- United States

- /

- Oil and Gas

- /

- NYSE:NAT

Here's Why Nordic American Tankers (NYSE:NAT) Can Afford Some Debt

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We can see that Nordic American Tankers Limited (NYSE:NAT) does use debt in its business. But is this debt a concern to shareholders?

When Is Debt Dangerous?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

Check out our latest analysis for Nordic American Tankers

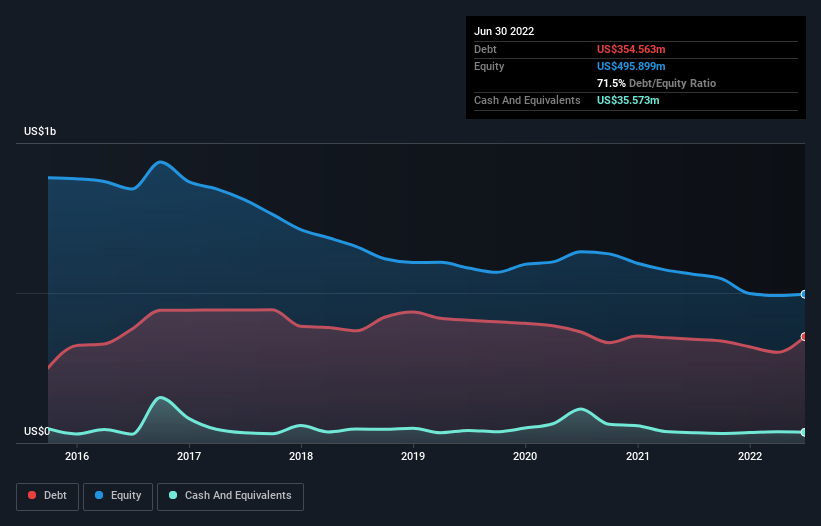

What Is Nordic American Tankers's Net Debt?

As you can see below, Nordic American Tankers had US$354.6m of debt, at June 2022, which is about the same as the year before. You can click the chart for greater detail. However, because it has a cash reserve of US$35.6m, its net debt is less, at about US$319.0m.

How Strong Is Nordic American Tankers' Balance Sheet?

According to the last reported balance sheet, Nordic American Tankers had liabilities of US$88.8m due within 12 months, and liabilities of US$314.5m due beyond 12 months. Offsetting this, it had US$35.6m in cash and US$11.4m in receivables that were due within 12 months. So it has liabilities totalling US$356.3m more than its cash and near-term receivables, combined.

This is a mountain of leverage relative to its market capitalization of US$486.0m. This suggests shareholders would be heavily diluted if the company needed to shore up its balance sheet in a hurry. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Nordic American Tankers's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

In the last year Nordic American Tankers wasn't profitable at an EBIT level, but managed to grow its revenue by 2.8%, to US$206m. We usually like to see faster growth from unprofitable companies, but each to their own.

Caveat Emptor

Over the last twelve months Nordic American Tankers produced an earnings before interest and tax (EBIT) loss. Indeed, it lost a very considerable US$67m at the EBIT level. When we look at that and recall the liabilities on its balance sheet, relative to cash, it seems unwise to us for the company to have any debt. So we think its balance sheet is a little strained, though not beyond repair. However, it doesn't help that it burned through US$104m of cash over the last year. So suffice it to say we consider the stock very risky. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet - far from it. To that end, you should learn about the 3 warning signs we've spotted with Nordic American Tankers (including 2 which shouldn't be ignored) .

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

Valuation is complex, but we're here to simplify it.

Discover if Nordic American Tankers might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:NAT

Nordic American Tankers

A tanker company, acquires and charters double-hull tankers in Bermuda and internationally.

Fair value with mediocre balance sheet.