- United States

- /

- Medical Equipment

- /

- NasdaqGS:ALGN

Align Technology (ALGN) Margin Drop Reinforces Bearish Narratives Despite Turnaround Forecasts

Reviewed by Simply Wall St

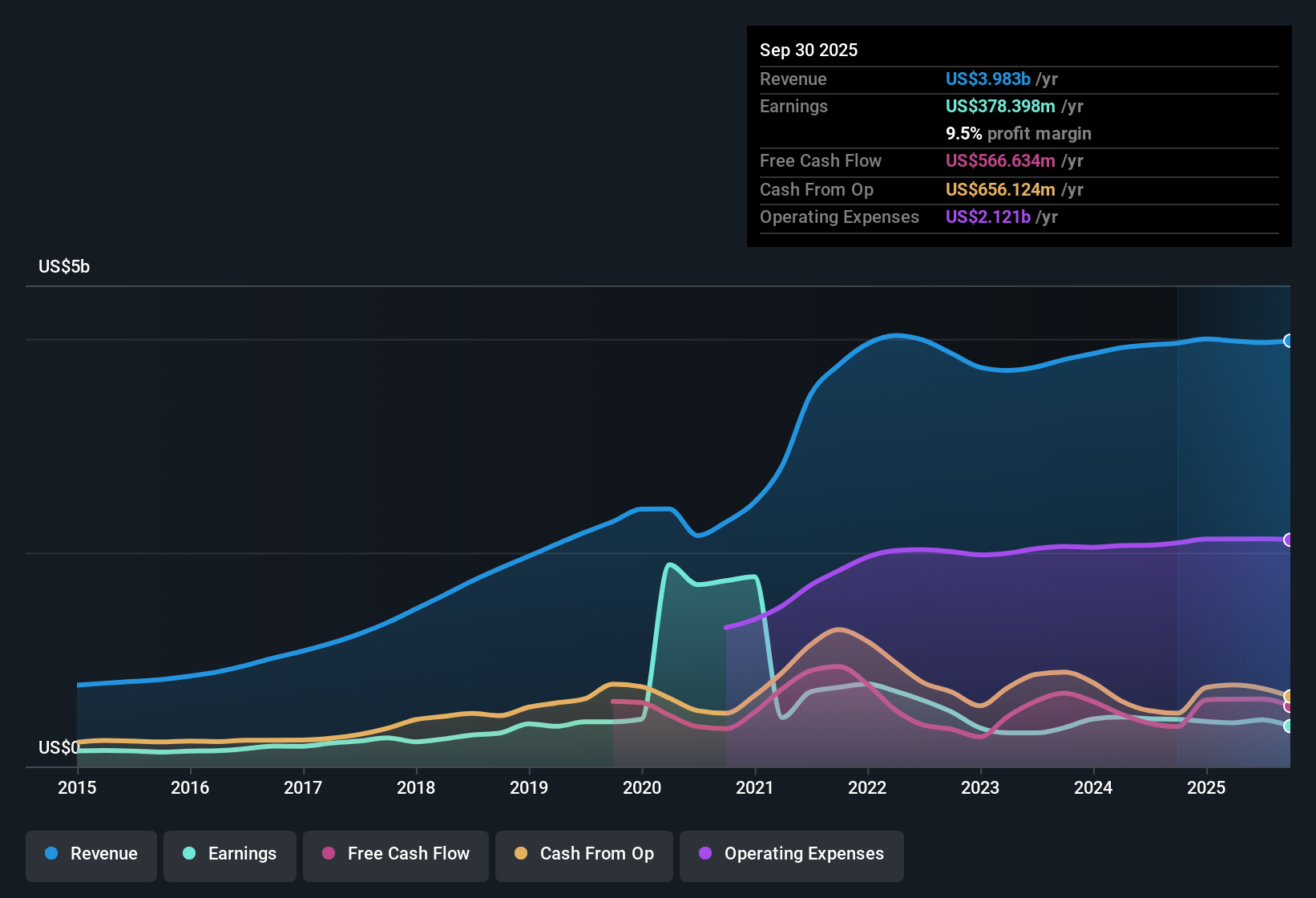

Align Technology (ALGN) has faced a challenging five-year stretch, with reported earnings declining by 28.3% annually and the current net profit margin at 9.5%, down from last year’s 11.1%. Looking forward, earnings are forecast to rebound at an 18.1% annual rate, above the broader US market’s 15.7% projection. However, revenue growth expectations remain muted at 4.8% compared to the market’s 10.3%. Despite the recent margin pressure, investors may find encouragement in forecasts for profit growth and valuation levels that appear favorable relative to both industry peers and analyst targets.

See our full analysis for Align Technology.Now, let's see how these earnings numbers compare with the leading narratives shaping investor sentiment. Some perspectives may find support, while others could be put to the test.

See what the community is saying about Align Technology

Margin Pressure Intensifies as Net Profit Falls to 9.5%

- Align Technology's net profit margin has dropped to 9.5%, down from 11.1% the previous year, highlighting ongoing profitability challenges that extend beyond the headline earnings decline.

- Analysts’ consensus view maintains that macroeconomic headwinds, a greater mix of lower-priced aligners, and tougher competition continue to put downward pressure on net margins and overall profitability.

- Consensus narrative notes that strategic investments in digital workflows and automation could restore margins in the coming years, but near-term pressures from less profitable product lines remain substantial.

- Bears in the consensus point out that shifting orthodontic preferences and sluggish scanner sales may keep margins and earnings from rebounding as quickly as forecast.

- Recent analyst expectations suggest profit margins could rebound to 14.9% in three years, but this would require both operational improvements and steadier demand for premium products.

Consensus narrative highlights how margin recovery is possible, but far from assured, as headwinds from product mix and competition linger. 📊 Read the full Align Technology Consensus Narrative.

Share Price Lags Analyst Targets Despite Value Signals

- At $138.13, Align Technology's current share price stands 22.8% below the analyst target price of $179.07, and trades at a P/E of 26.5x, which is lower than both industry (28x) and peer averages (30.3x).

- Consensus narrative argues that while discounted valuation and a 27.1% upside to analyst targets look appealing, diverging analyst estimates (ranging from $140 to $220 per share) introduce uncertainty about whether future growth will justify even the consensus price.

- Consensus also points out the “fair value” from discounted cash flow sits much higher at $316.46, but investors have not rewarded growth forecasts with a higher multiple yet.

- Bulls in the consensus see margin expansion and global adoption as catalysts for valuation catch-up; skeptics cite stagnant revenue growth versus industry averages as a near-term anchor.

Revenue Growth Trails Market, Denting Long-Term Upside

- Align’s revenue is projected to grow at 4.8% per year, well below the US market's average of 10.3% annually, even as earnings forecasts outpace the market.

- According to the analysts’ consensus view, new clinical indications and international expansion are expected to be the primary levers for future sales and profit growth.

- Consensus narrative underscores that robust demand in markets like APAC and EMEA has potential, but success depends on broadening product appeal and improving conversion rates through digital engagement.

- Cautious analysts emphasize that product mix shift to lower-priced offerings and weak equipment demand are still constraining top-line momentum.

Next Steps

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Align Technology on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Notice something in the data that stands out to you? Share your take and shape your unique investment story in just a few minutes. Do it your way

A great starting point for your Align Technology research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

See What Else Is Out There

Despite promising earnings recovery forecasts, Align Technology’s muted revenue growth and volatile margins raise concerns about its ability to deliver consistent long-term gains.

If you crave more predictable performance, use our stable growth stocks screener (2113 results) screener to focus on companies that have demonstrated they can grow revenues and earnings steadily in varying market conditions.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:ALGN

Align Technology

Provides Invisalign clear aligners, Vivera retainers, and iTero intraoral scanners and services in the United States, Switzerland, and internationally.

Flawless balance sheet and slightly overvalued.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Sunrun Stock: When the Energy Transition Collides With the Cost of Capital

Salesforce Stock: AI-Fueled Growth Is Real — But Can Margins Stay This Strong?

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)