Advertisement

- United States

- /

- Oil and Gas

- /

- NYSE:SOC

A Fresh Look at Sable Offshore’s Valuation After New Development Plan Update

Simply Wall St

Reviewed by Kshitija Bhandaru

Sable Offshore (SOC) has just submitted an updated development and production plan to U.S. regulators, highlighting a move to use an Offshore Storage and Treating Vessel as a backup to the pending Las Flores Pipeline. This adjustment could meaningfully reshape how Sable approaches oil production going forward.

See our latest analysis for Sable Offshore.

While Sable Offshore’s strategic pivot is making waves, the stock has struggled recently. A 1-year total shareholder return of -10.4% and a sharp 25.2% drop in the past month suggest momentum has faded despite strong multi-year gains. Still, Sable’s three-year total return stands out at an impressive 86%, highlighting just how volatile turnaround stories can be in the energy sector.

If you’re interested in how operational shakeups might lead to outsized returns, now’s a great moment to broaden your search and discover fast growing stocks with high insider ownership

The stock’s mixed track record, combined with swift operational changes and a substantial discount to analyst price targets, raises the question: Is Sable Offshore quietly undervalued here, or is the future already fully reflected in today's price?

Price-to-Book of 4.1x: Is it justified?

Sable Offshore trades at a price-to-book ratio of 4.1x based on the last close price of $18.39, which makes the shares appear significantly more expensive than its listed peers.

The price-to-book ratio compares a company's market value to its book value. For energy firms like Sable Offshore, this metric often reflects the market’s expectations for asset productivity and future earnings potential.

Despite trading at such a premium, the current ratio is well above both peer and industry averages. This raises questions about whether the market is overestimating Sable’s prospects. Compared to US Oil and Gas industry peers, whose average is 1.4x, the premium is notable.

See what the numbers say about this price — find out in our valuation breakdown.

Result: Price-to-Book of 4.1x (OVERVALUED)

However, significant volatility in share performance and a recent negative net income could challenge the case for Sable Offshore’s current valuation premium.

Find out about the key risks to this Sable Offshore narrative.

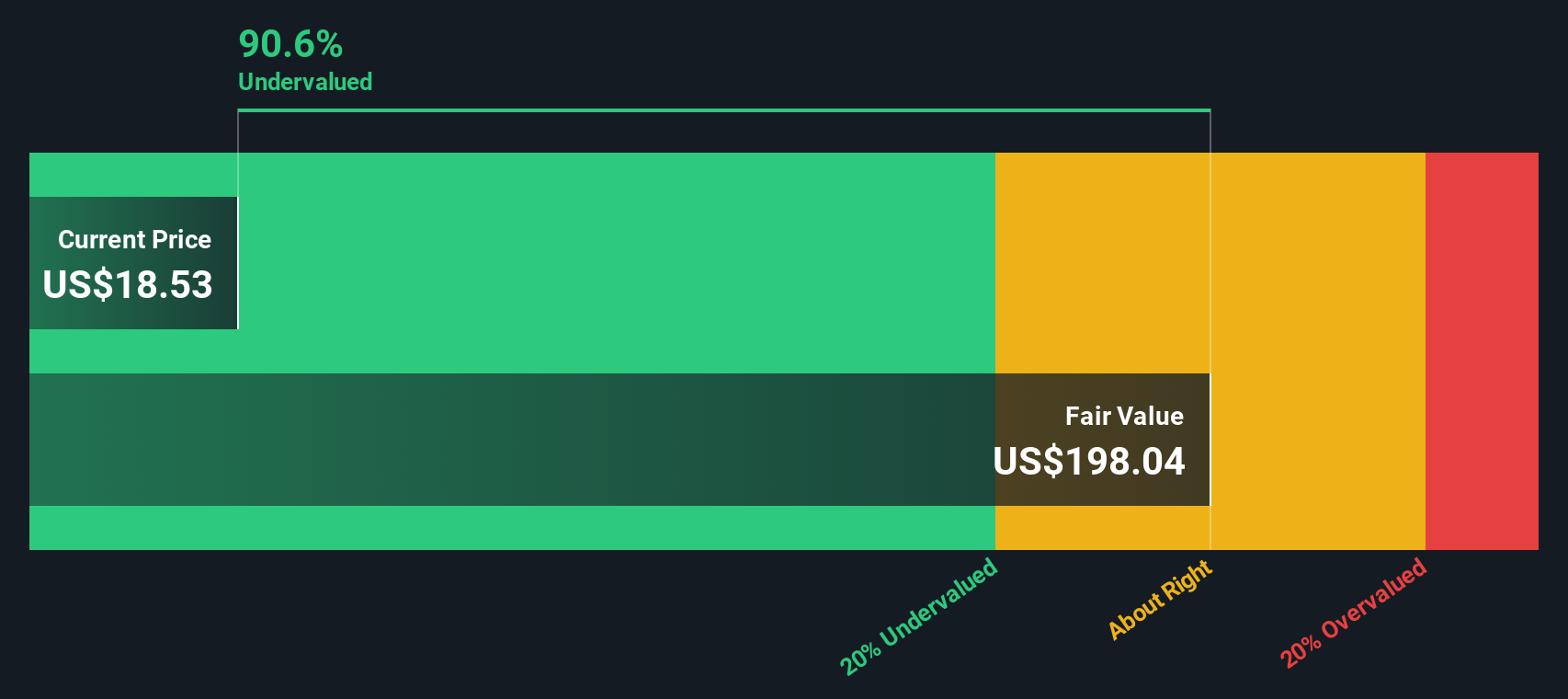

Another View: Discounted Cash Flow Paints a Different Picture

Looking beyond conventional multiples, our SWS DCF model estimates Sable Offshore's fair value at $209.12. This is dramatically higher than its current market price of $18.39. This suggests shares could be deeply undervalued if these cash flow forecasts prove reliable. Is the market overlooking hidden long-term value, or simply cautious for good reason?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Sable Offshore for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Sable Offshore Narrative

If you see the numbers differently or want to dig deeper into your own analysis, you can craft a Sable Offshore story in under three minutes. Do it your way

A great starting point for your Sable Offshore research is our analysis highlighting 3 key rewards and 4 important warning signs that could impact your investment decision.

Looking for more standout investment ideas?

Smart investors always keep an eye on what's next. Maximize your advantage by using our Simply Wall Street Screener to find the next breakout stocks and seize today’s opportunities.

- Unlock the potential of future finance by scanning these 79 cryptocurrency and blockchain stocks, which is reshaping global payments, decentralized security, and digital transactions.

- Capture stable returns with these 19 dividend stocks with yields > 3%, designed for those who prioritize consistent income and reliable yields above 3%.

- Stay ahead of market trends with these 24 AI penny stocks, spotlighting pioneering businesses at the forefront of artificial intelligence and automation breakthroughs.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:SOC

Sable Offshore

Operates as an independent oil and gas company in the United States.

High growth potential with slight risk.

Similar Companies

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|12.2% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|17.1% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|38.7% undervalued

TR

Community Contributor