- United States

- /

- Oil and Gas

- /

- NYSE:MPLX

Is It Too Late To Consider MPLX After Its Strong Multi Year Rally?

Reviewed by Bailey Pemberton

- If you are wondering whether MPLX is still a smart consideration after its big run, or if you would just be chasing past gains, this breakdown will help you think through whether the current price makes sense or not.

- The stock has cooled slightly over the last week with a -1.8% move, but it is still up 4.5% over the past month, 12.8% year to date, 21.3% over 1 year, 119.4% over 3 years, and 283.5% over 5 years, which naturally raises the question of how much upside might be left from here.

- Recent headlines around midstream energy infrastructure, pipeline capacity expansions, and continued demand for refined products have kept investor attention on MPLX. This has reinforced the idea that its cash flows could be more durable than a typical cyclical energy play. At the same time, broader market debates about interest rates and income-focused assets are influencing how investors price stable, high-yield names like this one.

- Despite that track record, MPLX currently scores a 5/6 on our valuation checks, suggesting it still looks undervalued on most of the metrics we track. In the sections that follow we will walk through those valuation approaches, before finishing with a different way to think about what "fair value" really means for this stock.

Approach 1: MPLX Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model estimates what a business is worth by projecting the cash it can generate in the future and discounting those cash flows back to today in $ terms.

For MPLX, the latest twelve month Free Cash Flow is about $4.9 billion. Analysts provide explicit forecasts for the next few years, and Simply Wall St then extends those trends using a 2 Stage Free Cash Flow to Equity model. Under this framework, MPLX’s Free Cash Flow is projected to reach roughly $6.4 billion by 2035, with analyst inputs through 2029 and more modest growth rates applied thereafter.

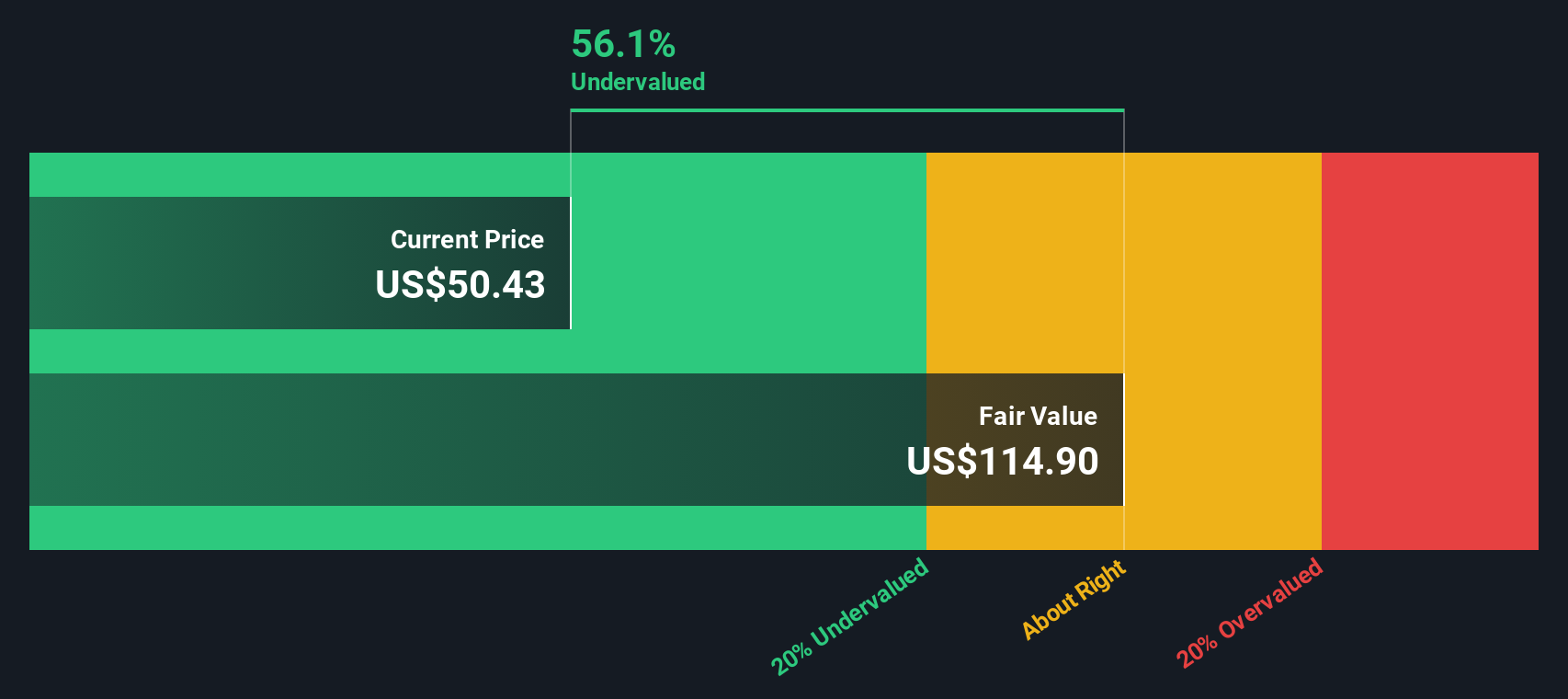

When all those projected cash flows are discounted back to today, the model arrives at an intrinsic value of about $123.51 per unit. Compared with the current market price, this indicates MPLX is trading at roughly a 55.6% discount to its estimated fair value, suggesting a wide margin of safety based purely on cash generation.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests MPLX is undervalued by 55.6%. Track this in your watchlist or portfolio, or discover 907 more undervalued stocks based on cash flows.

Approach 2: MPLX Price vs Earnings

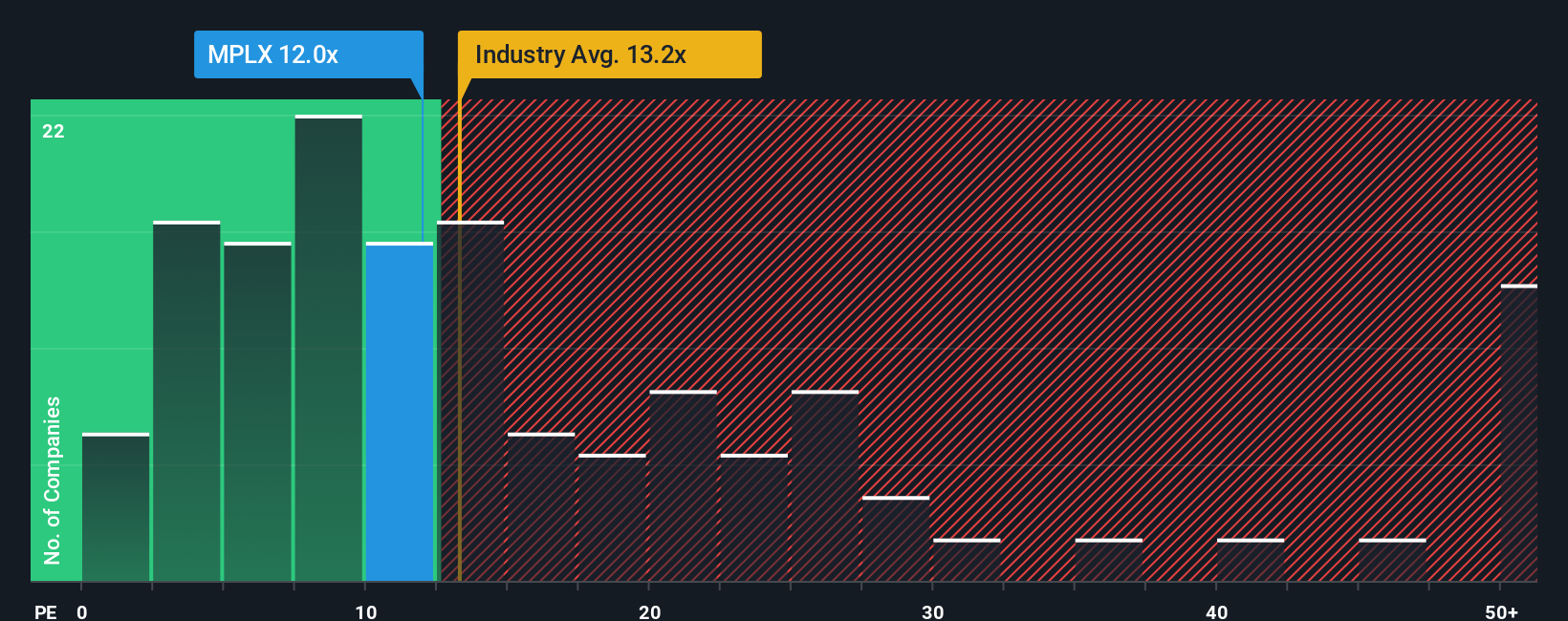

For profitable, steady cash generators like MPLX, the Price to Earnings (PE) ratio is a useful way to gauge how much investors are paying for each dollar of current earnings. It is intuitive, widely used, and links directly to the income that ultimately supports distributions.

What counts as a fair PE ratio depends on two big levers: expected earnings growth and perceived risk. Faster, more dependable growers usually command higher multiples, while slower or riskier names tend to trade at discounts. MPLX currently trades on a PE of about 11.6x, below the Oil and Gas industry average of roughly 13.3x and well under the peer average of around 19.5x. This suggests the market is valuing its earnings more conservatively than many comparable names.

Simply Wall St’s Fair Ratio framework goes a step further by estimating what PE multiple might be appropriate given MPLX’s specific earnings growth outlook, industry, profit margins, size, and risk profile. For MPLX, that Fair Ratio is about 20.0x, materially higher than the current 11.6x. Because this approach is tailored to the company rather than generic sector comparisons, it provides a more nuanced view that points to the units trading at a meaningful discount to what its fundamentals might justify.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1448 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your MPLX Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives. These are simply the story you believe about a company, tied directly to your own assumptions for its future revenue, earnings, margins and fair value. All of this is captured in an easy tool on Simply Wall St’s Community page that millions of investors use to compare their Fair Value to today’s Price. The tool automatically updates as fresh news or earnings arrive and allows, for example, one MPLX investor to build a bullish Narrative around successful Permian expansion and robust contracts that supports a fair value closer to the top of the current analyst range at about $64 per unit. Another investor may take a more cautious view on commodity cycles and project risk and anchor their Narrative nearer the low end around $51. In each case, the investor turns their perspective into a concrete forecast and valuation that can be tracked over time.

Do you think there's more to the story for MPLX? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:MPLX

MPLX

Owns and operates midstream energy infrastructure and logistics assets primarily in the United States.

Undervalued established dividend payer.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

A tech powerhouse quietly powering the world’s AI infrastructure.

Keppel DC REIT (SGX: AJBU) is a resilient gem in the data center space.

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)