If you are keeping an eye on McKesson stock these days, you are hardly alone. Whether you are a current shareholder, thinking about jumping in, or just watching for cues from one of healthcare’s giants, recent movements in MCK have definitely stirred up conversation. In the past year alone, the stock has gained nearly 24%, a run that easily outpaces the broader market and hints at serious momentum. For those with a longer view, the total return over five years has soared to more than 360%, making some investors wish they had bought in even sooner.

Shorter-term moves, however, show a more mixed picture. The last month saw McKesson dip about 4.6%, while the 90-day period is similarly negative. Yet, despite these pullbacks, the stock remains up nearly 20% for the year, and it trades at a healthy discount, about 16% below its average analyst price target. Some of this volatility ties back to shifting market sentiment on healthcare distribution and ongoing conversations about regulatory changes, profitability, and buying patterns across the sector.

If you are wondering whether McKesson is still a good value, the short answer is not straightforward. On a standard six-factor valuation checklist, MCK is undervalued in 3 out of 6 areas, earning it a value score of 3. That is enough to make value-oriented investors perk up, but there are nuances behind those checks, and several popular methods of assessing what the stock is truly worth. Let’s break down those approaches next, before digging into what might be an even more useful way to think about McKesson’s valuation.

McKesson delivered 24.0% returns over the last year. See how this stacks up to the rest of the Healthcare industry.

Advertisement

Approach 1: McKesson Cash Flows

A Discounted Cash Flow (DCF) model is a classic way to estimate what a company is really worth by projecting its future cash flows and then discounting them back to today’s value. Put simply, this approach looks ahead at how much cash McKesson could generate in the future, brings those numbers to the present using a set discount rate, and lands on what the business might be intrinsically worth right now.

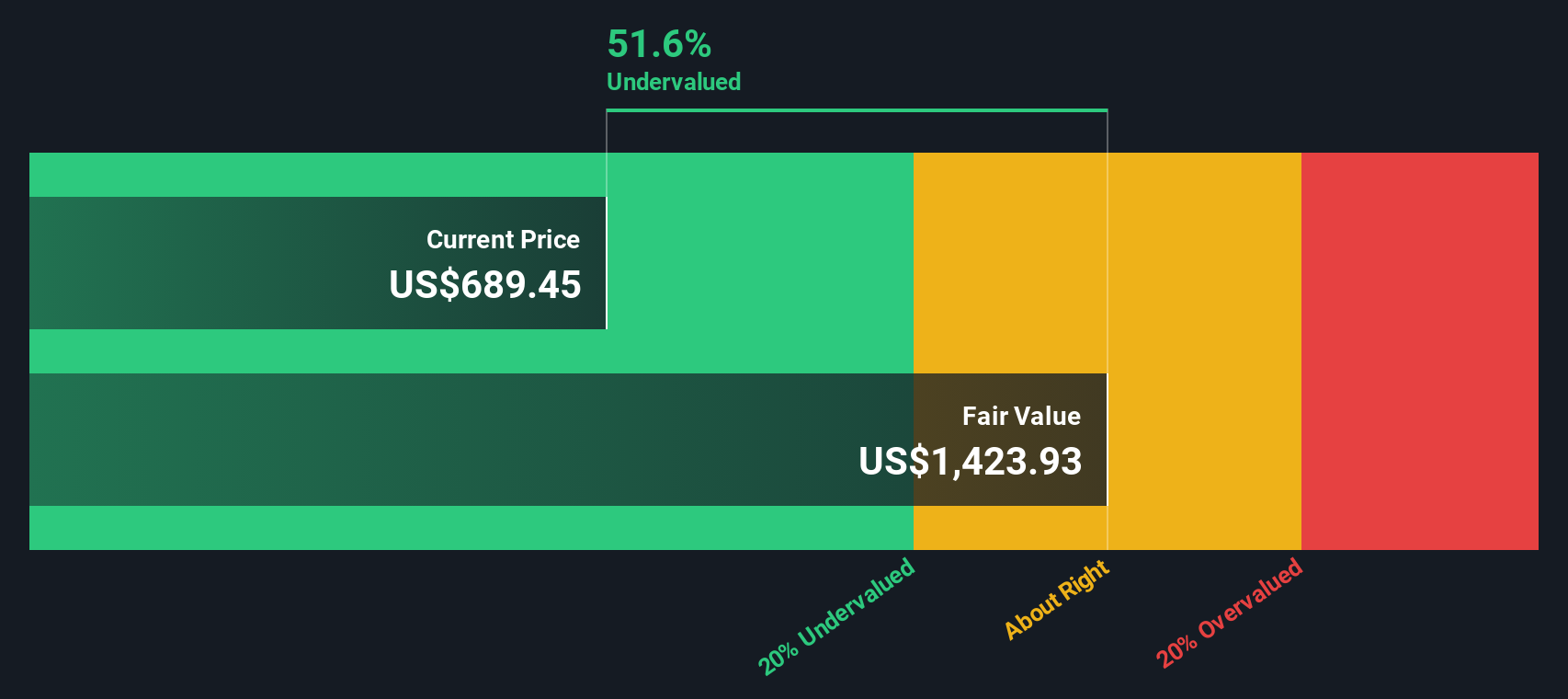

Currently, McKesson generates robust Free Cash Flow (FCF), with $5.7 billion produced over the last twelve months. Analysts expect this number to keep growing, projecting FCF to reach approximately $8.9 billion by 2035. This reflects a solid uptrend, with 10-year projections steadily increasing each year.

Using these figures in a two-stage Free Cash Flow to Equity model results in an estimated intrinsic value of $1,423.93 per share. This valuation suggests McKesson stock is trading at a significant 52.5% discount to its underlying worth. In other words, it may be considered 52.5% undervalued based on its long-term cash-generating potential.

For investors focused on the fundamentals, this DCF approach highlights considerable upside if those cash flows materialize as forecast.

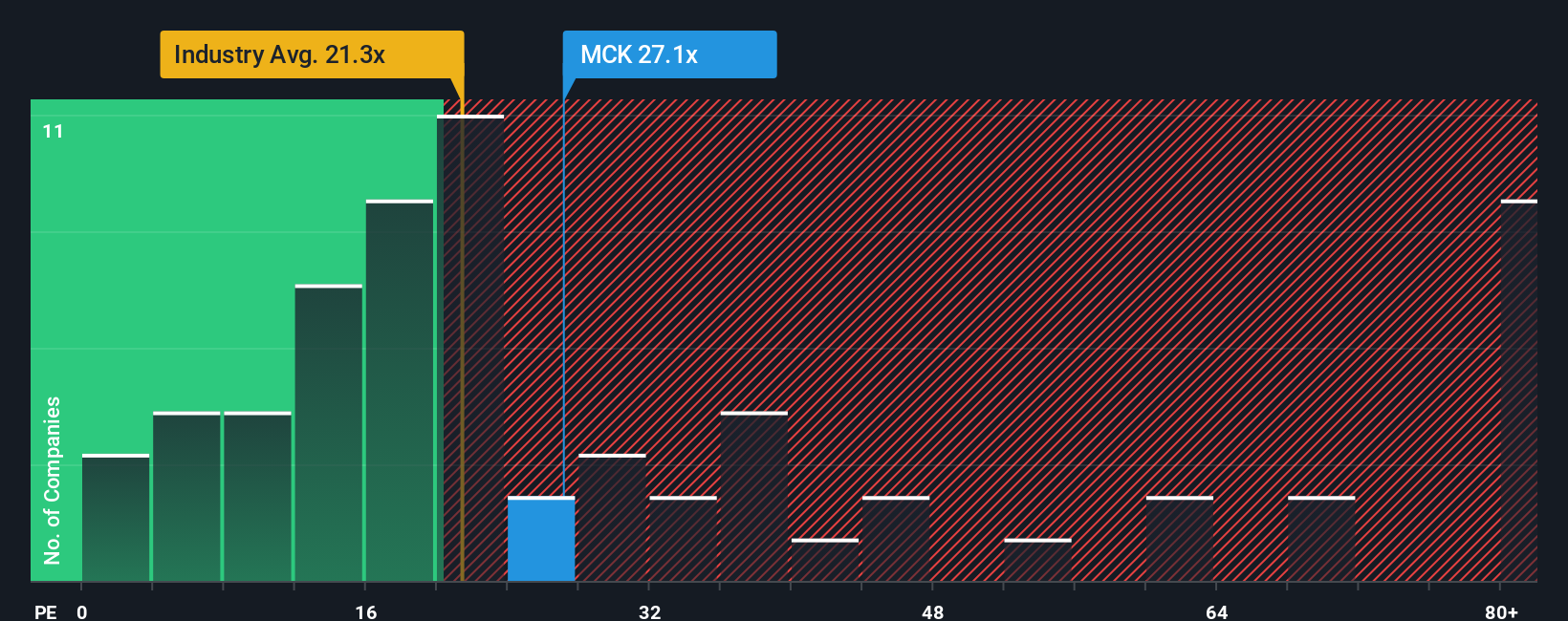

For profitable companies like McKesson, the Price-to-Earnings (PE) ratio is one of the most widely used tools for evaluating whether a stock is trading at a reasonable valuation. The PE ratio helps investors understand how much they are paying for each dollar of the company's earnings. This is especially useful when those earnings are consistent and reliable.

A "normal" or "fair" PE ratio depends on several factors, including a company’s expected growth rate and the level of risk investors are willing to accept. Higher anticipated growth or lower risk often justifies a higher PE ratio. Conversely, slower growth or more uncertainty may lead to lower multiples being considered appropriate.

Looking at the numbers, McKesson currently trades at a PE ratio of 26.6x. This is above both the Healthcare industry average of 21.3x and the average PE ratio of close peers, which sits at 22.6x. However, Simply Wall St’s proprietary Fair Ratio for McKesson is 31.9x. This figure takes into account the company’s earnings growth prospects, its size, profit margins, and risks relative to industry norms.

With the Fair Ratio notably higher than McKesson’s current PE, this approach suggests that the stock may actually be undervalued relative to what its fundamentals warrant, even though it appears pricier than some industry benchmarks.

Upgrade Your Decision Making: Choose your McKesson Narrative

Beyond ratios and cash flow models, Narratives offer a smarter, more dynamic way to make investment decisions by connecting a company's story—your personal perspective, assumptions, and insights on its future—to its estimated fair value. A Narrative empowers you to weave together everything you know or believe about McKesson, from evolving healthcare demand and digital innovation to regulatory risks and shifting business models. You can then use those expectations to forecast future revenue, earnings, margins, and ultimately, what you think the shares are truly worth.

Within the Simply Wall St platform and investor community, Narratives are effortless to create and update. They provide you with an accessible tool that exists alongside millions of other perspectives. By constantly incorporating the very latest news and earnings data, your Narrative helps you instantly see how your fair value view compares with the current market price, clarifying whether it might be more appropriate to buy, hold, or sell.

For example, even among professionals, one Narrative sees McKesson as worth as much as $830.00 per share thanks to optimism about pharmaceutical demand and automation. Another places fair value at $640.00 due to concerns over tighter regulation and industry disruption. The power of Narratives lies in making these differing perspectives crystal clear, letting you decide which story fits you best.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency • Be alerted to new Warning Signs or Risks via email or mobile • Track the Fair Value of your stocks