Advertisement

- United States

- /

- Healthcare Services

- /

- NYSE:UHS

How Investors May Respond To Universal Health Services (UHS) Options Surge and Analyst Optimism After Mixed Earnings

Simply Wall St

Reviewed by Simply Wall St

- Earlier this month, Universal Health Services released its second quarter 2025 earnings report, revealing mixed performance across its segments and highlighting shifts in payer dynamics that are influencing investor sentiment.

- Rising implied volatility in UHS’s options market, alongside upward analyst earnings estimate revisions, underscores growing anticipation of a potential significant event impacting the company’s future outlook.

- We'll explore how heightened options activity and analyst optimism may shift Universal Health Services' investment narrative and future expectations.

Uncover the next big thing with financially sound penny stocks that balance risk and reward.

Universal Health Services Investment Narrative Recap

To be a Universal Health Services shareholder, you need to believe in the company’s ability to drive consistent revenue and profit growth through its diversified acute care and behavioral health business, while managing risks around reimbursement, competition, and labor. The recent surge in options market volatility and upward analyst estimate revisions signal anticipation of an upcoming catalyst, but they do not materially alter the most important short-term driver, successful execution on improved payer mix, or the key risk, which remains regulatory exposure tied to Medicaid rate changes.

The most relevant announcement is Universal Health Services’ raised 2025 revenue guidance following its second-quarter results, reflecting management’s confidence despite mixed segment performance and ongoing shifts in payer dynamics. This directly links to the company’s ability to manage reimbursement headwinds and capitalize on new behavioral health opportunities, the main catalysts attracting market attention right now.

However, against these catalysts, investors should also be mindful of the company’s continued reliance on government payors and what happens if future Medicaid policies shift...

Read the full narrative on Universal Health Services (it's free!)

Universal Health Services is projected to achieve $19.0 billion in revenue and $1.5 billion in earnings by 2028. This outlook assumes a 5.0% annual revenue growth rate and a $0.2 billion increase in earnings from the current level of $1.3 billion.

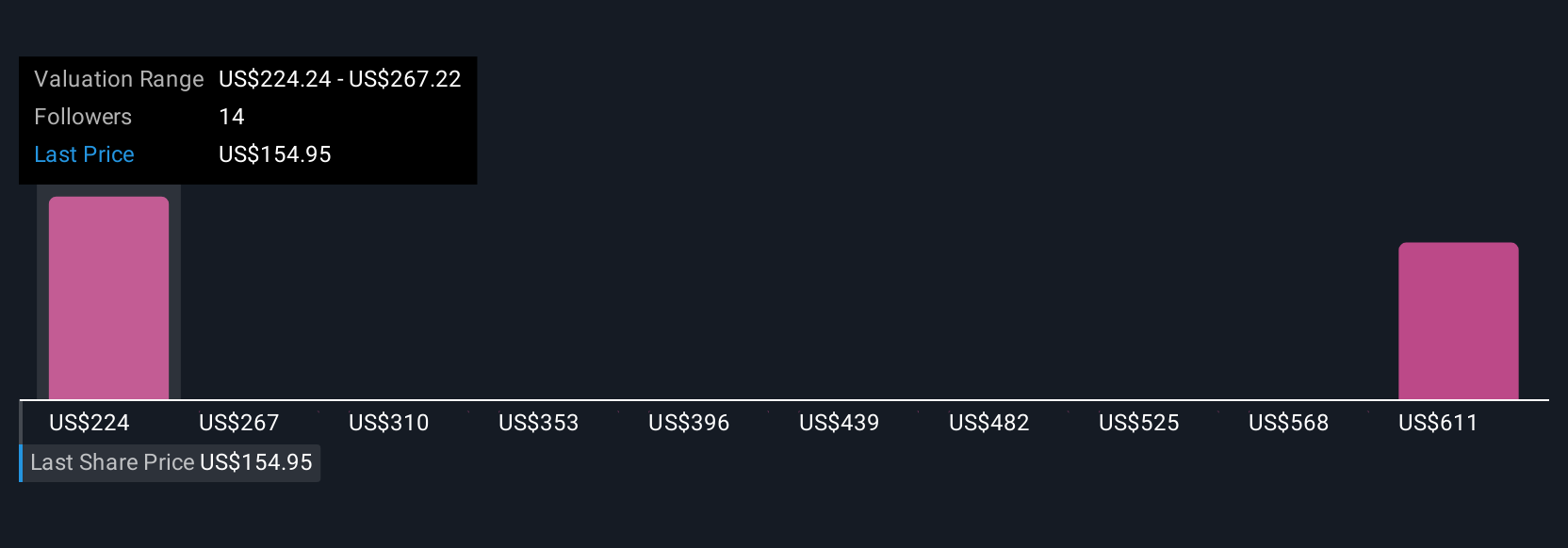

Uncover how Universal Health Services' forecasts yield a $218.31 fair value, a 14% upside to its current price.

Exploring Other Perspectives

Three members of the Simply Wall St Community have posted fair value targets for UHS ranging widely from US$218.31 to US$644.04 per share. While expectations differ, the company’s increasing focus on higher-margin outpatient behavioral health could reshape its revenue base, inviting you to explore these diverse viewpoints further.

Explore 3 other fair value estimates on Universal Health Services - why the stock might be worth over 3x more than the current price!

Build Your Own Universal Health Services Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Universal Health Services research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Universal Health Services research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Universal Health Services' overall financial health at a glance.

Want Some Alternatives?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- AI is about to change healthcare. These 31 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- We've found 18 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:UHS

Universal Health Services

Through its subsidiaries, owns and operates acute care hospitals, and outpatient and behavioral health care facilities.

Undervalued with solid track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

Quality at a Premium. A time to watch, not to buy?

Fair Value US$154.56|29.9% undervalued

DA

Community Contributor

GRAB: The Super-App at the Heart of Southeast Asia’s Digital Boom

Fair Value US$8.20|22.9% undervalued

BL

Community Contributor

Verve Group to Surge with 51.61% Revenue Growth

Fair Value €6.00|64.1% undervalued

ME

Community Contributor