Advertisement

- United States

- /

- Household Products

- /

- NasdaqGS:CENT

Is Central Garden & Pet a Value Opportunity After 2025 Price Slide and DCF Upside Potential?

Simply Wall St

Reviewed by Bailey Pemberton

- If you have been wondering whether Central Garden & Pet at around $33.63 is quietly turning into a value opportunity or just a value trap, you are not alone.

- The stock is down about 11.8% year to date and 17.6% over the last year, even though it has managed positive annualized returns of roughly 10.5% over 3 years and 13.1% over 5 years, a mix that hints at both recovery potential and shifting risk sentiment.

- Recent headlines have focused on Central Garden & Pet sharpening its portfolio through brand refreshes and distribution wins in its lawn, garden, and pet categories, alongside ongoing efforts to streamline operations and strengthen its balance sheet. Together, these moves help explain why the share price has been volatile as investors reassess how durable its growth and margins might be.

- Despite the choppy performance, our checks suggest the shares look attractive on fundamentals, with a valuation score of 6/6 for being undervalued across all key metrics. In the rest of this article we will unpack those valuation methods, before circling back at the end to an even more powerful way to think about what Central Garden & Pet might really be worth.

Approach 1: Central Garden & Pet Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model estimates what a business is worth today by projecting its future cash flows and then discounting those cash flows back to their value in today’s dollars.

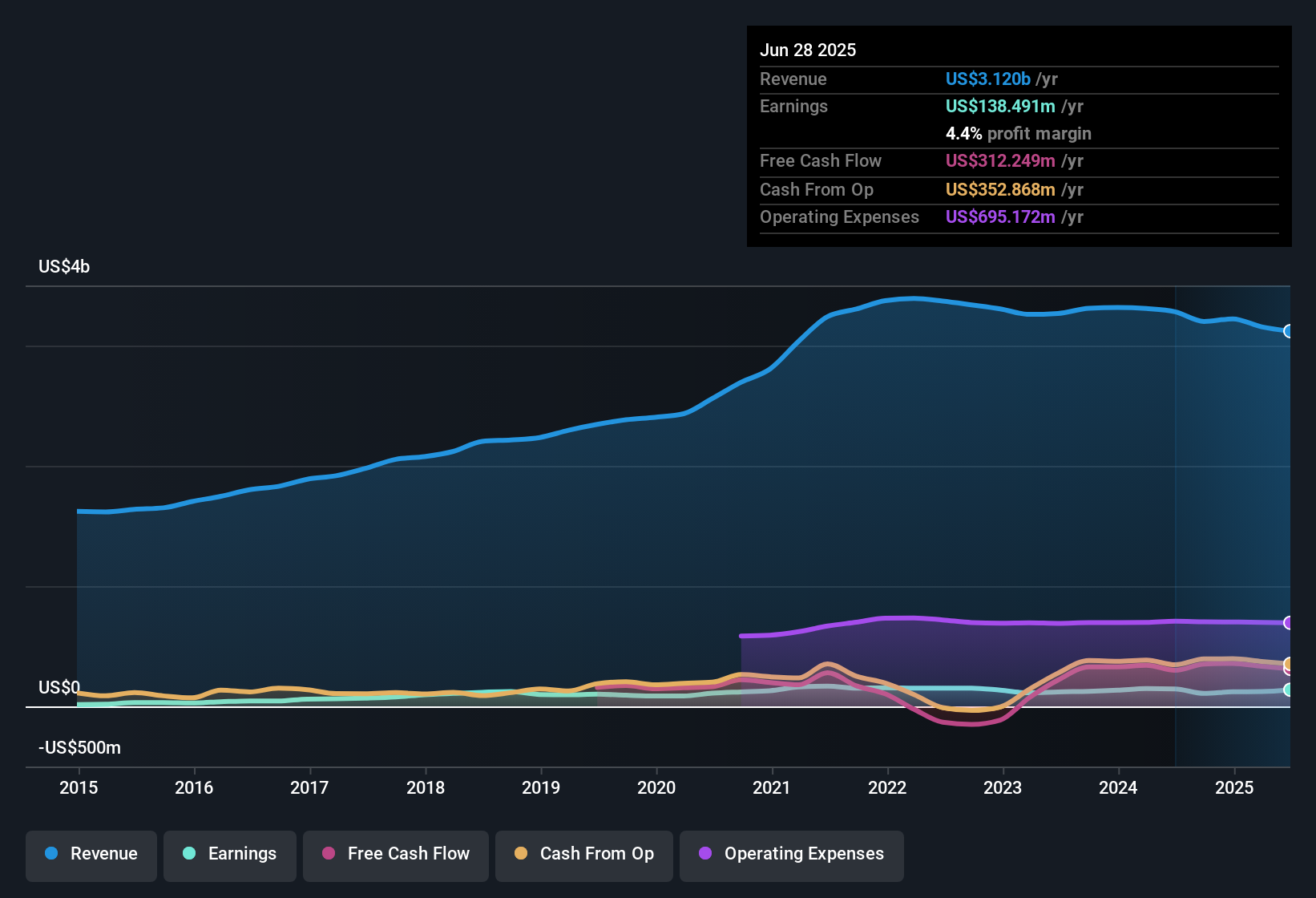

For Central Garden & Pet, the latest twelve month Free Cash Flow is about $287.5 million. Analysts plus modelled estimates project this to reach roughly $340.1 million in 2035 under a 2 Stage Free Cash Flow to Equity approach. Early years are guided by analyst forecasts, while the later years are extrapolated using more moderate growth assumptions based on Simply Wall St’s methodology.

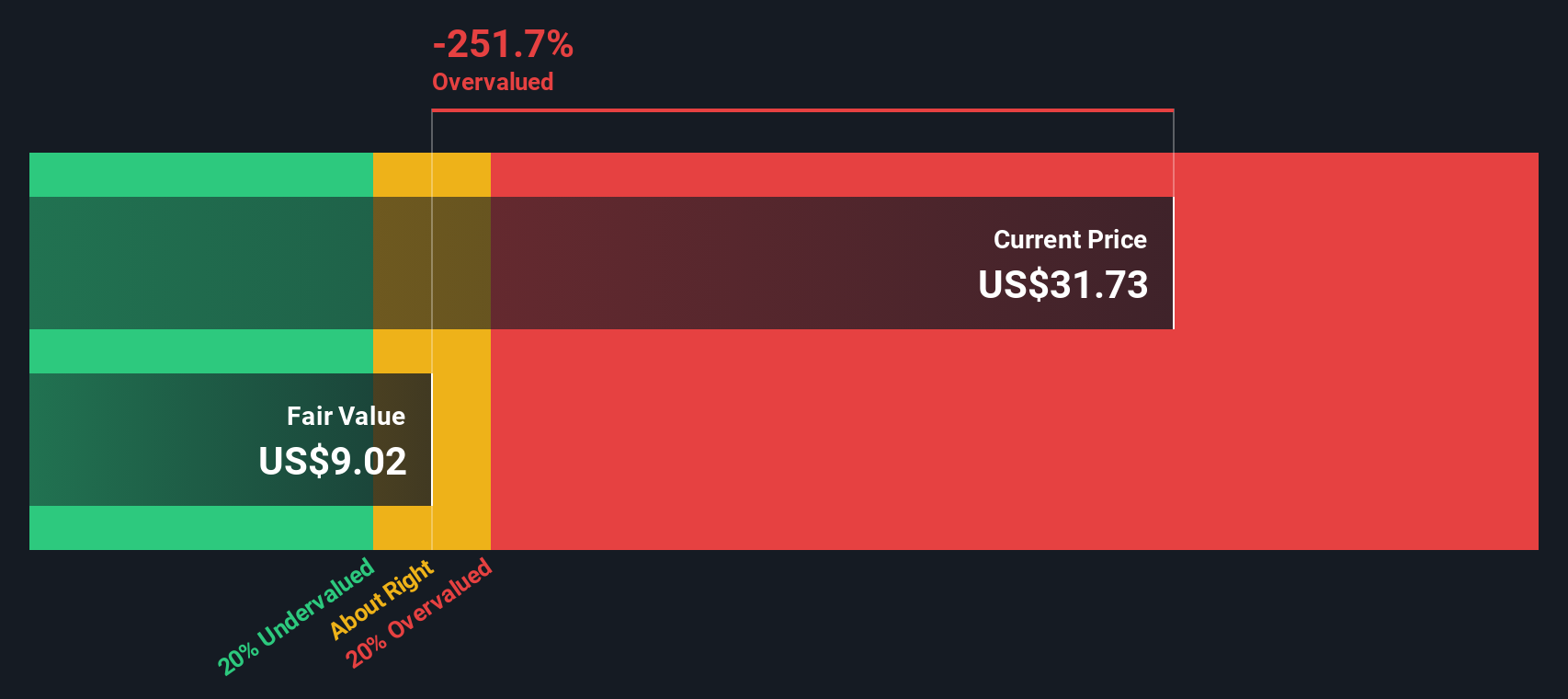

When all these future cash flows are discounted back, the model arrives at an intrinsic value of about $106.04 per share. Compared with the current share price around the low $30s, the DCF implies the stock is roughly 68.3% undervalued. This indicates that investors are paying far less than what the company’s projected cash generation appears to justify according to this model.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Central Garden & Pet is undervalued by 68.3%. Track this in your watchlist or portfolio, or discover 925 more undervalued stocks based on cash flows.

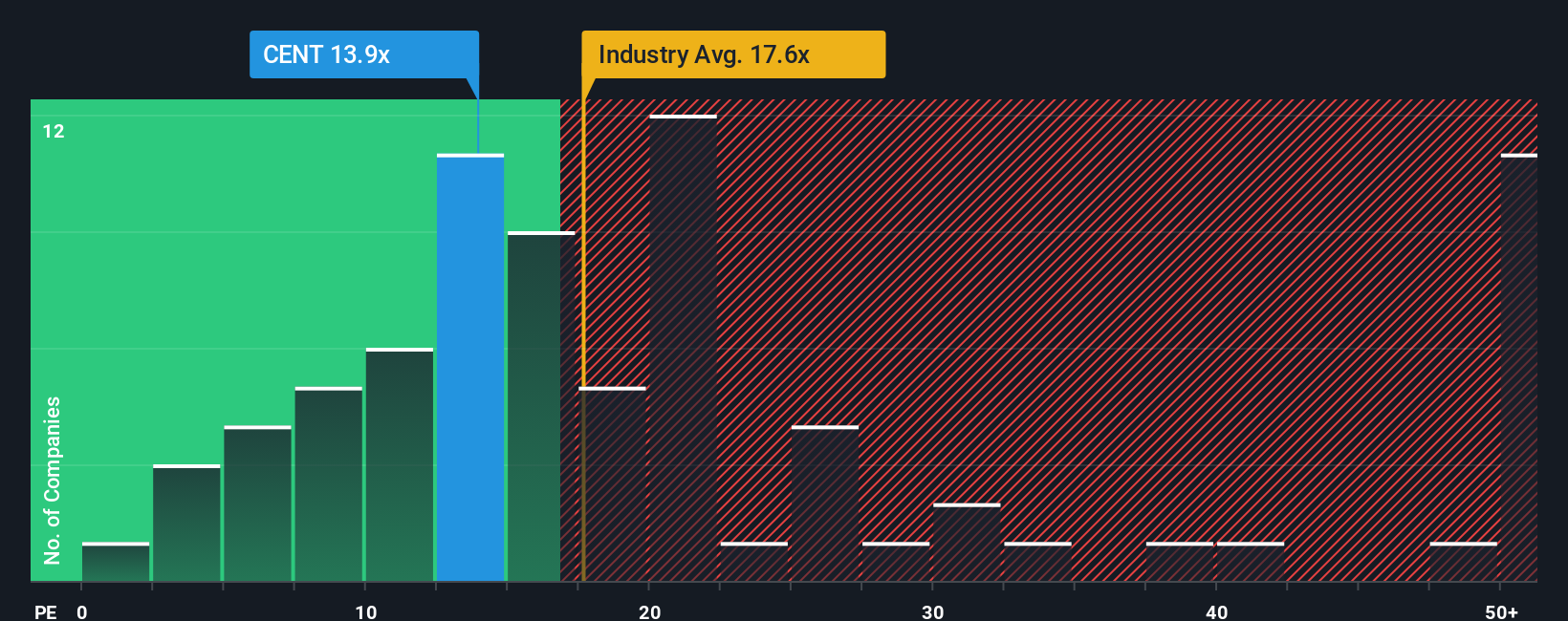

Approach 2: Central Garden & Pet Price vs Earnings

For profitable companies like Central Garden & Pet, the price to earnings (PE) ratio is a practical way to gauge value because it directly links what investors pay to the earnings the business is already generating. In general, faster growth and lower perceived risk justify a higher, or more expensive, PE, while slower growth or higher uncertainty usually warrant a lower multiple.

Central Garden & Pet currently trades on a PE of about 12.9x, which sits below both the Household Products industry average of roughly 17.5x and the broader peer group average near 16.1x. Simply Wall St also calculates a proprietary Fair Ratio of around 14.3x, which represents the PE you might expect given the company’s earnings growth outlook, margins, industry, market cap and risk profile.

This Fair Ratio is more informative than a simple comparison with peers or the industry because it adjusts for Central Garden & Pet’s specific strengths and risks rather than assuming it should trade exactly like its neighbors. Set against this tailored 14.3x Fair Ratio, the current 12.9x PE suggests the stock still trades at a discount on earnings terms.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1441 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Central Garden & Pet Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, which are simply the stories investors tell about a company that link their view of its future revenues, earnings and margins to a specific fair value estimate.

On Simply Wall St’s Community page, Narratives turn those stories into straightforward forecasts and fair values, so you can easily compare what you think Central Garden & Pet is worth with what the market is currently paying and decide whether that gap makes it a buy, a hold, or a sell.

Because Narratives update dynamically when new information comes in, such as earnings results, macro news or major strategy shifts, they remain a living reflection of how the Central Garden & Pet story is evolving rather than a static one off model.

For example, one investor might build a Narrative where premium pet and garden trends, margin expansion and e commerce investments support a fair value closer to the bullish 50 dollar target. In contrast, a more cautious investor might focus on weather risks, tariff pressure and category stagnation to justify something nearer the bearish 35 dollar view. With Narratives, you can quickly see where your own view of Central Garden & Pet sits between those extremes.

Do you think there's more to the story for Central Garden & Pet? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:CENT

Central Garden & Pet

Produces and distributes various products for the lawn and garden, and pet supplies markets in the United States.

Very undervalued with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

16 followersusers have followed this narrative

5 commentsusers have commented on this narrative

3 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$126.1% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$242.5% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

MA

MarkoVT on Alphabet ·

Positioned globally, partnered locally

Fair Value:US$390.1919.1% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

JO

JohnJ on Worldline ·

When will fraudsters be investigated in depth. Fraud was ongoing in France too.

Fair Value:€0.5200.8% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on Applied Digital ·

Staggered by dilution; positions for growth

Fair Value:US$35.4520.9% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.6% undervalued

112 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3927.5% undervalued

948 followersusers have followed this narrative

6 commentsusers have commented on this narrative

24 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3407.1% undervalued

148 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative