- United States

- /

- Medical Equipment

- /

- OTCPK:VAPO

Health Check: How Prudently Does Vapotherm (NYSE:VAPO) Use Debt?

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. Importantly, Vapotherm, Inc. (NYSE:VAPO) does carry debt. But the real question is whether this debt is making the company risky.

When Is Debt Dangerous?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we think about a company's use of debt, we first look at cash and debt together.

Check out our latest analysis for Vapotherm

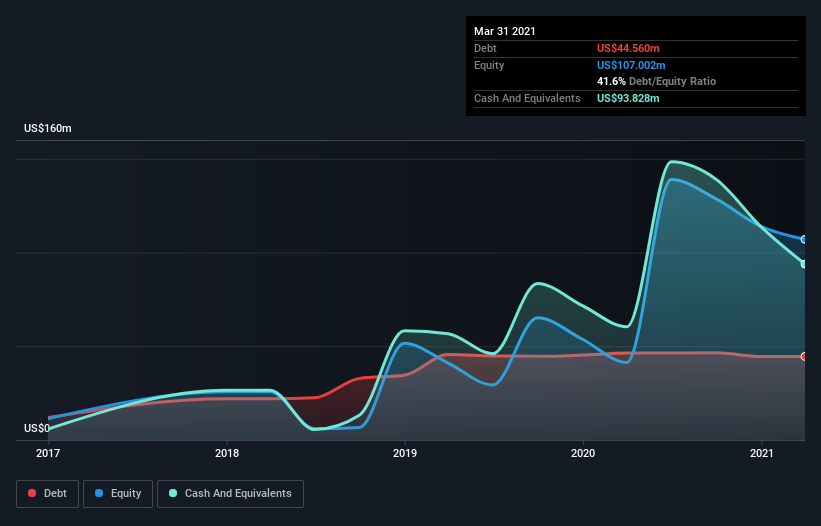

What Is Vapotherm's Debt?

As you can see below, Vapotherm had US$36.2m of debt at March 2021, down from US$46.3m a year prior. However, it does have US$93.8m in cash offsetting this, leading to net cash of US$57.6m.

How Healthy Is Vapotherm's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Vapotherm had liabilities of US$28.0m due within 12 months and liabilities of US$56.0m due beyond that. On the other hand, it had cash of US$93.8m and US$13.7m worth of receivables due within a year. So it actually has US$23.5m more liquid assets than total liabilities.

This short term liquidity is a sign that Vapotherm could probably pay off its debt with ease, as its balance sheet is far from stretched. Simply put, the fact that Vapotherm has more cash than debt is arguably a good indication that it can manage its debt safely. There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Vapotherm's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

In the last year Vapotherm wasn't profitable at an EBIT level, but managed to grow its revenue by 153%, to US$139m. So its pretty obvious shareholders are hoping for more growth!

So How Risky Is Vapotherm?

Statistically speaking companies that lose money are riskier than those that make money. And we do note that Vapotherm had an earnings before interest and tax (EBIT) loss, over the last year. And over the same period it saw negative free cash outflow of US$59m and booked a US$48m accounting loss. But at least it has US$57.6m on the balance sheet to spend on growth, near-term. Importantly, Vapotherm's revenue growth is hot to trot. High growth pre-profit companies may well be risky, but they can also offer great rewards. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. These risks can be hard to spot. Every company has them, and we've spotted 3 warning signs for Vapotherm you should know about.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

If you decide to trade Vapotherm, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About OTCPK:VAPO

Vapotherm

A medical technology company, focuses on the development and commercialization of proprietary high velocity therapy products used to treat patients of various ages suffering from respiratory distress in the United States and internationally.

Slight and slightly overvalued.

Similar Companies

Market Insights

Community Narratives