- United States

- /

- Energy Services

- /

- NasdaqGS:KLXE

Health Check: How Prudently Does KLX Energy Services Holdings (NASDAQ:KLXE) Use Debt?

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We can see that KLX Energy Services Holdings, Inc. (NASDAQ:KLXE) does use debt in its business. But the more important question is: how much risk is that debt creating?

Why Does Debt Bring Risk?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

Check out our latest analysis for KLX Energy Services Holdings

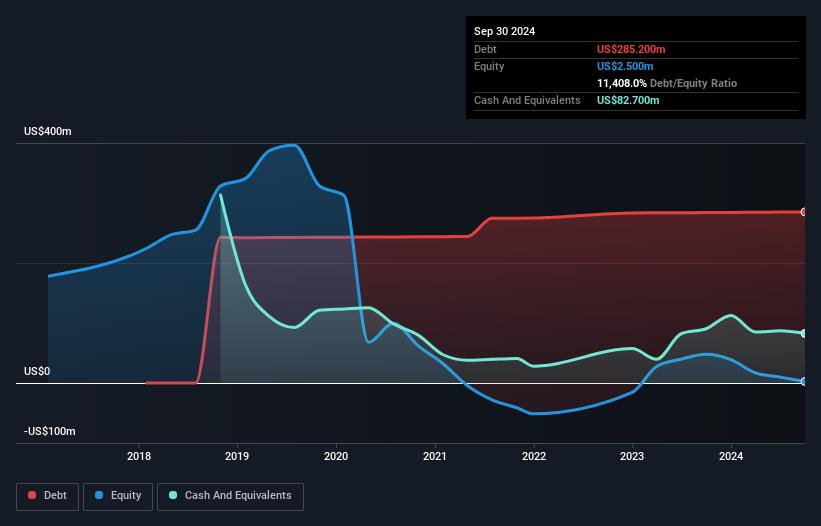

How Much Debt Does KLX Energy Services Holdings Carry?

The chart below, which you can click on for greater detail, shows that KLX Energy Services Holdings had US$285.2m in debt in September 2024; about the same as the year before. On the flip side, it has US$82.7m in cash leading to net debt of about US$202.5m.

A Look At KLX Energy Services Holdings' Liabilities

We can see from the most recent balance sheet that KLX Energy Services Holdings had liabilities of US$205.1m falling due within a year, and liabilities of US$279.2m due beyond that. Offsetting these obligations, it had cash of US$82.7m as well as receivables valued at US$124.8m due within 12 months. So it has liabilities totalling US$276.8m more than its cash and near-term receivables, combined.

This deficit casts a shadow over the US$105.4m company, like a colossus towering over mere mortals. So we definitely think shareholders need to watch this one closely. At the end of the day, KLX Energy Services Holdings would probably need a major re-capitalization if its creditors were to demand repayment. There's no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if KLX Energy Services Holdings can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

In the last year KLX Energy Services Holdings had a loss before interest and tax, and actually shrunk its revenue by 20%, to US$738m. That's not what we would hope to see.

Caveat Emptor

Not only did KLX Energy Services Holdings's revenue slip over the last twelve months, but it also produced negative earnings before interest and tax (EBIT). Indeed, it lost US$8.5m at the EBIT level. Combining this information with the significant liabilities we already touched on makes us very hesitant about this stock, to say the least. That said, it is possible that the company will turn its fortunes around. Nevertheless, we would not bet on it given that it lost US$48m in just last twelve months, and it doesn't have much by way of liquid assets. So while it's not wise to assume the company will fail, we do think it's risky. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. For example, we've discovered 4 warning signs for KLX Energy Services Holdings that you should be aware of before investing here.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

Valuation is complex, but we're here to simplify it.

Discover if KLX Energy Services Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:KLXE

KLX Energy Services Holdings

Provides drilling, completions, production, and well intervention services and products to the onshore oil and gas producing regions of the United States.

Undervalued with mediocre balance sheet.