- United States

- /

- Healthtech

- /

- NYSE:PHR

Phreesia (PHR) Reports Q2 Earnings with Sales Rising from US$28M to US$35M

Reviewed by Simply Wall St

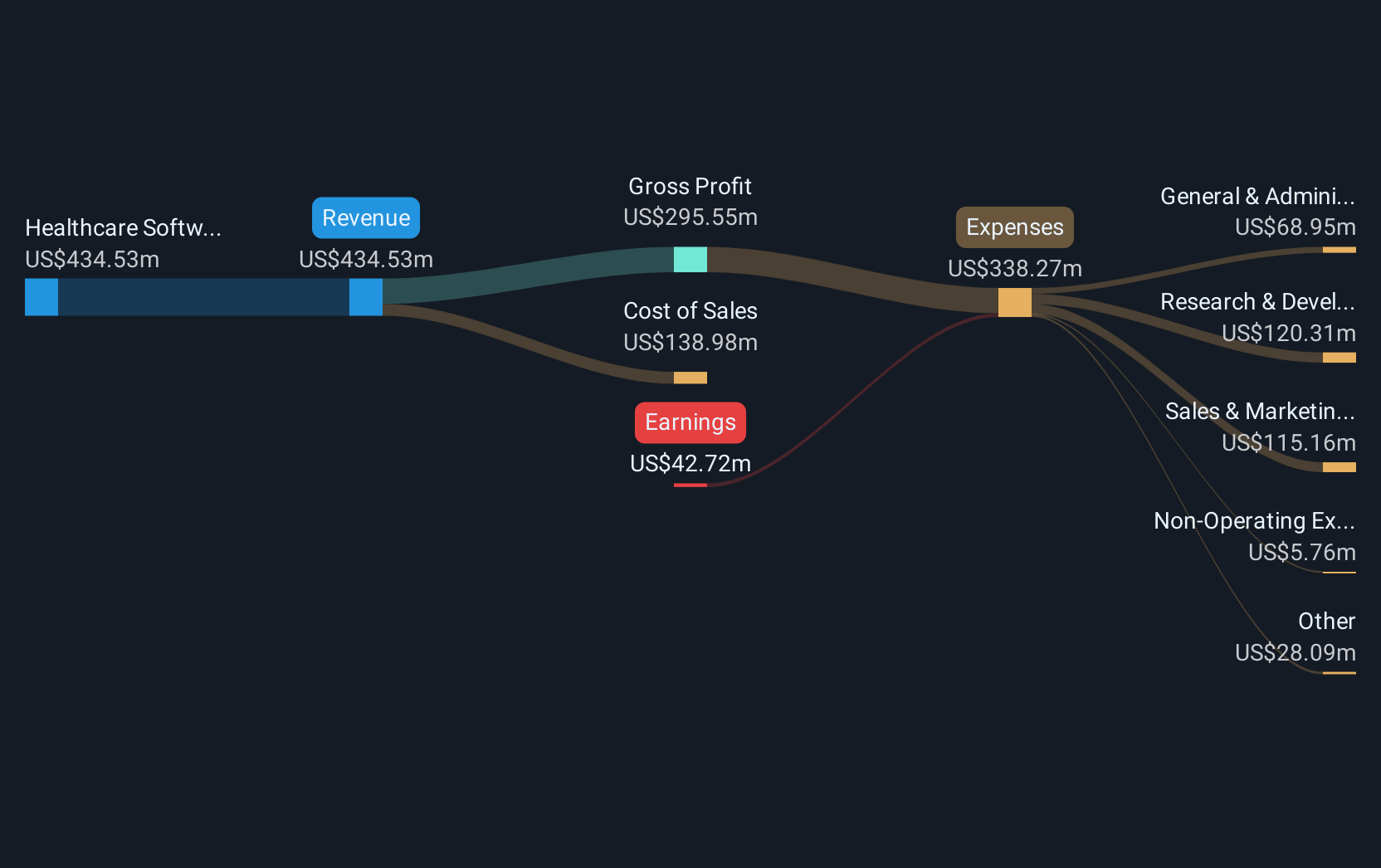

Phreesia (PHR) recently announced its second-quarter earnings, showcasing significant growth with sales climbing from $28 million to $35 million and net income improving from a loss to a positive figure. Despite these positive results and the launch of Phreesia VoiceAI, the company's stock experienced a small decline of 1.7% over the past month. This movement came as broad markets, including the S&P 500 and Nasdaq, hit all-time highs with tech and AI stocks leading gains. Phreesia's developments offered a counterbalance to general positive market trends, maintaining investor interest amid broader economic shifts.

We've spotted 1 weakness for Phreesia you should be aware of.

Uncover the next big thing with financially sound penny stocks that balance risk and reward.

Phreesia's recent earnings announcement, highlighting a revenue increase from US$28 million to US$35 million and a shift from a loss to a positive net income, showcases its growing financial health. This news, alongside the launch of Phreesia VoiceAI, could enhance future revenue and earnings forecasts, particularly as digital adoption in healthcare continues to expand. Phreesia's integration of AI could further support operating efficiencies and product differentiation, benefiting long-term revenue and earnings potential.

Over the past year, Phreesia's total shareholder return, inclusive of share price movements and dividends, reached 12.36%. This performance is supported by increasing adoption of its value-added modules and persistent industry trends favoring digital health solutions. However, the company's 1% decline over the past month contrasts with the broader market's record highs. Phreesia underperformed compared to the US and healthcare services industries, both of which recorded higher returns over the past year.

With the current share price at US$26.55, Phreesia is trading at a discount to the consensus analyst price target of US$34, indicating a potential upside of around 28%. While analysts expect revenue and profit margins to improve significantly over the coming years, it is essential for investors to weigh such expectations against existing competitive and regulatory challenges. The current price movement, set in the context of the price target, may provide an opportunity for investors considering the company's long-term growth prospects.

Explore Phreesia's analyst forecasts in our growth report.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:PHR

Phreesia

Provides an integrated SaaS-based software and payment platform for the healthcare industry in the United States and Canada.

Very undervalued with flawless balance sheet.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fiverr International will transform the freelance industry with AI-powered growth

Jackson Financial Stock: When Insurance Math Meets a Shifting Claims Landscape

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion