Advertisement

- United States

- /

- Medical Equipment

- /

- NYSE:NVRO

Nevro Corp.'s (NYSE:NVRO) Price Is Right But Growth Is Lacking After Shares Rocket 30%

Nevro Corp. (NYSE:NVRO) shares have had a really impressive month, gaining 30% after a shaky period beforehand. Still, the 30-day jump doesn't change the fact that longer term shareholders have seen their stock decimated by the 73% share price drop in the last twelve months.

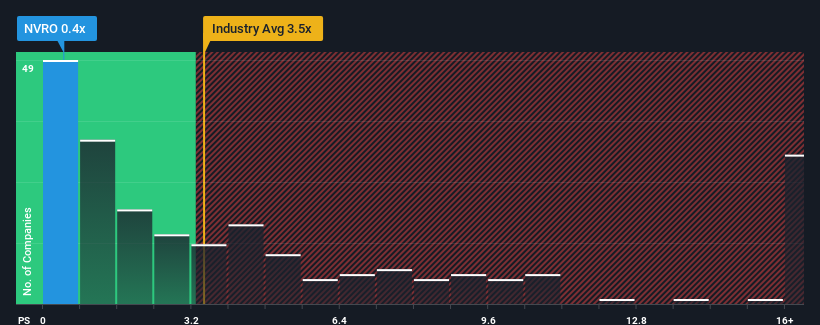

Even after such a large jump in price, Nevro may still look like a strong buying opportunity at present with its price-to-sales (or "P/S") ratio of 0.4x, considering almost half of all companies in the Medical Equipment industry in the United States have P/S ratios greater than 3.5x and even P/S higher than 8x aren't out of the ordinary. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's so limited.

Check out our latest analysis for Nevro

What Does Nevro's P/S Mean For Shareholders?

Nevro hasn't been tracking well recently as its declining revenue compares poorly to other companies, which have seen some growth in their revenues on average. It seems that many are expecting the poor revenue performance to persist, which has repressed the P/S ratio. If this is the case, then existing shareholders will probably struggle to get excited about the future direction of the share price.

Keen to find out how analysts think Nevro's future stacks up against the industry? In that case, our free report is a great place to start.What Are Revenue Growth Metrics Telling Us About The Low P/S?

In order to justify its P/S ratio, Nevro would need to produce anemic growth that's substantially trailing the industry.

Retrospectively, the last year delivered virtually the same number to the company's top line as the year before. Fortunately, a few good years before that means that it was still able to grow revenue by 6.4% in total over the last three years. Therefore, it's fair to say that revenue growth has been inconsistent recently for the company.

Looking ahead now, revenue is anticipated to climb by 1.9% per annum during the coming three years according to the analysts following the company. That's shaping up to be materially lower than the 9.7% per annum growth forecast for the broader industry.

In light of this, it's understandable that Nevro's P/S sits below the majority of other companies. It seems most investors are expecting to see limited future growth and are only willing to pay a reduced amount for the stock.

What Does Nevro's P/S Mean For Investors?

Nevro's recent share price jump still sees fails to bring its P/S alongside the industry median. Typically, we'd caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

We've established that Nevro maintains its low P/S on the weakness of its forecast growth being lower than the wider industry, as expected. At this stage investors feel the potential for an improvement in revenue isn't great enough to justify a higher P/S ratio. Unless these conditions improve, they will continue to form a barrier for the share price around these levels.

You always need to take note of risks, for example - Nevro has 2 warning signs we think you should be aware of.

If you're unsure about the strength of Nevro's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Valuation is complex, but we're here to simplify it.

Discover if Nevro might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:NVRO

Nevro

A medical device company, engages in the provision of products for patients suffering from chronic pain in the United States and internationally.

Excellent balance sheet and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|32.0% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|21.7% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|0.5% overvalued

DA

Community Contributor