- United States

- /

- Food

- /

- NYSE:K

Shareholders Will Most Likely Find Kellanova's (NYSE:K) CEO Compensation Acceptable

Key Insights

- Kellanova will host its Annual General Meeting on 26th of April

- Salary of US$1.34m is part of CEO Steve Cahillane's total remuneration

- Total compensation is similar to the industry average

- Kellanova's total shareholder return over the past three years was 7.8% while its EPS was down 15% over the past three years

The share price of Kellanova (NYSE:K) has been growing in the past few years, however, the per-share earnings growth has been lacking, suggesting something is amiss. These concerns will be at the front of shareholders' minds as they go into the AGM coming up on 26th of April. One way that shareholders can influence managerial decisions is through voting on CEO and executive remuneration packages, which studies show could impact company performance. From what we gathered, we think shareholders should be wary of raising CEO compensation until the company shows some marked improvement.

See our latest analysis for Kellanova

Comparing Kellanova's CEO Compensation With The Industry

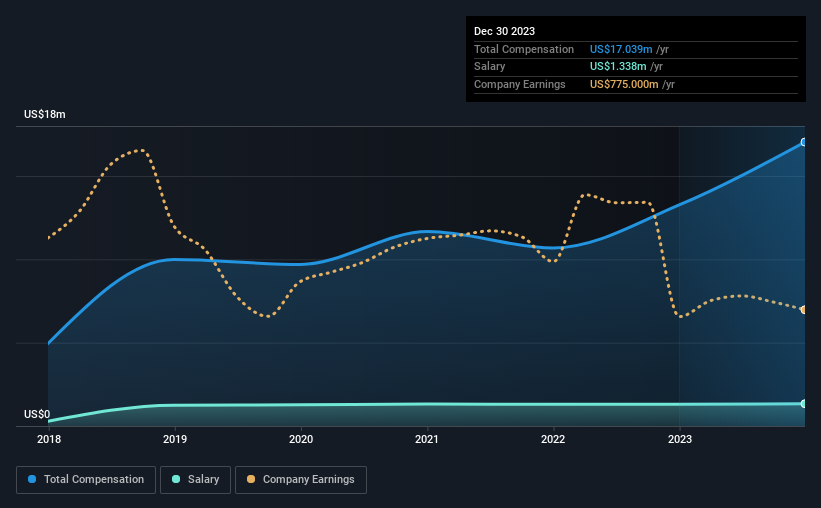

At the time of writing, our data shows that Kellanova has a market capitalization of US$20b, and reported total annual CEO compensation of US$17m for the year to December 2023. That's a notable increase of 28% on last year. We think total compensation is more important but our data shows that the CEO salary is lower, at US$1.3m.

In comparison with other companies in the American Food industry with market capitalizations over US$8.0b, the reported median total CEO compensation was US$16m. From this we gather that Steve Cahillane is paid around the median for CEOs in the industry. Furthermore, Steve Cahillane directly owns US$21m worth of shares in the company, implying that they are deeply invested in the company's success.

| Component | 2023 | 2022 | Proportion (2023) |

| Salary | US$1.3m | US$1.3m | 8% |

| Other | US$16m | US$12m | 92% |

| Total Compensation | US$17m | US$13m | 100% |

On an industry level, around 21% of total compensation represents salary and 79% is other remuneration. Kellanova sets aside a smaller share of compensation for salary, in comparison to the overall industry. If non-salary compensation dominates total pay, it's an indicator that the executive's salary is tied to company performance.

Kellanova's Growth

Over the last three years, Kellanova has shrunk its earnings per share by 15% per year. It achieved revenue growth of 3.5% over the last year.

Few shareholders would be pleased to read that EPS have declined. The modest increase in revenue in the last year isn't enough to make us overlook the disappointing change in EPS. It's hard to argue the company is firing on all cylinders, so shareholders might be averse to high CEO remuneration. Moving away from current form for a second, it could be important to check this free visual depiction of what analysts expect for the future.

Has Kellanova Been A Good Investment?

With a total shareholder return of 7.8% over three years, Kellanova has done okay by shareholders, but there's always room for improvement. As a result, investors in the company might be reluctant about agreeing to increase CEO pay in the future, before seeing an improvement on their returns.

To Conclude...

Despite the positive returns on shareholders' investments, the fact that earnings have failed to grow makes us skeptical about whether these returns will continue. In the upcoming AGM, shareholders will get the opportunity to discuss any concerns with the board, including those related to CEO remuneration and assess if the board's plan will likely improve performance in the future.

While CEO pay is an important factor to be aware of, there are other areas that investors should be mindful of as well. We've identified 2 warning signs for Kellanova that investors should be aware of in a dynamic business environment.

Switching gears from Kellanova, if you're hunting for a pristine balance sheet and premium returns, this free list of high return, low debt companies is a great place to look.

Valuation is complex, but we're here to simplify it.

Discover if Kellanova might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:K

Kellanova

Manufactures and markets snacks and convenience foods in North America, Europe, Latin America, the Asia Pacific, the Middle East, Australia, and Africa.

Established dividend payer with proven track record.