Advertisement

- United States

- /

- Oil and Gas

- /

- NYSE:FRO

Will Frontline’s (FRO) High Dividend Focus Sustain Investor Confidence Amid Strong VLCC Market?

Simply Wall St

Reviewed by Sasha Jovanovic

- Following recent investor meetings, BTIG reiterated positive commentary on Frontline Ltd., highlighting ongoing strength in Very Large Crude Carrier (VLCC) rates and management’s reaffirmation of its 80% dividend distribution target, signaling a continued emphasis on shareholder returns and capital discipline.

- This focus on distributing cash rather than accumulating it, underpinned by management’s commitment and supported by a strong balance sheet, may further reinforce investor confidence in Frontline’s approach to aligning interests with shareholders amid a favorable industry backdrop.

- Given management’s clear commitment to high dividend payouts, we’ll examine the implications of this strategy for Frontline’s investment narrative.

Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

Frontline Investment Narrative Recap

To be a Frontline shareholder today, you need to believe in the ongoing resilience of global crude oil demand, tight vessel supply, and the company’s ability to sustain high dividend payouts even as earnings fluctuate. The recent BTIG commentary confirms management’s commitment to cash returns and highlights strong VLCC rates, which supports the primary short-term catalyst, but does not materially change the current biggest risk: exposure to volatile spot market rates if demand weakens.

Among recent company developments, Frontline’s August 2025 dividend increase to US$0.36 per share stands out as most relevant, given the current focus on shareholder returns. This aligns with the reiterated 80 percent cash distribution target and continued strong balance sheet, supporting the company’s stance amid robust tanker demand but not eliminating the earnings sensitivity to rate movements.

However, investors should keep in mind, while dividend payouts are currently high, changes in spot charter rates could rapidly affect Frontline’s ability to maintain these distributions if demand...

Read the full narrative on Frontline (it's free!)

Frontline's narrative projects $1.3 billion revenue and $828.1 million earnings by 2028. This requires a 10.7% annual revenue decline and an earnings increase of $590.1 million from current earnings of $238.0 million.

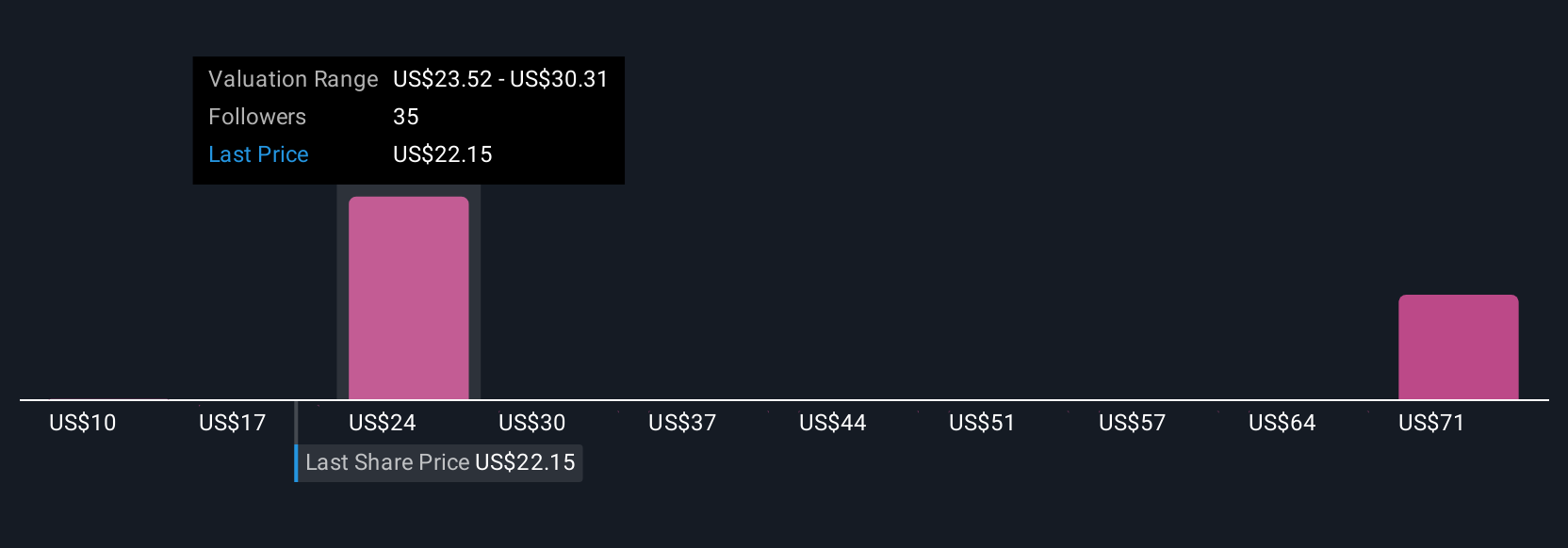

Uncover how Frontline's forecasts yield a $25.40 fair value, a 14% upside to its current price.

Exploring Other Perspectives

Eight Simply Wall St Community members estimate Frontline’s fair value from as low as US$9.65 to as high as US$81.64 per share. High dependence on the spot market may amplify volatility for both earnings and perceptions of value, so take the time to review a variety of forecasts before deciding how this aligns with your outlook.

Explore 8 other fair value estimates on Frontline - why the stock might be worth less than half the current price!

Build Your Own Frontline Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Frontline research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Frontline research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Frontline's overall financial health at a glance.

Ready For A Different Approach?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- We've found 19 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- These 13 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:FRO

Frontline

A shipping company, engages in the ownership and operation of oil and product tankers worldwide.

Good value with reasonable growth potential and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|12.2% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|17.1% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|38.1% undervalued

TR

Community Contributor