Honest Company (HNST) shares have been trending lower lately, with a nearly 23% decline over the past 3 months. Investors are watching to see whether recent positive annual net income growth could signal a turnaround in the near future.

Despite the rough patch for Honest Company shares this year, with a steep year-to-date share price return of -47.72%, there are hints of renewed interest as its recent positive net income growth sets a different tone. Looking at the bigger picture, short-term momentum has faded. However, the three-year total shareholder return of 8.23% shows that some long-term investors have still come out ahead.

With Honest Company’s share price hovering well below analyst targets and fundamentals showing signs of life, the question now is whether the market is overlooking a compelling value or if all the upside is already priced in.

Advertisement

Most Popular Narrative: 47.7% Undervalued

The consensus narrative points to Honest Company's fair value being well above its last close. The recent share price drop contrasts this outlook and has sparked a debate on the potential upside.

The company is capitalizing on the accelerating shift towards natural and clean-label products, as seen in strong growth in sensitive skin, fragrance-free, and natural baby personal care items. This positions Honest to benefit from increasing consumer demand and supports future revenue expansion.

Wondering how bullish analysts see Honest's future? Their fair value estimate is based on rapid earnings gains, expanding profit margins, and a future earnings multiple that is uncommon in the sector. Curious how these projections could justify a price nearly double today's? Only the full narrative unpacks the details.

However, a slowdown in diaper category growth and rising tariff costs could present challenges for Honest Company's margin expansion and raise questions about its turnaround narrative.

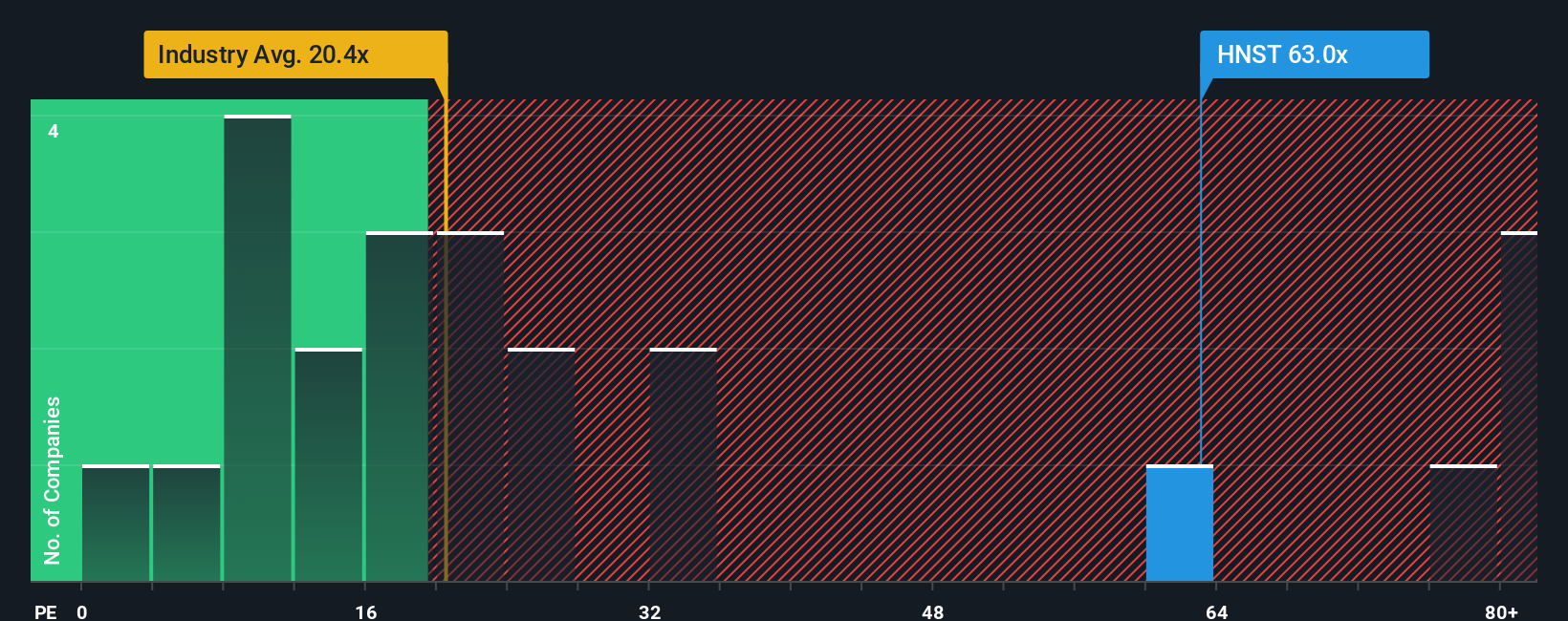

While the consensus narrative points to Honest Company as undervalued, looking through the lens of price-to-earnings paints a much different picture. At 61x, Honest's ratio is much higher than both the industry average (19.8x) and its peer group (11.6x), and well above the fair ratio of 21.2x. This sizable gap suggests investors may be paying a premium, raising the question: could optimism outpace reality if growth falls short?

If you'd rather draw your own conclusions or question the popular sentiment, you can dig into the numbers and shape your own view in minutes with Do it your way.

A great starting point for your Honest Company research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for More Investment Ideas?

Great investing goes beyond one stock. Keep your edge sharp and capitalize on other opportunities that could outperform. These screens consistently surface stocks Wall Street can’t ignore.

Seize the AI revolution’s momentum and pinpoint promising upstarts among these 26 AI penny stocks that are driving the future of intelligent technology.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Honest Company might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.