Advertisement

- United States

- /

- Food

- /

- NYSE:HSY

Does Hershey Stock Still Offer Upside After Recent Price Swings And Cost Pressure Concerns?

Simply Wall St

Reviewed by Bailey Pemberton

- Wondering if Hershey at around $180 a share is still a sweet deal or if the best days are already priced in? In this article, we unpack what the current market price might be signaling about potential future returns.

- After a choppy stretch that left the stock down 4.0% over the last week but up 11.3% in the past month and 7.0% year to date, Hershey now sits only modestly above its 1 year gain of 4.9%. The stock is still nursing a 17.3% drop over 3 years, even with a 33.7% gain over 5 years.

- Recent headlines have focused on shifting consumer preferences toward premium and healthier snacks, as well as ongoing input cost pressures that could squeeze margins if not managed carefully. At the same time, Hershey has been in the news for strategic brand investments and portfolio changes intended to keep it relevant on store shelves and in e commerce channels.

- On our framework of 6 valuation checks, Hershey is currently undervalued in 0. This gives it a valuation score of 0/6. Below, we walk through what different valuation approaches say about that score and then finish with a more holistic way to think about what the stock might really be worth.

Hershey scores just 0/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Hershey Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model estimates what a business is worth by projecting the cash it can generate in the future, then discounting those cash flows back to today’s dollars.

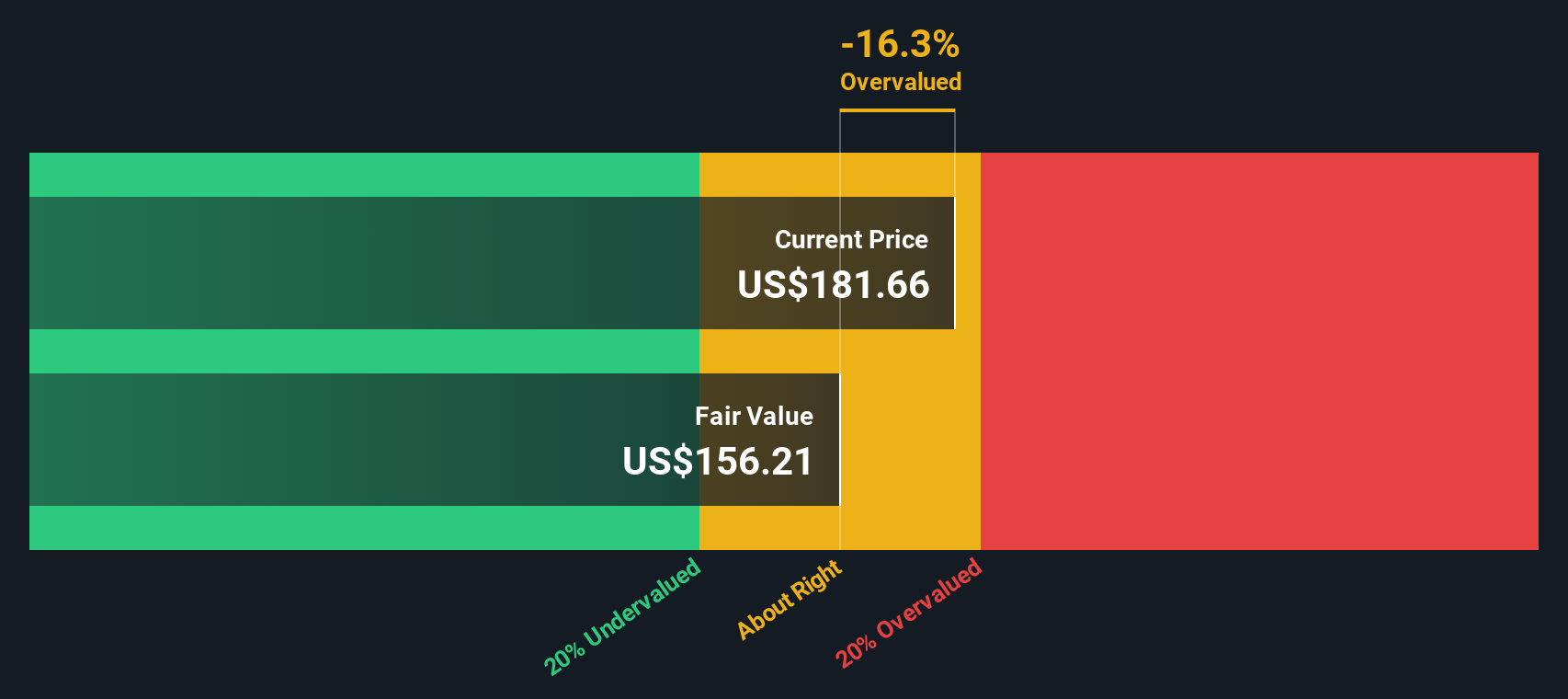

For Hershey, the latest twelve month Free Cash Flow is about $1.59 billion. Analysts provide detailed forecasts for the next few years, and beyond that, Simply Wall St extrapolates the trajectory, resulting in an estimated Free Cash Flow of around $1.59 billion in 2035. These projected cash flows are discounted using a required return to arrive at an intrinsic value per share.

On this basis, the DCF model points to an estimated fair value of roughly $163.04 per share. With the stock currently trading near $180, the model implies Hershey is about 10.8% overvalued. This suggests the market is pricing in slightly more optimism than the cash flow outlook alone would justify.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Hershey may be overvalued by 10.8%. Discover 915 undervalued stocks or create your own screener to find better value opportunities.

Approach 2: Hershey Price vs Earnings

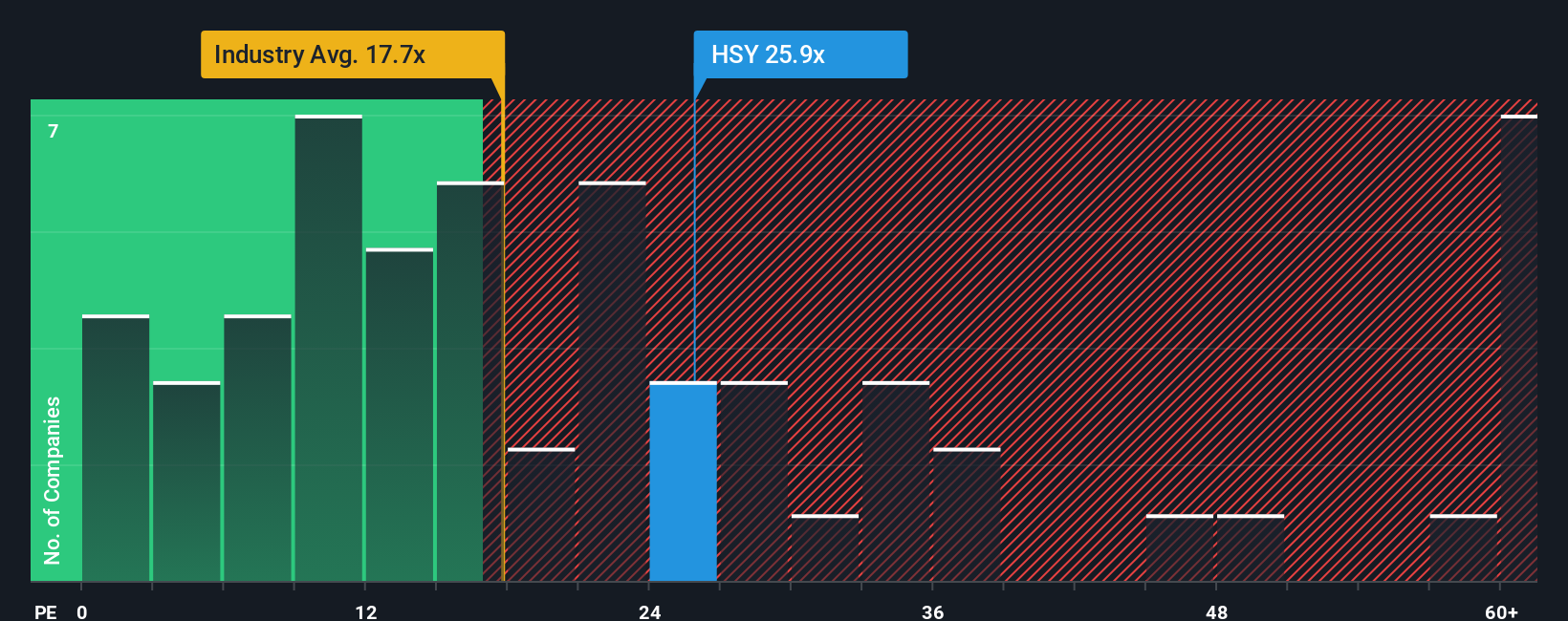

For a mature, consistently profitable business like Hershey, the Price to Earnings (PE) ratio is a useful way to gauge whether investors are paying a sensible price for each dollar of earnings. The higher the expected growth and the lower the perceived risk, the more investors are typically willing to pay in the form of a higher PE multiple.

Hershey currently trades on a PE of about 26.9x, which is above both the broader Food industry average of around 20.5x and the peer group average of roughly 23.5x. Simply Wall St also calculates a proprietary Fair Ratio of 23.0x for Hershey, which reflects what investors might reasonably pay given its earnings growth outlook, margins, industry, size and risk profile.

This Fair Ratio is more informative than a simple comparison with peers or the industry, because it adjusts for Hershey specific fundamentals instead of assuming all companies deserve similar multiples. With the stock trading at 26.9x versus a Fair Ratio of 23.0x, the PE lens suggests the market is assigning Hershey a premium that looks somewhat rich relative to its fundamentals.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1443 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Hershey Narrative

Earlier we mentioned that there is an even better way to understand valuation. Let us introduce you to Narratives, an easy tool on Simply Wall St’s Community page that lets you connect your view of a company’s story with a specific forecast for revenue, earnings, margins and, ultimately, a fair value you can compare against today’s price to help inform your decision. These Narratives update dynamically as new news or earnings arrive and allow, for example, one Hershey investor to build a bullish narrative that aligns with a fair value near the upper end of Street targets around $211 based on successful tariff mitigation, innovation and snack diversification. Another, more cautious investor might create a bearish narrative that aligns with a fair value closer to $123 if they expect prolonged cocoa cost pressure, weaker demand and tougher competition to weigh on growth and profitability.

Do you think there's more to the story for Hershey? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Hershey might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:HSY

Hershey

Engages in the manufacture and sale of confectionery products and pantry items in the United States and internationally.

Established dividend payer with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.4% undervalued

41 followersusers have followed this narrative

6 commentsusers have commented on this narrative

12 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$123.8% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$244.5% overvalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

SC

scm on Text ·

TXT will see revenue grow 26% with a profit margin boost of almost 40%

Fair Value:zł8048.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VL

Vladislav on Galleon Gold ·

Significantly undervalued gold explorer in Timmins, finally getting traction

Fair Value:CA$482.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

FU

FundamentallySarcastic on Credit Corp Group ·

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Fair Value:AU$12.6411.8% overvalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

115 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3928.3% undervalued

954 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3406.0% undervalued

147 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative