Advertisement

- United States

- /

- Medical Equipment

- /

- NasdaqGM:TNDM

Shareholders May Be More Conservative With Tandem Diabetes Care, Inc.'s (NASDAQ:TNDM) CEO Compensation For Now

Key Insights

- Tandem Diabetes Care will host its Annual General Meeting on 21st of May

- Salary of US$732.0k is part of CEO John Sheridan's total remuneration

- Total compensation is 31% above industry average

- Tandem Diabetes Care's three-year loss to shareholders was 68% while its EPS was down 29% over the past three years

Shareholders of Tandem Diabetes Care, Inc. (NASDAQ:TNDM) will have been dismayed by the negative share price return over the last three years. In addition, the company's per-share earnings growth is not looking good, despite growing revenues. In light of this performance, shareholders will have a chance to question the board in the upcoming AGM on 21st of May, where they can impact on future company performance by voting on resolutions, including executive compensation. Here's why we think shareholders should hold off on a raise for the CEO at the moment.

See our latest analysis for Tandem Diabetes Care

How Does Total Compensation For John Sheridan Compare With Other Companies In The Industry?

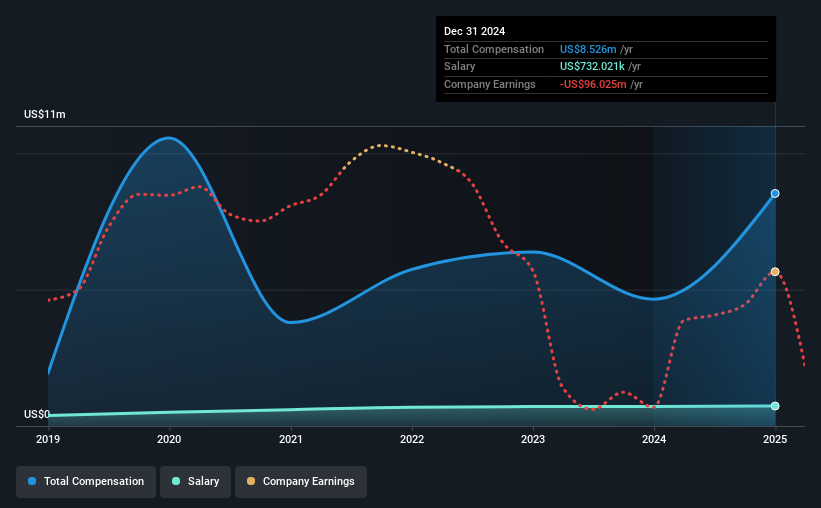

Our data indicates that Tandem Diabetes Care, Inc. has a market capitalization of US$1.5b, and total annual CEO compensation was reported as US$8.5m for the year to December 2024. We note that's an increase of 83% above last year. We think total compensation is more important but our data shows that the CEO salary is lower, at US$732k.

In comparison with other companies in the American Medical Equipment industry with market capitalizations ranging from US$1.0b to US$3.2b, the reported median CEO total compensation was US$6.5m. This suggests that John Sheridan is paid more than the median for the industry. What's more, John Sheridan holds US$1.8m worth of shares in the company in their own name.

| Component | 2024 | 2023 | Proportion (2024) |

| Salary | US$732k | US$711k | 9% |

| Other | US$7.8m | US$3.9m | 91% |

| Total Compensation | US$8.5m | US$4.7m | 100% |

Speaking on an industry level, nearly 25% of total compensation represents salary, while the remainder of 75% is other remuneration. In Tandem Diabetes Care's case, non-salary compensation represents a greater slice of total remuneration, in comparison to the broader industry. It's important to note that a slant towards non-salary compensation suggests that total pay is tied to the company's performance.

Tandem Diabetes Care, Inc.'s Growth

Over the last three years, Tandem Diabetes Care, Inc. has shrunk its earnings per share by 29% per year. It achieved revenue growth of 28% over the last year.

Investors would be a bit wary of companies that have lower EPS On the other hand, the strong revenue growth suggests the business is growing. It's hard to reach a conclusion about business performance right now. This may be one to watch. Moving away from current form for a second, it could be important to check this free visual depiction of what analysts expect for the future.

Has Tandem Diabetes Care, Inc. Been A Good Investment?

With a total shareholder return of -68% over three years, Tandem Diabetes Care, Inc. shareholders would by and large be disappointed. So shareholders would probably want the company to be less generous with CEO compensation.

To Conclude...

The loss to shareholders over the past three years is certainly concerning and possibly has something to do with the fact that the company's earnings haven't grown. In the upcoming AGM, shareholders will get the opportunity to discuss any issues with the board, including those related to CEO remuneration and assess if the board's plan is in line with their expectations.

While CEO pay is an important factor to be aware of, there are other areas that investors should be mindful of as well. We did our research and spotted 1 warning sign for Tandem Diabetes Care that investors should look into moving forward.

Of course, you might find a fantastic investment by looking at a different set of stocks. So take a peek at this free list of interesting companies.

Valuation is complex, but we're here to simplify it.

Discover if Tandem Diabetes Care might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGM:TNDM

Tandem Diabetes Care

Designs, develops, and commercializes technology solutions for people living with diabetes in the United States and internationally.

Adequate balance sheet and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

Apple: A Dying Star with an Overpriced Valuation

Fair Value US$177.34|19.1% overvalued

IN

Community Contributor

Avino a case for USD$20 per share within 5 years (assuming $3,500 gold, $100 silver and $4 copper).

Fair Value CA$26.79|86.0% undervalued

AG

Community Contributor

Riding the Defense Boom RENK Sees Revenue Climb at 15% CAGR by FY 2029

Fair Value €69.87|14.3% undervalued

CH

Community Contributor