- United States

- /

- Healthcare Services

- /

- NYSE:DGX

Quest Diagnostics (NYSE:DGX) Board Declares US$0.80 Quarterly Dividend

Reviewed by Simply Wall St

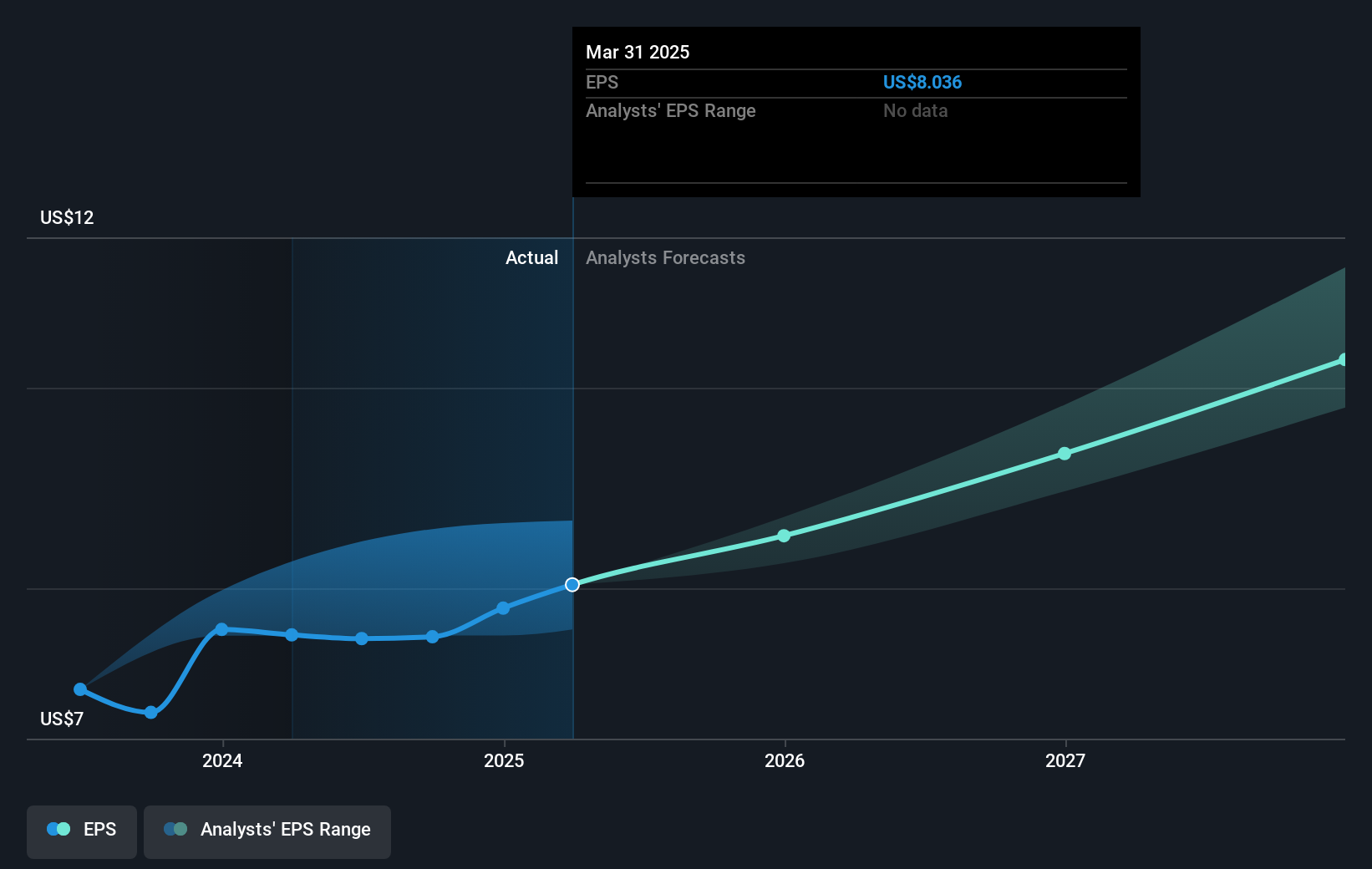

Quest Diagnostics (NYSE:DGX) recently affirmed a quarterly dividend of $0.80 per share, reinforcing its commitment to returning value to its shareholders. This announcement, coupled with raised earnings guidance and positive first-quarter earnings results—including a 12% sales increase and improved EPS—likely supported the company's 3% price gain over the past month. In comparison, the broader market remained robust with a general upward trend. Despite these positive developments, a lack of shares bought back during the period highlights a potential area for investor focus. Overall, Quest Diagnostics aligned, but did not uniquely shift, with broader market movements.

Be aware that Quest Diagnostics is showing 1 warning sign in our investment analysis.

The recent affirmation of a US$0.80 per share dividend by Quest Diagnostics underscores their shareholder value focus and complements the positive news from raised earnings guidance and robust first-quarter results. Over a longer term, Quest Diagnostics has achieved a total return of 67.08%, demonstrating a positive trajectory over a five-year span. Compared to the broader healthcare industry, Quest's one-year return surpasses the sector's negative performance of 22.2%, reflecting its relative resilience in the more immediate term.

The current developments, particularly the strategic dividend affirmation and absence of share buybacks, could influence investor sentiment and position Quest favorably for anticipated revenue and earnings growth. Analyst forecasts project revenue and earnings increases by 4.8% and greater margins over the coming years, despite the challenges of operational pressures and potential economic uncertainty. However, with current shares priced at US$176.11, close to the analyst consensus target of US$183.92, the scope for immediate price appreciation may be limited, aligning with the view that Quest is fairly valued. Investors should carefully consider these factors when assessing potential financial outcomes.

Take a closer look at Quest Diagnostics' potential here in our financial health report.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Quest Diagnostics might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:DGX

Quest Diagnostics

Provides diagnostic testing and services in the United States and internationally.

Established dividend payer and good value.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

Deep Value Multi Bagger Opportunity

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)