Advertisement

The board of Turning Point Brands, Inc. (NYSE:TPB) has announced that it will pay a dividend on the 6th of October, with investors receiving $0.065 per share. Including this payment, the dividend yield on the stock will be 1.0%, which is a modest boost for shareholders' returns.

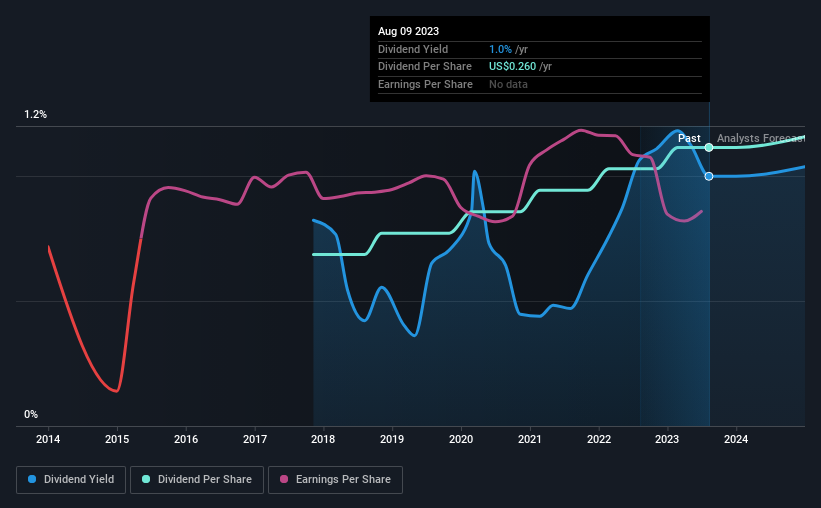

View our latest analysis for Turning Point Brands

Turning Point Brands' Payment Has Solid Earnings Coverage

If it is predictable over a long period, even low dividend yields can be attractive. However, prior to this announcement, Turning Point Brands' dividend was comfortably covered by both cash flow and earnings. As a result, a large proportion of what it earned was being reinvested back into the business.

The next year is set to see EPS grow by 62.3%. Assuming the dividend continues along recent trends, we think the payout ratio could be 25% by next year, which is in a pretty sustainable range.

Turning Point Brands Doesn't Have A Long Payment History

Turning Point Brands' dividend has been pretty stable for a little while now, but we will continue to be cautious until it has been demonstrated for a few more years. Since 2017, the dividend has gone from $0.16 total annually to $0.26. This implies that the company grew its distributions at a yearly rate of about 8.4% over that duration. Investors will likely want to see a longer track record of growth before making decision to add this to their income portfolio.

Dividend Growth May Be Hard To Come By

The company's investors will be pleased to have been receiving dividend income for some time. However, things aren't all that rosy. In the last five years, Turning Point Brands' earnings per share has shrunk at approximately 9.8% per annum. If earnings continue declining, the company may have to make the difficult choice of reducing the dividend or even stopping it completely - the opposite of dividend growth. It's not all bad news though, as the earnings are predicted to rise over the next 12 months - we would just be a bit cautious until this can turn into a longer term trend.

In Summary

In summary, while it's good to see that the dividend hasn't been cut, we are a bit cautious about Turning Point Brands' payments, as there could be some issues with sustaining them into the future. The company is generating plenty of cash, which could maintain the dividend for a while, but the track record hasn't been great. We would probably look elsewhere for an income investment.

Market movements attest to how highly valued a consistent dividend policy is compared to one which is more unpredictable. Still, investors need to consider a host of other factors, apart from dividend payments, when analysing a company. Just as an example, we've come across 3 warning signs for Turning Point Brands you should be aware of, and 1 of them can't be ignored. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

Valuation is complex, but we're here to simplify it.

Discover if Turning Point Brands might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:TPB

Turning Point Brands

Manufactures, markets, and distributes branded consumer products in the United States and Canada.

Reasonable growth potential with proven track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

Pole position to benefit from GENIUS Act

Fair Value US$233.04|58.8% undervalued

CH

Community Contributor

IREN will transform from bitcoin miner to leader in AI infrastructure

Fair Value US$21.48|11.6% undervalued

KA

Community Contributor

Behind the Assay: XRF Scientific’s Role in Modern Mining Economics

Fair Value AU$2.10|0% overvalued

RO

Community Contributor