The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We can see that Frontline plc (NYSE:FRO) does use debt in its business. But should shareholders be worried about its use of debt?

When Is Debt Dangerous?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we examine debt levels, we first consider both cash and debt levels, together.

Check out our latest analysis for Frontline

What Is Frontline's Debt?

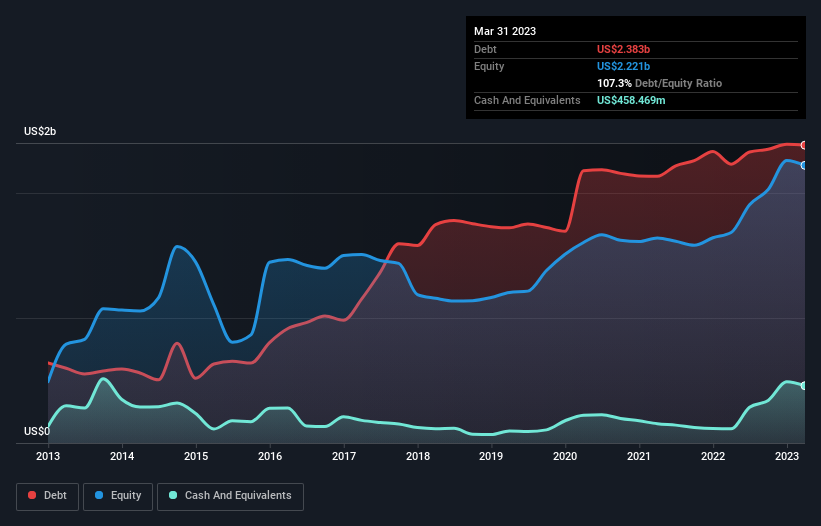

You can click the graphic below for the historical numbers, but it shows that as of March 2023 Frontline had US$2.38b of debt, an increase on US$2.23b, over one year. On the flip side, it has US$458.5m in cash leading to net debt of about US$1.92b.

How Strong Is Frontline's Balance Sheet?

The latest balance sheet data shows that Frontline had liabilities of US$475.0m due within a year, and liabilities of US$2.02b falling due after that. On the other hand, it had cash of US$458.5m and US$260.6m worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$1.78b.

While this might seem like a lot, it is not so bad since Frontline has a market capitalization of US$3.39b, and so it could probably strengthen its balance sheet by raising capital if it needed to. But we definitely want to keep our eyes open to indications that its debt is bringing too much risk.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

With a debt to EBITDA ratio of 2.3, Frontline uses debt artfully but responsibly. And the alluring interest cover (EBIT of 7.7 times interest expense) certainly does not do anything to dispel this impression. Notably, Frontline made a loss at the EBIT level, last year, but improved that to positive EBIT of US$649m in the last twelve months. There's no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Frontline can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So it's worth checking how much of the earnings before interest and tax (EBIT) is backed by free cash flow. In the last year, Frontline's free cash flow amounted to 24% of its EBIT, less than we'd expect. That weak cash conversion makes it more difficult to handle indebtedness.

Our View

Frontline's conversion of EBIT to free cash flow and level of total liabilities definitely weigh on it, in our esteem. But it seems to be able to cover its interest expense with its EBIT without much trouble. Taking the abovementioned factors together we do think Frontline's debt poses some risks to the business. So while that leverage does boost returns on equity, we wouldn't really want to see it increase from here. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. Be aware that Frontline is showing 4 warning signs in our investment analysis , and 1 of those is potentially serious...

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:FRO

Frontline

A shipping company, engages in the seaborne transportation of crude oil and oil products worldwide.

Undervalued slight.

Similar Companies

Market Insights

Community Narratives