Advertisement

- United States

- /

- Healthcare Services

- /

- NYSE:CAH

Cardinal Health (CAH): Rethinking Valuation After a Strong Multi‑Month Share Price Rally

Simply Wall St

Reviewed by Simply Wall St

Cardinal Health (CAH) has quietly turned into a strong compounder, with the stock up around 69% year-to-date and roughly 34% over the past 3 months, drawing fresh attention from long term investors.

See our latest analysis for Cardinal Health.

That surge has come despite a recent pullback, with the 7 day share price return negative but the 30 day share price return still positive and the 3 year total shareholder return exceptionally strong. This signals momentum that is moderating rather than breaking.

If Cardinal Health’s run has you rethinking the healthcare space, this could be a good moment to explore other opportunities across healthcare stocks and see what else fits your strategy.

With Cardinal Health now flirting with analyst targets yet still trading at a steep implied discount to intrinsic value, investors face a pivotal question: is there still upside to capture, or is the market already pricing in its future growth?

Most Popular Narrative: 7% Undervalued

With Cardinal Health last closing at $199.71 against a narrative fair value of about $214.71, the story assumes more upside is still on the table.

The analysts have a consensus price target of $180.462 for Cardinal Health based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $203.0, and the most bearish reporting a price target of just $150.0.

Curious how modest margin expansion, steady revenue growth, and a rich future earnings multiple combine to justify that higher value? The crucial assumptions might surprise you.

Result: Fair Value of $214.71 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, tighter regulation on drug pricing and the potential loss of key customer contracts could quickly cap upside and challenge the current undervaluation story.

Find out about the key risks to this Cardinal Health narrative.

Another Angle on Valuation

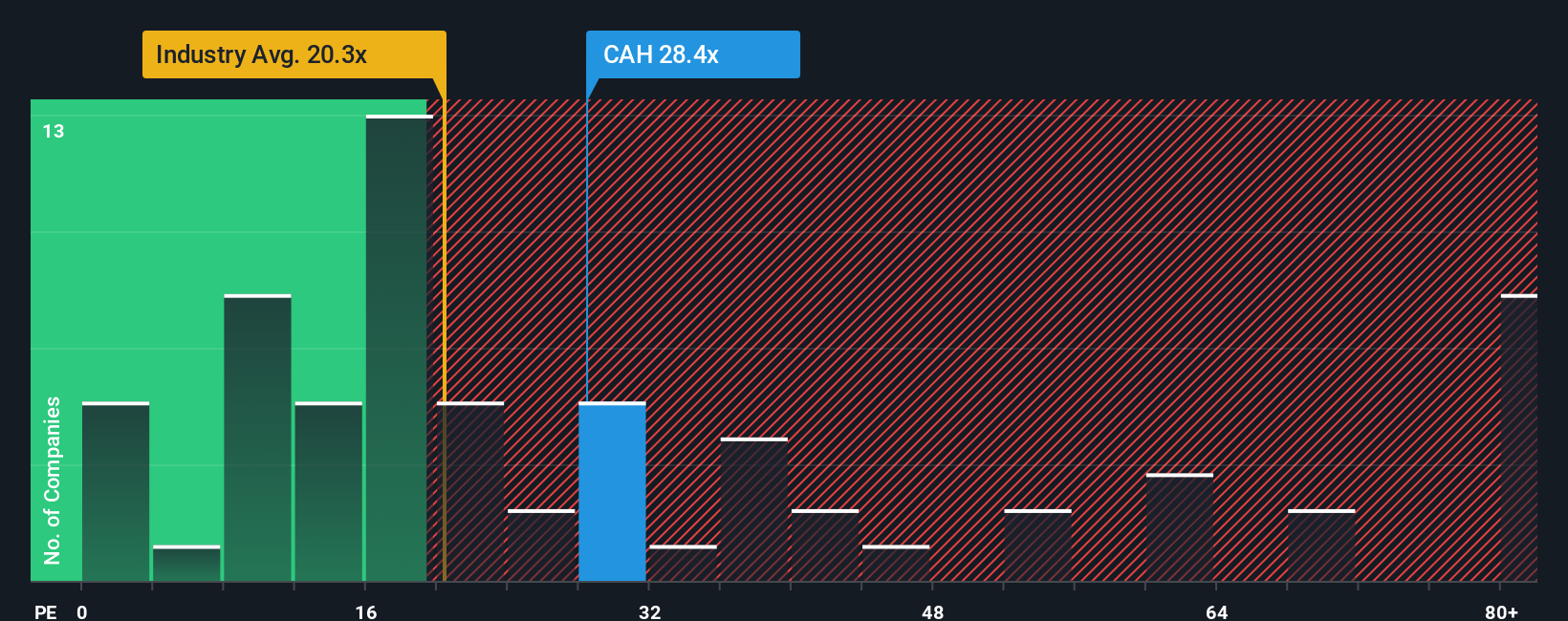

Multiples tell a more cautious story. Cardinal Health trades on a P/E of 29.7x, richer than peers at 26.2x and above its own fair ratio of 29.3x. That premium implies less margin for error, so how much execution risk are investors really willing to pay for?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Cardinal Health Narrative

If you would rather challenge these assumptions and dig into the numbers yourself, you can build a personalized view of Cardinal Health in minutes: Do it your way.

A great starting point for your Cardinal Health research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Ready for your next investing move?

Once you have weighed up Cardinal Health, do not stop there. Use the Simply Wall St screener to uncover fresh opportunities before the market catches on.

- Capture potential mispricings by targeting companies that look cheap on cash flow with these 920 undervalued stocks based on cash flows tailored to value focused investors.

- Ride powerful structural trends by zeroing in on innovators shaping the future of automation and intelligence through these 25 AI penny stocks.

- Strengthen your income strategy by focusing on reliable payouts and capital stability using these 14 dividend stocks with yields > 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:CAH

Cardinal Health

Operates as a healthcare services and products company in the United States and internationally.

Solid track record average dividend payer.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.4% undervalued

38 followersusers have followed this narrative

6 commentsusers have commented on this narrative

10 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$126.1% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$244.5% overvalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

FU

FundamentallySarcastic on Credit Corp Group ·

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Fair Value:AU$12.6411.4% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on Alphabet ·

Positioned globally, partnered locally

Fair Value:US$390.1918.1% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

JO

JohnJ on Worldline ·

When will fraudsters be investigated in depth. Fraud was ongoing in France too.

Fair Value:€0.5190.0% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

114 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3928.3% undervalued

952 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3406.0% undervalued

148 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative