Advertisement

- United States

- /

- Healthcare Services

- /

- NYSE:MOH

Molina Healthcare (NYSE:MOH) Could Easily Take On More Debt

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. As with many other companies Molina Healthcare, Inc. (NYSE:MOH) makes use of debt. But is this debt a concern to shareholders?

When Is Debt A Problem?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. If things get really bad, the lenders can take control of the business. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

View our latest analysis for Molina Healthcare

How Much Debt Does Molina Healthcare Carry?

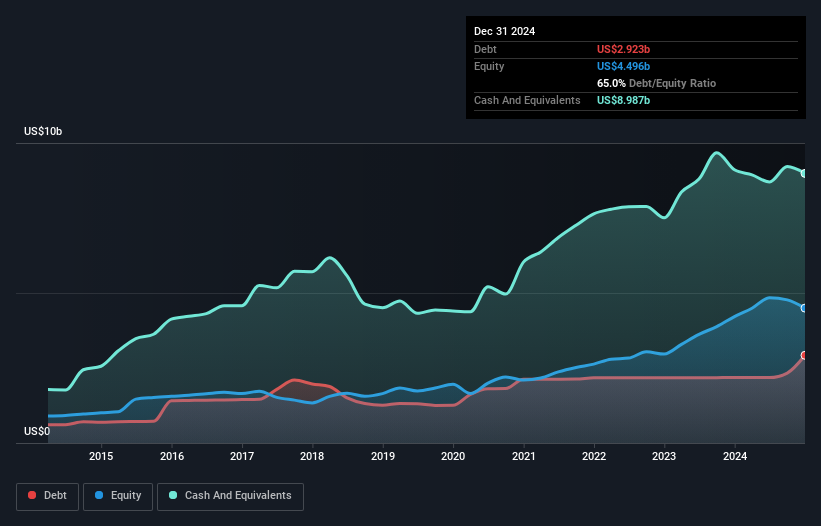

As you can see below, at the end of December 2024, Molina Healthcare had US$2.92b of debt, up from US$2.18b a year ago. Click the image for more detail. But it also has US$8.99b in cash to offset that, meaning it has US$6.06b net cash.

How Strong Is Molina Healthcare's Balance Sheet?

We can see from the most recent balance sheet that Molina Healthcare had liabilities of US$7.90b falling due within a year, and liabilities of US$3.24b due beyond that. Offsetting this, it had US$8.99b in cash and US$3.30b in receivables that were due within 12 months. So it actually has US$1.15b more liquid assets than total liabilities.

This short term liquidity is a sign that Molina Healthcare could probably pay off its debt with ease, as its balance sheet is far from stretched. Succinctly put, Molina Healthcare boasts net cash, so it's fair to say it does not have a heavy debt load!

The good news is that Molina Healthcare has increased its EBIT by 5.8% over twelve months, which should ease any concerns about debt repayment. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Molina Healthcare can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. While Molina Healthcare has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. During the last three years, Molina Healthcare produced sturdy free cash flow equating to 60% of its EBIT, about what we'd expect. This cold hard cash means it can reduce its debt when it wants to.

Summing Up

While we empathize with investors who find debt concerning, you should keep in mind that Molina Healthcare has net cash of US$6.06b, as well as more liquid assets than liabilities. So we don't think Molina Healthcare's use of debt is risky. We'd be very excited to see if Molina Healthcare insiders have been snapping up shares. If you are too, then click on this link right now to take a (free) peek at our list of reported insider transactions.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:MOH

Molina Healthcare

Provides managed healthcare services to low-income families and individuals under the Medicaid and Medicare programs and through the state insurance marketplaces.

Undervalued with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|27.5% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|4.2% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|27.0% undervalued

KA

Community Contributor