- United States

- /

- Energy Services

- /

- NYSE:NBR

Nabors Industries (NYSE:NBR) Has Debt But No Earnings; Should You Worry?

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We note that Nabors Industries Ltd. (NYSE:NBR) does have debt on its balance sheet. But the real question is whether this debt is making the company risky.

When Is Debt Dangerous?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we think about a company's use of debt, we first look at cash and debt together.

View our latest analysis for Nabors Industries

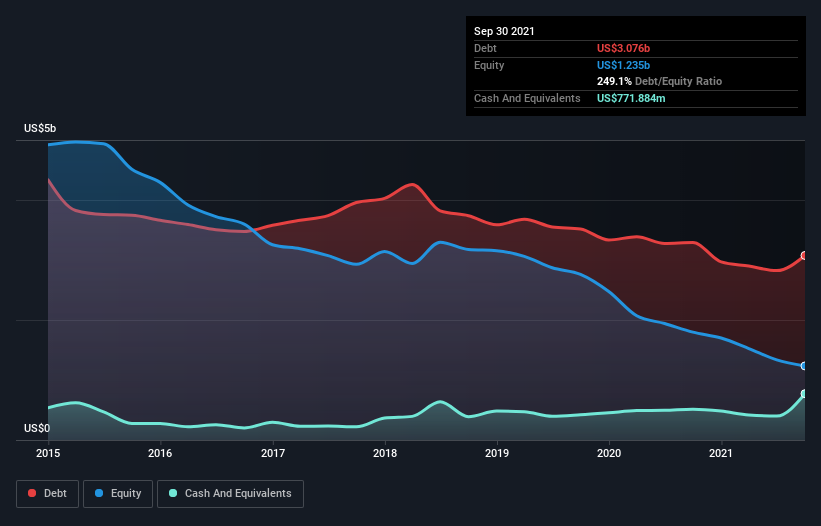

What Is Nabors Industries's Debt?

You can click the graphic below for the historical numbers, but it shows that Nabors Industries had US$3.08b of debt in September 2021, down from US$3.29b, one year before. On the flip side, it has US$771.9m in cash leading to net debt of about US$2.30b.

How Healthy Is Nabors Industries' Balance Sheet?

The latest balance sheet data shows that Nabors Industries had liabilities of US$516.1m due within a year, and liabilities of US$3.42b falling due after that. Offsetting this, it had US$771.9m in cash and US$308.9m in receivables that were due within 12 months. So its liabilities total US$2.86b more than the combination of its cash and short-term receivables.

This deficit casts a shadow over the US$661.8m company, like a colossus towering over mere mortals. So we'd watch its balance sheet closely, without a doubt. At the end of the day, Nabors Industries would probably need a major re-capitalization if its creditors were to demand repayment. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Nabors Industries's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

In the last year Nabors Industries had a loss before interest and tax, and actually shrunk its revenue by 20%, to US$1.9b. To be frank that doesn't bode well.

Caveat Emptor

Not only did Nabors Industries's revenue slip over the last twelve months, but it also produced negative earnings before interest and tax (EBIT). Its EBIT loss was a whopping US$286m. If you consider the significant liabilities mentioned above, we are extremely wary of this investment. That said, it is possible that the company will turn its fortunes around. But we think that is unlikely since it is low on liquid assets, and made a loss of US$583m in the last year. So while it's not wise to assume the company will fail, we do think it's risky. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. We've identified 3 warning signs with Nabors Industries , and understanding them should be part of your investment process.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

Valuation is complex, but we're here to simplify it.

Discover if Nabors Industries might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:NBR

Nabors Industries

Provides drilling and drilling-related services for land-based and offshore oil and natural gas wells in the United States and internationally.

Undervalued with reasonable growth potential.