The spotlight is back on National Energy Services Reunited (NasdaqCM:NESR) after Maxim Group’s analyst Tate Sullivan initiated coverage with a buy rating. For investors who have been following the company, this new coverage is more than just another stamp of approval. Analyst initiations with an upbeat outlook tend to attract attention, and it is not uncommon for these events to reframe how the market views a stock’s potential and risk.

This comes at a time when NESR has shown clear momentum. The stock is up over 7% in the past week and nearly 47% during the past month, signaling that the market is taking a closer look. Zooming out, the 12 month return clocks in at around 8%, which trails its multi-year pace. NESR has grown almost 50% over three years. While there have been periods of slower progress, the recent burst suggests this new analyst coverage could be amplifying existing trends.

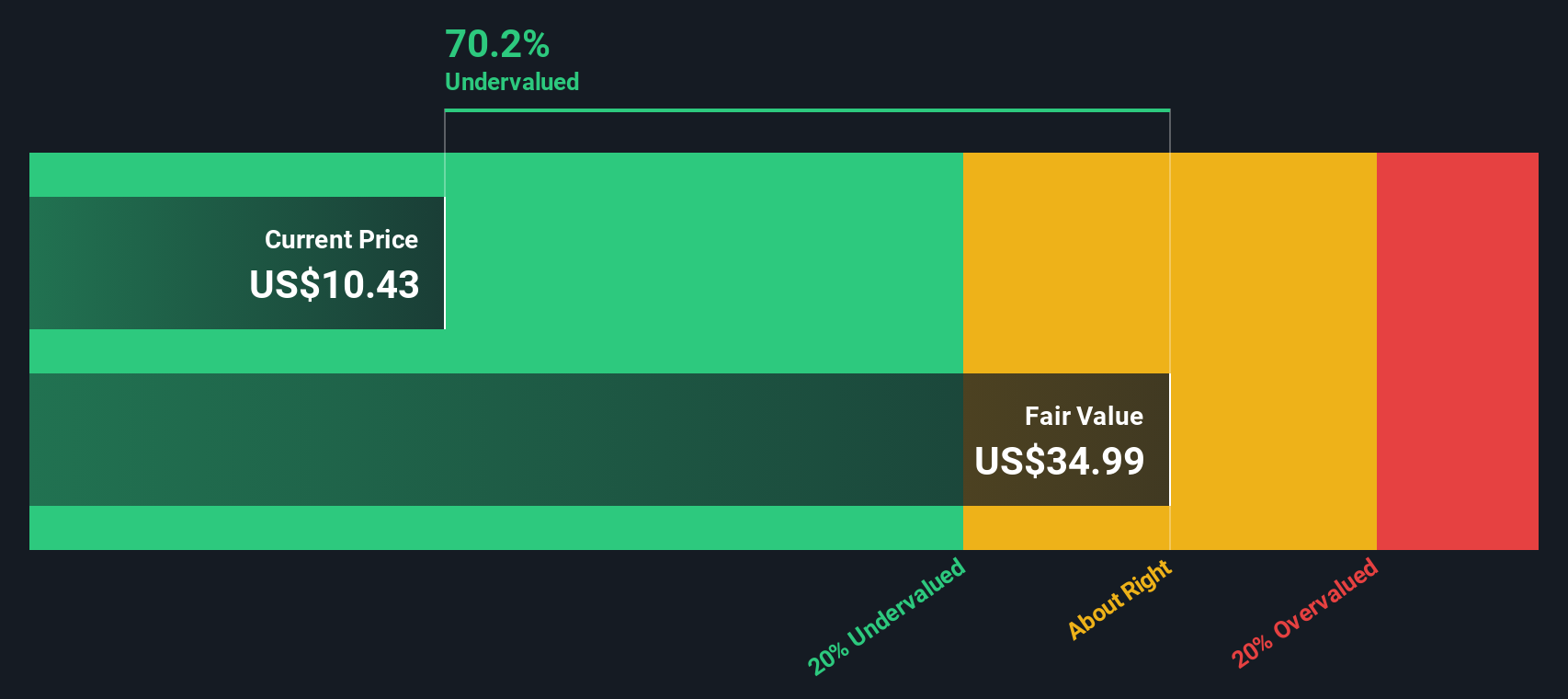

The big question now is whether NESR is attractively priced in the wake of this rally, or if the market is already baking future growth into today's price.

Advertisement

Most Popular Narrative: 22.3% Undervalued

The dominant narrative values NESR as significantly undervalued, suggesting a notable gap between its current price and what analysts believe is its fair value. This is based on future earnings growth and sector tailwinds.

“Activity in unconventional resource development, especially gas, across the Middle East is accelerating. NESR's established position in Saudi's Jafurah project and expanding contracts in Kuwait and North Africa provide strong exposure to secular increases in service intensity per well, which supports both top-line expansion and higher per-unit margins.”

What if the most important numbers for NESR's future have yet to hit the headlines? The main narrative fueling this undervaluation is built on bold financial projections about growth in key energy regions and a dramatic improvement in profitability. Analysts are betting on a transformation, but the real logic behind this fair value target is hidden in the forward-looking math. Hungry for the financial details that make this target possible? The core assumptions are more ambitious than you might think.

However, delays in contract awards or unrest in some MENA countries could quickly disrupt NESR's revenue visibility and put pressure on the bullish outlook.

While analysts' price targets paint a bullish picture, our DCF model tells a more extreme story by indicating NESR is dramatically undervalued if future cash flows play out as modeled. Does the market see it differently?

Build Your Own National Energy Services Reunited Narrative

If you see things differently, or want to dive deeper into the numbers yourself, you can craft your own narrative in just a few minutes: Do it your way.

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding National Energy Services Reunited.

Looking for more investment ideas?

Missing out on other high-potential stocks is easy if you only stick to the headlines. Take control of your investing future with handpicked opportunities waiting below.

Supercharge your portfolio's income with companies offering market-beating yields by using our dividend stocks with yields > 3%.

Get ahead of the curve with companies at the forefront of artificial intelligence using our exclusive AI penny stocks.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if National Energy Services Reunited might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.