As with many other companies, PepsiCo, Inc. (NASDAQ:PEP) makes use of debt. We want to evaluate the risk and burden of debt.

As many investors know, debt can be used productively to fund profitable projects and establish a resilient capital structure, however if mismanaged, debt can be a burden and a significant risk to a company.

Debt financing is especially available and effective for older companies like PepsiCo, which have a multitude of assets and regular cash flows they can use to guarantee debt repayments.

PepsiCo has recently announced a 5% increase of quarterly dividend payments to US$1.075 per share, and we want to know if this is sustainable in the long run.

How Much Debt Does PepsiCo Carry?

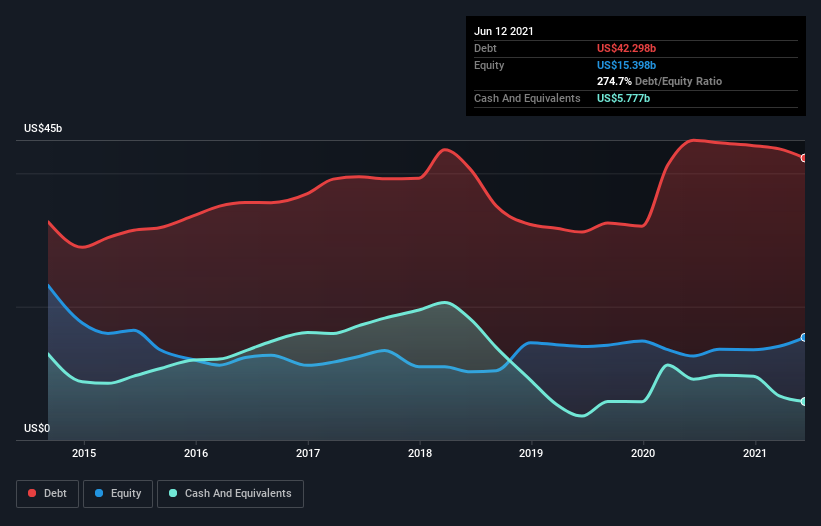

As you can see below, PepsiCo had US$40.6b of debt at June 2021, down from US$45.0b a year prior. On the flip side, it has US$5.78b in cash leading to net debt of about US$34.8b.

View our latest analysis for PepsiCo

A Look At PepsiCo's Liabilities

The latest balance sheet data shows that PepsiCo had liabilities of US$23.6b due within a year, and liabilities of US$53.4b falling due after that.

On the other hand, it had cash of US$5.78b and US$9.72b worth of receivables due within a year. So, its liabilities total US$61.5b more than the combination of its cash and short-term receivables.

This deficit isn't so bad because PepsiCo is worth a massive US$214.6b, and thus could probably raise enough capital to shore up its balance sheet.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover).

PepsiCo has a debt to EBITDA ratio of 2.5, which signals significant debt, but is still pretty reasonable for most types of business.

Its EBIT was about 11.4 times its interest expense, implying the company isn't really paying a high cost to maintain that level of debt.

Finally, a company can only pay off debt with cash, not profit. So we always check how much of that EBIT is translated into free cash flow. During the last three years, PepsiCo produced sturdy free cash flow equating to 58% of its EBIT, a reasonable portion. This cold hard cash means it can reduce its debt when it wants to.

Are Dividend Payment Threatened by Debt

PepsiCo is also notable for paying a 2.77% dividend to its shareholders, while this yield might not be spectacular, a stable company is sometimes the better option for investors.

Comparing dividend payments to a company's net profit after tax is a simple way of reality-checking whether a dividend is sustainable. In the last year, PepsiCo paid out 70% of its profit as dividends. Which means that PepsiCo is earning enough to afford dividends.

We also look at the percentage of free cash flows used to cover dividend payments and found that PepsiCo used 80% of its free cash flows to cover dividend payments.

The key point here is that the company seems quite able to cover dividends both by earnings and cash flows. Importantly, they are not reaching into debt issuance or asset selling to cover these expenses - which means dividend payments are not currently a risk for an increase in debt.

Conclusion

With a 247% debt to equity ratio, it is normal for shareholders to be taken a back at first glance, but the company has enough capacity and capital to stably manage its operations while reliably making dividend payments.

PepsiCo's 11.4x interest coverage ratio suggests it can regularly cover handle its debt.

The company is also making enough profit and free cash flows that it can allocate to shareholder dividends.

The sheer US$214b market cap of PepsiCo, allows it to raise enough capital if it needed to resolve some outstanding debt.

Of course, while this leverage can enhance returns on equity, it does bring more risk, so it's worth keeping an eye on this one. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. These risks can be hard to spot. Every company has them, and we've spotted 2 warning signs for PepsiCo you should know about.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Goran Damchevski and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Goran Damchevski

Goran is an Equity Analyst and Writer at Simply Wall St with over 5 years of experience in financial analysis and company research. Goran previously worked in a seed-stage startup as a capital markets research analyst and product lead and developed a financial data platform for equity investors.

About NasdaqGS:PEP

PepsiCo

Engages in the manufacture, marketing, distribution, and sale of various beverages and convenient foods worldwide.

Good value with proven track record and pays a dividend.

Similar Companies

Market Insights

Community Narratives