- United States

- /

- Energy Services

- /

- NYSE:SEI

Solaris Oilfield Infrastructure (NYSE:SOI) Will Pay A Larger Dividend Than Last Year At $0.12

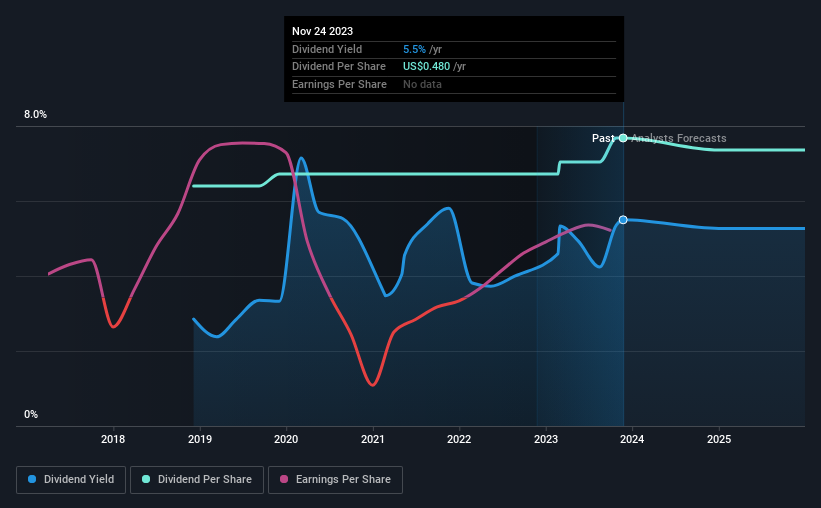

The board of Solaris Oilfield Infrastructure, Inc. (NYSE:SOI) has announced that it will be paying its dividend of $0.12 on the 11th of December, an increased payment from last year's comparable dividend. This takes the dividend yield to 5.5%, which shareholders will be pleased with.

See our latest analysis for Solaris Oilfield Infrastructure

Solaris Oilfield Infrastructure's Earnings Easily Cover The Distributions

While it is great to have a strong dividend yield, we should also consider whether the payment is sustainable. The last payment was quite easily covered by earnings, but it made up 186% of cash flows. While the company may be more focused on returning cash to shareholders than growing the business at this time, we think that a cash payout ratio this high might expose the dividend to being cut if the business ran into some challenges.

The next year is set to see EPS grow by 64.5%. Assuming the dividend continues along recent trends, we think the payout ratio could be 39% by next year, which is in a pretty sustainable range.

Solaris Oilfield Infrastructure Doesn't Have A Long Payment History

It is great to see that Solaris Oilfield Infrastructure has been paying a stable dividend for a number of years now, however we want to be a bit cautious about whether this will remain true through a full economic cycle. The annual payment during the last 5 years was $0.40 in 2018, and the most recent fiscal year payment was $0.48. This means that it has been growing its distributions at 3.7% per annum over that time. Modest dividend growth is good to see, especially with the payments being relatively stable. However, the payment history is relatively short and we wouldn't want to rely on this dividend too much.

Solaris Oilfield Infrastructure May Find It Hard To Grow The Dividend

Investors could be attracted to the stock based on the quality of its payment history. Let's not jump to conclusions as things might not be as good as they appear on the surface. Over the past five years, it looks as though Solaris Oilfield Infrastructure's EPS has declined at around 4.4% a year. Declining earnings will inevitably lead to the company paying a lower dividend in line with lower profits. However, the next year is actually looking up, with earnings set to rise. We would just wait until it becomes a pattern before getting too excited.

The Dividend Could Prove To Be Unreliable

Overall, we always like to see the dividend being raised, but we don't think Solaris Oilfield Infrastructure will make a great income stock. While the low payout ratio is a redeeming feature, this is offset by the minimal cash to cover the payments. We would probably look elsewhere for an income investment.

Companies possessing a stable dividend policy will likely enjoy greater investor interest than those suffering from a more inconsistent approach. Still, investors need to consider a host of other factors, apart from dividend payments, when analysing a company. For instance, we've picked out 2 warning signs for Solaris Oilfield Infrastructure that investors should take into consideration. If you are a dividend investor, you might also want to look at our curated list of high yield dividend stocks.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:SEI

Solaris Energy Infrastructure

Designs and manufactures specialized equipment for oil and natural gas operators in the United States.

Medium-low with high growth potential.

Similar Companies

Market Insights

Community Narratives