- United States

- /

- Oil and Gas

- /

- NYSE:EQT

EQT (EQT) Secures 20-Year LNG Agreement from Port Arthur Phase 2 Project

Reviewed by Simply Wall St

EQT (EQT) saw a price movement of 4% over the last week, coinciding with the announcement of a 20-year agreement with Sempra Infrastructure for the purchase of liquefied natural gas. This agreement may have added weight to the broader market's upward trend of 1% during the same period. While the market anticipated Nvidia's earnings, regulatory news around EQT's involvement in LNG projects gained attention. As market indices reached near-record highs, EQT's developments provided an additional nod to investor interest, aligned with the positive market momentum.

Buy, Hold or Sell EQT? View our complete analysis and fair value estimate and you decide.

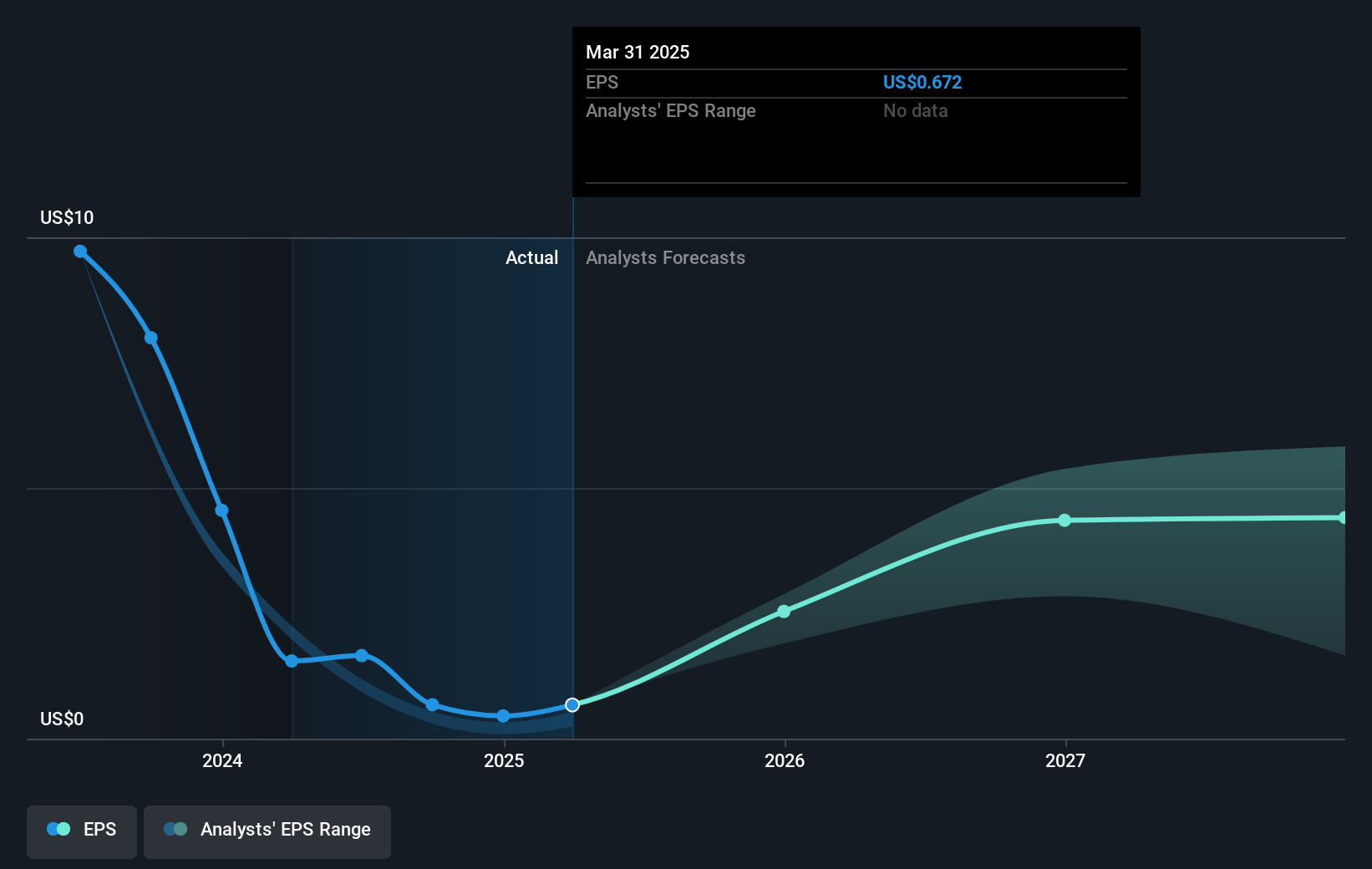

The recent 4% uptick in EQT’s share price, linked with the announcement of a 20-year agreement with Sempra Infrastructure, reinforces the company’s focus on long-term stability and growth in liquefied natural gas. This collaboration is likely to support EQT’s aim for high-quality cash flow, as detailed in the prior narrative. The agreement amplifies EQT's exposure to burgeoning demand for natural gas infrastructure in the Appalachian region, potentially bolstering future revenues and earnings. Analysts have predicted a rise in EQT's revenue, but this new deal could enhance such forecasts by securing stable cash flows and allowing for margin expansions amid a competitive landscape.

Over the past five years, EQT has achieved a significant total shareholder return of 258.61%, reflecting strong investor interest and favorable market conditions. Compared to the broader US market's one-year return of 16.2%, EQT has performed well, surpassing the industry growth rates, particularly in the last year, where it exceeded the US Oil and Gas industry's decline of 0.1% by a large margin. This longer-term performance context highlights EQT’s robust growth trajectory and ability to deliver attractive shareholder returns over time.

With the current share price at US$52.71 and a consensus price target of US$63.28, the market's reaction puts EQT's stock at a 20.05% discount. This gap presents a potential opportunity for investors as analysts show an expectation for higher valuation based on future earnings growth and margin improvements. While market trends and regulatory risks remain factors to watch, the ongoing development in infrastructure and strategic agreements such as the one with Sempra are critical to realizing these expectations and aligning them with the narrative's emphasis on long-term value.

Our expertly prepared valuation report EQT implies its share price may be lower than expected.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if EQT might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:EQT

EQT

Engages in the production, gathering, and transmission of natural gas.

Solid track record with adequate balance sheet.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fiverr International will transform the freelance industry with AI-powered growth

Stride Stock: Online Education Finds Its Second Act

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)