- United States

- /

- Food

- /

- NYSE:GIS

Has General Mills’ 26% Share Price Slide in 2025 Created an Opportunity?

Reviewed by Bailey Pemberton

- Wondering if General Mills at around $46.69 is a bargain hiding in plain sight or a classic value trap in the making? This article is designed to help you figure that out with a clear, valuation-first lens.

- Despite a modest 1.7% gain over the last 7 days and a flat 0.4% over 30 days, the stock is still down a steep 26.5% year to date and 26.8% over the last year, which naturally raises questions about whether sentiment has overshot the fundamentals.

- Recently, investors have been rethinking classic consumer staples as higher rates, shifting consumer preferences and retailer dynamics put pressure on traditional packaged food companies, and General Mills has been caught up in that broader rotation. At the same time, management’s ongoing focus on portfolio optimization, cost discipline and brand investment has kept the long term cash generation story very much alive.

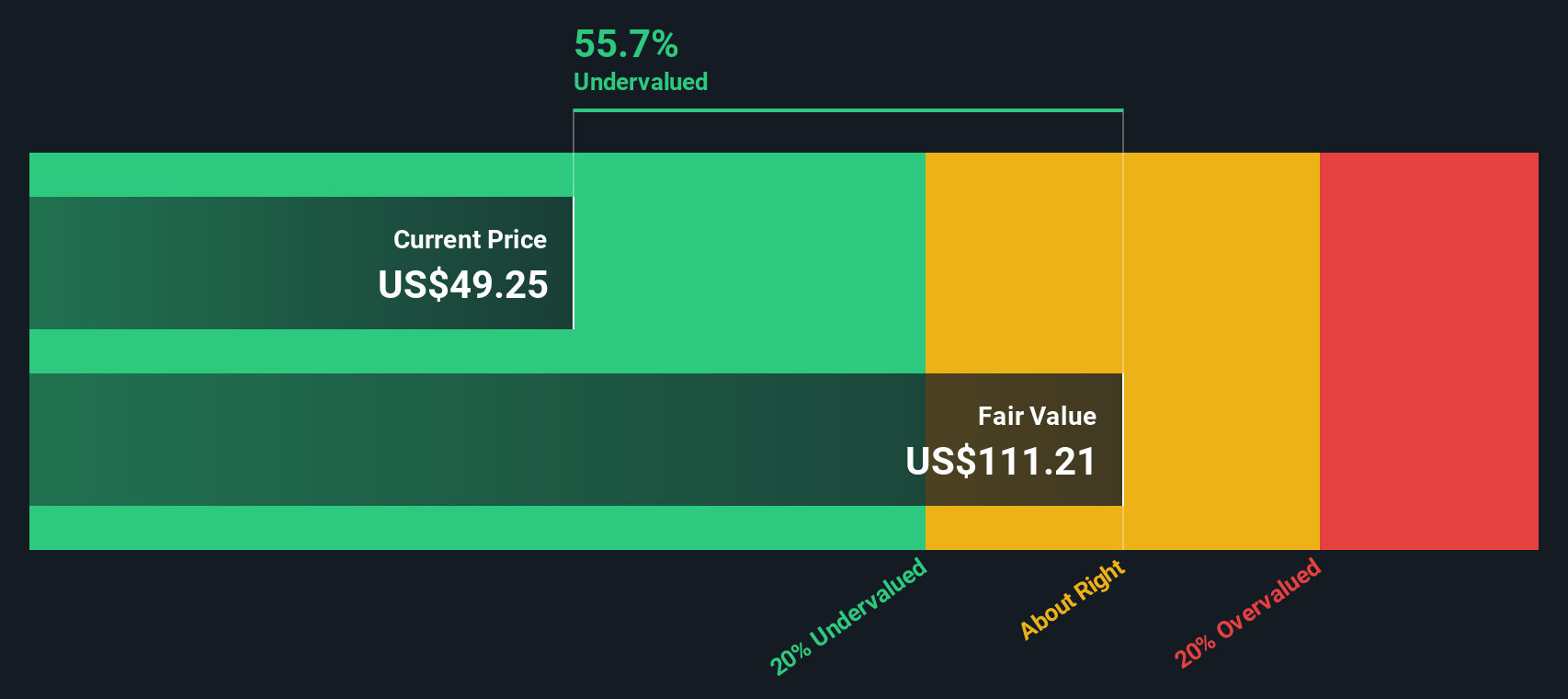

- On our checks, General Mills scores a solid 5/6 valuation score, suggesting it screens as undervalued on most of the metrics that matter. Next, we will walk through those individual valuation approaches, before finishing with an even more powerful way to think about what the stock is really worth.

Find out why General Mills's -26.8% return over the last year is lagging behind its peers.

Approach 1: General Mills Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model estimates what a business is worth by projecting the cash it can generate in the future, then discounting those cash flows back to today in $ terms.

For General Mills, the latest twelve month Free Cash Flow sits at about $2.0 billion, and analysts expect this to rise steadily as the company grows earnings and improves efficiency. Based on a 2 Stage Free Cash Flow to Equity model, analyst forecasts drive the next few years of cash flows. Beyond that point, Simply Wall St extrapolates the trend, with projected Free Cash Flow reaching roughly $2.3 billion by 2029 and continuing to edge higher thereafter.

When all those future $ cash flows are discounted back to today, the model arrives at an intrinsic value of roughly $104.11 per share. Compared with a current share price around $46.69, the DCF suggests the stock is trading at about a 55.2% discount to its estimated fair value, which represents a substantial valuation gap.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests General Mills is undervalued by 55.2%. Track this in your watchlist or portfolio, or discover 907 more undervalued stocks based on cash flows.

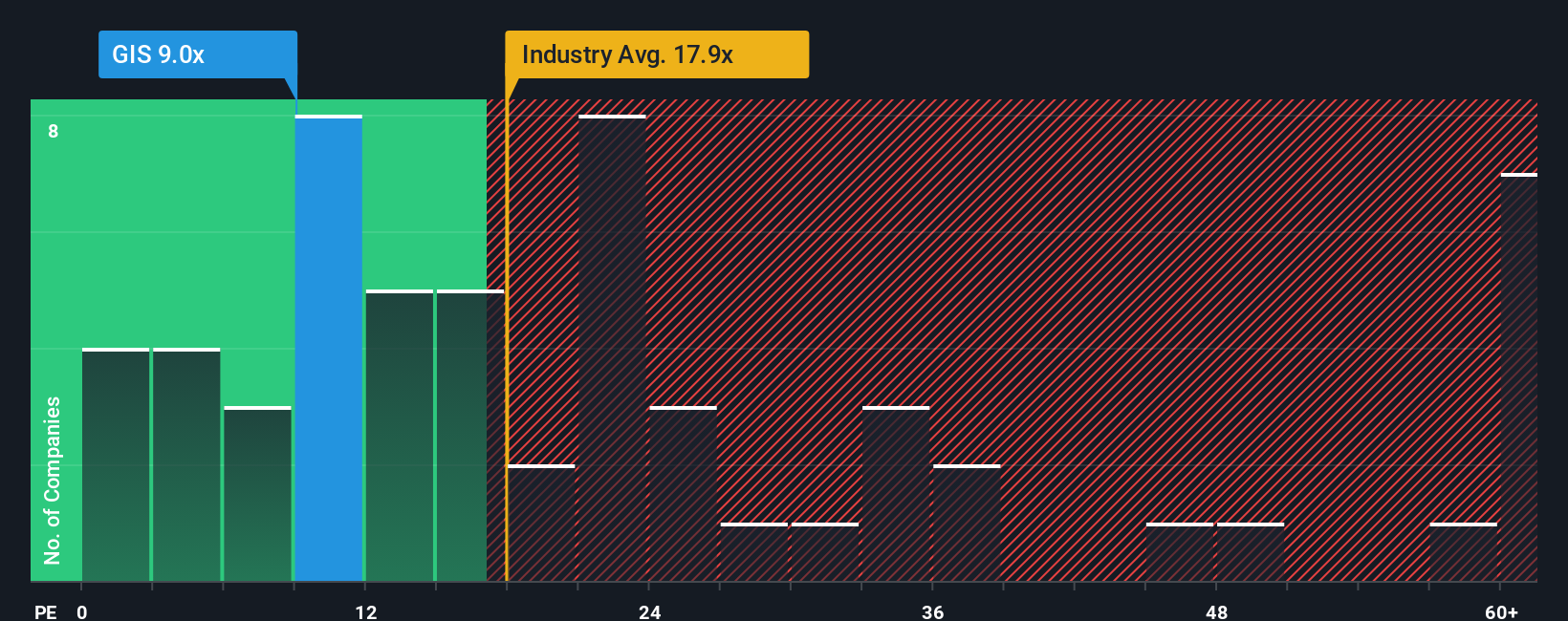

Approach 2: General Mills Price vs Earnings

For profitable, established companies like General Mills, the Price to Earnings, or PE, ratio is often a clear way to judge valuation because it links what investors pay today to the earnings the business is actually generating.

In practice, growth expectations and risk profile play a significant role in setting what a normal or fair PE should look like. Faster, more resilient growers tend to justify higher PE ratios, while slower or riskier businesses typically trade on lower multiples.

General Mills currently trades on a PE of about 8.6x, which is well below the Food industry average of roughly 20.2x and the broader peer group, which sits near 24.5x. To move beyond simple comparisons, Simply Wall St also calculates a Fair Ratio. This is a proprietary PE estimate that reflects the company’s specific earnings growth outlook, profit margins, risk characteristics, industry positioning and market cap. This can be more informative than looking at peers alone because it adjusts for the fact that not all food companies have the same quality or growth prospects.

For General Mills, the Fair Ratio is around 12.3x. Compared with the current 8.6x multiple, this suggests the shares may be undervalued on an earnings basis.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1448 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your General Mills Narrative

Earlier we mentioned that there is an even better way to understand valuation. Let us introduce you to Narratives, a simple framework on Simply Wall St’s Community page where you connect your view of General Mills’ story to a specific forecast for its future revenue, earnings and margins. This then rolls up into your own fair value estimate and a clear stance by comparing that fair value to today’s price. Everything updates dynamically as new information like earnings or news comes in. For example, one investor might build a cautious General Mills Narrative around modestly declining revenue, slightly lower margins and a fair value near $45, while another leans into improving volume trends, gradual margin recovery and a fair value closer to $63. Both can then see at a glance whether the current price makes the stock look attractively undervalued or too expensive relative to the future they believe is most likely.

Do you think there's more to the story for General Mills? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:GIS

6 star dividend payer and undervalued.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

A tech powerhouse quietly powering the world’s AI infrastructure.

Keppel DC REIT (SGX: AJBU) is a resilient gem in the data center space.

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)