- United States

- /

- Healthcare Services

- /

- NYSE:CNC

Centene (NYSE:CNC) Reports Strong Q1 Results With Increased Revenue And Earnings Guidance

Reviewed by Simply Wall St

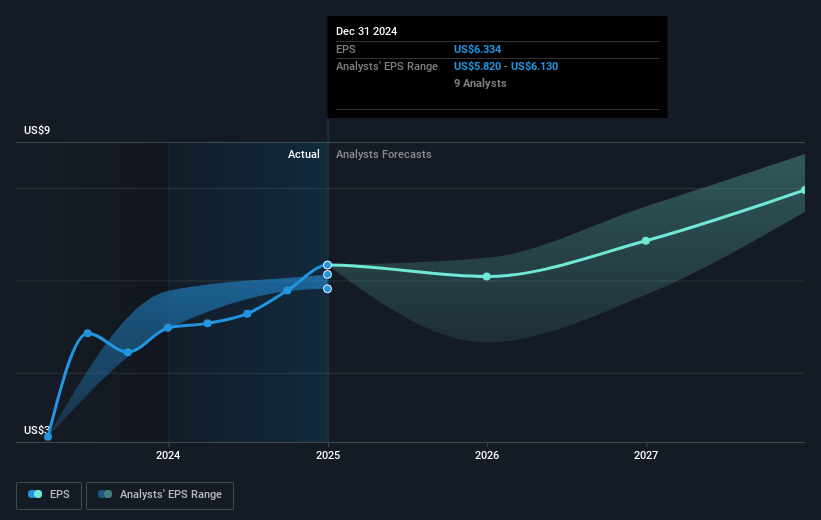

Centene (NYSE:CNC) reported strong financial performance for Q1 2025, with a revenue increase to $46.62 billion, up from the previous year's $40.41 billion, along with an uplift in net income and EPS. Following this, the company saw a 4.48% share price increase over the past month. Additionally, Centene confirmed its full-year guidance, raising revenue projections due to strong enrollment, highlighting a robust health trajectory. In a broader context of mixed market movements, Centene's performance paralleled the Dow's rise and sustained market volatility, illustrating investor confidence amid the ongoing tariff discussions that influenced wider market sentiment.

Buy, Hold or Sell Centene? View our complete analysis and fair value estimate and you decide.

The recent report of strong financial performance for Centene in Q1 2025, with revenues climbing to US$46.62 billion, underscores its ongoing growth initiatives despite sector headwinds. Centene's focus on modernization through AI and the expansion of Medicare and Medicaid services is aligned with this revenue surge and bolstered investor confidence, as seen by the 4.48% share price uptick. This momentum may influence analysts' revenue and earnings forecasts, potentially enhancing the outlook further and supporting their positive sentiment regarding the company’s strategic efforts.

Over the past five years, Centene's total return, which includes share price and dividends, witnessed a 7.51% decline, indicating challenges in sustaining long-term stockholder value. By comparison, it has lagged behind the broader US market's positive return of 7.9% over the last year. Such performance metrics highlight the uphill task Centene faces in maintaining competitiveness and shareholder returns amid evolving industry dynamics.

With analysts setting a consensus price target of US$79.5, the company trades at a 29.1% discount currently, suggesting potential for an upward price adjustment if revenue projections materialize as expected. This market positioning implies that successful execution of strategic initiatives could facilitate further share price appreciation, assuming earnings and margin forecasts reach anticipated levels.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:CNC

Centene

Operates as a healthcare enterprise that provides programs and services to under-insured and uninsured families, and commercial organizations in the United States.

Very undervalued with solid track record.

Similar Companies

Market Insights

Community Narratives