Advertisement

- United States

- /

- Healthcare Services

- /

- NYSE:MCK

McKesson (MCK): Assessing Valuation After Dividend Hike and Strategic Refocus on High-Margin Services

Simply Wall St

Reviewed by Kshitija Bhandaru

McKesson, fresh from its recent investor day, is drawing attention with its sharpened outlook and strategic changes. The company’s Board just approved a 15% quarterly dividend increase and outlined plans to separate its Medical-Surgical business.

See our latest analysis for McKesson.

McKesson’s sharpened strategy, dividend boost, and growing focus on higher-margin segments have attracted attention this year. The company’s momentum is clear, with a 33.9% year-to-date share price return and an impressive 50.4% total shareholder return over the past twelve months. This points to renewed optimism among investors about its long-term opportunities.

If McKesson’s strategic moves have you rethinking your portfolio, this is the perfect moment to discover See the full list for free.

But with shares already up more than 50% in the past year and analysts raising fair value estimates, the key question is whether McKesson still offers upside or if its future growth is already reflected in the stock price.

Most Popular Narrative: 8.6% Undervalued

With the most recent closing price at $757.96, the leading narrative from analysts assigns McKesson a fair value of $829.57. This is a notable margin above today’s price and a signal that the market may be underestimating its future potential.

Operational efficiency gains driven by automation and digitization support margin improvement and reinforce market leadership. Expanding value-added services, such as pharmacy management, patient access/adherence solutions, and commercialization support for biopharma customers, allow for stronger customer relationships, greater recurring revenue streams, and improved revenue visibility.

What’s driving this outperformance? The underlying assumptions point to ambitious growth, improving profit margins, and a future profit multiple not typically seen in this sector. Wondering what else goes into these bullish projections? Unlock the full narrative for the numbers and logic behind McKesson’s fair value target.

Result: Fair Value of $829.57 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, sustained regulatory pressure on drug pricing or further industry consolidation could quickly undermine McKesson’s margin expansion and slow its revenue growth trajectory.

Find out about the key risks to this McKesson narrative.

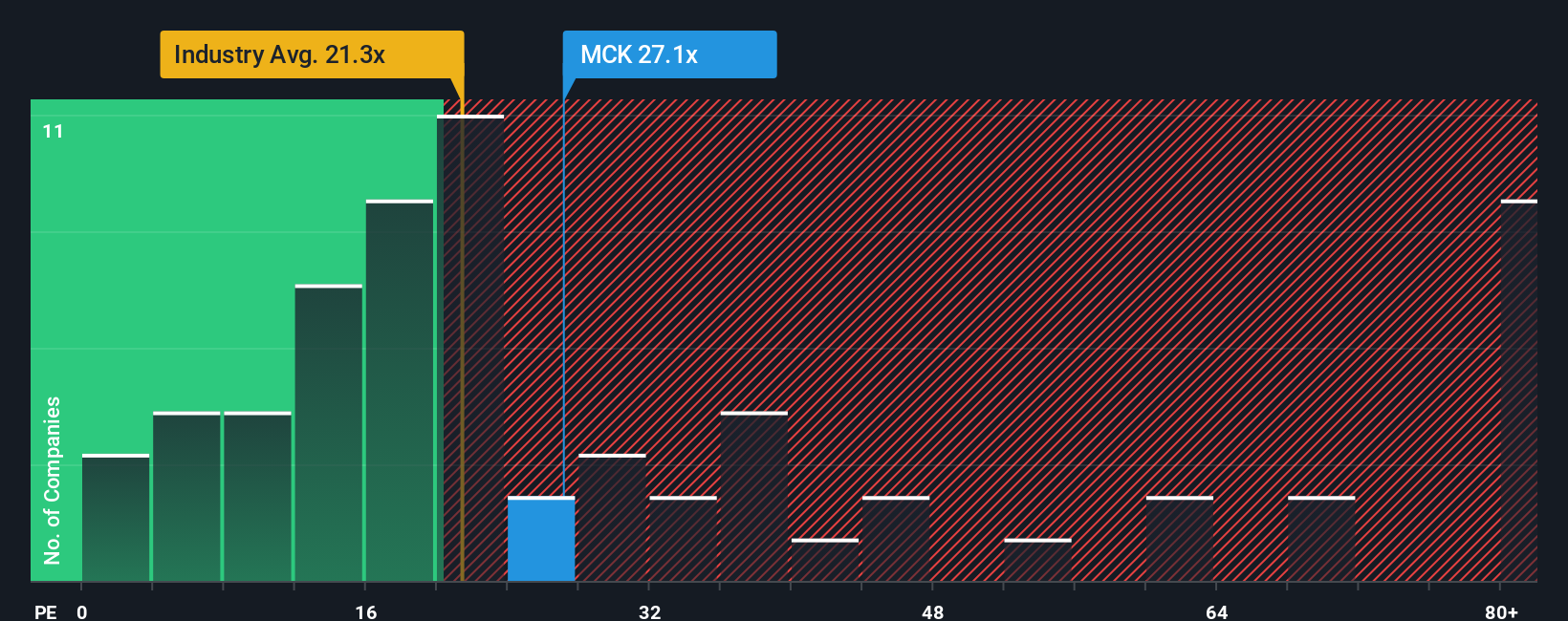

Another View: Comparing Market Ratios

Looking at McKesson’s valuation from a different angle, its current price-to-earnings ratio sits at 29.8x, significantly higher than both the US Healthcare industry average of 21.6x and its peer average of 23.1x. Although the fair ratio for McKesson is estimated at 31x, suggesting some room for justification, the high premium leaves little margin for error if growth expectations falter. Could this premium signal risk, or is the market betting on McKesson’s potential?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own McKesson Narrative

If you have a different perspective or want to dig deeper into the numbers, you can analyze the data yourself and shape your own McKesson story in just a few minutes. Do it your way.

A great starting point for your McKesson research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for More Investment Ideas?

Ambitious investors know that growth does not stop at one company. Now is your chance to access new opportunities and stay ahead by tapping into unique market themes.

- Unlock the potential of digital finance by checking out these 79 cryptocurrency and blockchain stocks that are pioneering the latest advances in blockchain and payment technology.

- Accelerate your search for strong returns by reviewing these 897 undervalued stocks based on cash flows currently trading below fair value, based on future cash flows and fundamentals.

- Capitalize on the AI revolution and see which innovators are making waves with these 25 AI penny stocks shaping the next era of smart automation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:MCK

McKesson

Provides healthcare services in the United States and internationally.

Fair value with limited growth.

Similar Companies

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|12.2% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|17.1% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|38.7% undervalued

TR

Community Contributor