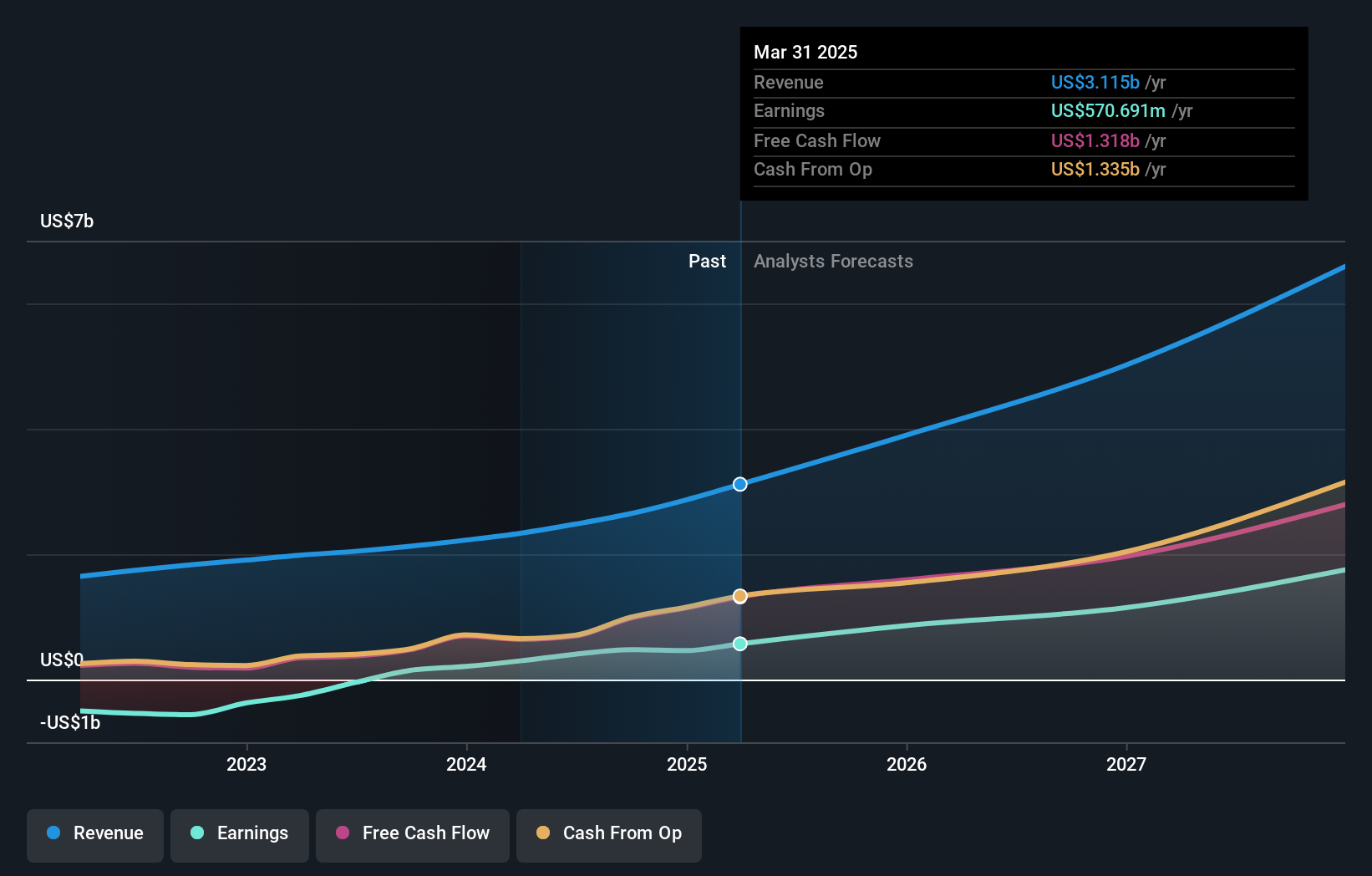

Palantir Technologies (NYSE:PLTR)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Palantir Technologies Inc. develops and implements software platforms for intelligence and counterterrorism operations globally, with a market cap of approximately $70.50 billion.

Operations: Palantir's revenue is derived from two main segments: $1.14 billion from commercial clients and $1.34 billion from government contracts.

Insider Ownership: 13.4%

Earnings Growth Forecast: 22.5% p.a.

Palantir Technologies, with high insider ownership, is experiencing significant growth and strategic partnerships. Its revenue is forecast to grow 16.8% annually, outpacing the US market average of 8.7%. Recent partnerships with Sompo, Surf Air Mobility, and Wendy's QSCC highlight its expanding influence in AI and data integration. Despite a low forecasted return on equity (17.4%) and past shareholder dilution, Palantir remains undervalued by 39.7% against fair value estimates.

- Get an in-depth perspective on Palantir Technologies' performance by reading our analyst estimates report here.

- Our expertly prepared valuation report Palantir Technologies implies its share price may be too high.

Seize The Opportunity

- Click this link to deep-dive into the 178 companies within our Fast Growing US Companies With High Insider Ownership screener.

- Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

- Invest smarter with the free Simply Wall St app providing detailed insights into every stock market around the globe.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:LI

Li Auto

Operates in the energy vehicle market in the People’s Republic of China.

Flawless balance sheet with solid track record.