- United States

- /

- Oil and Gas

- /

- NYSE:BTU

Peabody Energy Corporation (NYSE:BTU) Held Back By Insufficient Growth Even After Shares Climb 26%

Peabody Energy Corporation (NYSE:BTU) shares have had a really impressive month, gaining 26% after a shaky period beforehand. Notwithstanding the latest gain, the annual share price return of 8.1% isn't as impressive.

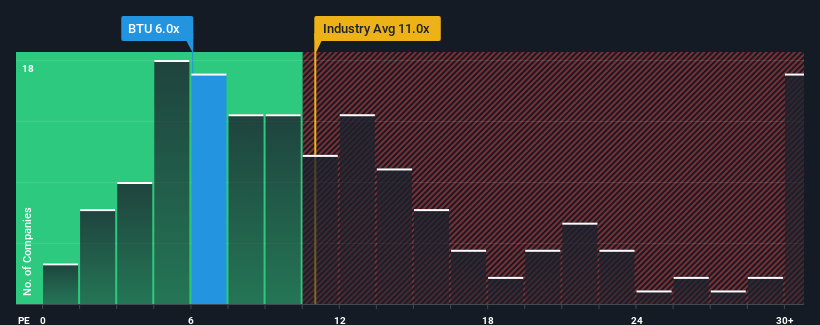

In spite of the firm bounce in price, Peabody Energy may still be sending very bullish signals at the moment with its price-to-earnings (or "P/E") ratio of 6x, since almost half of all companies in the United States have P/E ratios greater than 19x and even P/E's higher than 34x are not unusual. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's so limited.

Peabody Energy has been struggling lately as its earnings have declined faster than most other companies. The P/E is probably low because investors think this poor earnings performance isn't going to improve at all. If you still like the company, you'd want its earnings trajectory to turn around before making any decisions. If not, then existing shareholders will probably struggle to get excited about the future direction of the share price.

See our latest analysis for Peabody Energy

Does Growth Match The Low P/E?

In order to justify its P/E ratio, Peabody Energy would need to produce anemic growth that's substantially trailing the market.

Retrospectively, the last year delivered a frustrating 58% decrease to the company's bottom line. At least EPS has managed not to go completely backwards from three years ago in aggregate, thanks to the earlier period of growth. So it appears to us that the company has had a mixed result in terms of growing earnings over that time.

Turning to the outlook, the next three years should bring diminished returns, with earnings decreasing 8.2% each year as estimated by the four analysts watching the company. With the market predicted to deliver 10% growth each year, that's a disappointing outcome.

With this information, we are not surprised that Peabody Energy is trading at a P/E lower than the market. However, shrinking earnings are unlikely to lead to a stable P/E over the longer term. There's potential for the P/E to fall to even lower levels if the company doesn't improve its profitability.

The Final Word

Even after such a strong price move, Peabody Energy's P/E still trails the rest of the market significantly. Using the price-to-earnings ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

We've established that Peabody Energy maintains its low P/E on the weakness of its forecast for sliding earnings, as expected. Right now shareholders are accepting the low P/E as they concede future earnings probably won't provide any pleasant surprises. It's hard to see the share price rising strongly in the near future under these circumstances.

Before you settle on your opinion, we've discovered 2 warning signs for Peabody Energy (1 makes us a bit uncomfortable!) that you should be aware of.

If these risks are making you reconsider your opinion on Peabody Energy, explore our interactive list of high quality stocks to get an idea of what else is out there.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:BTU

Peabody Energy

Engages in coal mining business in the United States, Japan, Taiwan, Australia, India, Brazil, Belgium, Chile, France, Indonesia, China, Vietnam, South Korea, Germany, and internationally.

Very undervalued with flawless balance sheet.

Similar Companies

Market Insights

Community Narratives