Certainly! Here is the revised article with em dashes removed and the formatting improved:

If you’re holding shares of Two Harbors Investment (TWO) or considering adding it to your watchlist, the latest dividend news probably raised your eyebrows. The company’s Board of Directors just announced a reduced third quarter dividend for common shareholders, a move that often stirs debate about management’s outlook. While preferred dividends remain steady for now, this lower payout on common shares signals that management might be rethinking its priorities given the current earnings environment.

Even before this change, Two Harbors Investment stock had not been on a winning streak. Over the past year, shares are down 15%. Longer-term performance has also been underwhelming, with momentum continuing to fade throughout the year. The dividend cut comes in addition to annual revenue that shrank, while net income bounced back from deeper losses. This creates a complicated picture for investors tracking value and risk.

With this recent adjustment and a lagging share price, some may wonder whether Two Harbors Investment is now a bargain, or if the current price already reflects Wall Street’s expectations for future growth setbacks.

Advertisement

Price-to-Sales Ratio of 4.1x: Is it justified?

Two Harbors Investment is currently valued at a Price-to-Sales (P/S) ratio of 4.1x, which suggests the stock is somewhat expensive compared to both its industry peers and broader valuation benchmarks.

The Price-to-Sales ratio measures how much investors are willing to pay for each dollar of a company’s revenue. For mortgage REITs and similar financial stocks, this ratio is particularly useful when companies are unprofitable or earnings are volatile. Revenue is generally a more stable metric than net income.

Looking specifically at the current figures, the stock’s P/S ratio is higher than the peer average of 3.9x and is considerably above the estimated fair value multiple of 0.3x. While it is slightly cheaper than the broader US Mortgage REITs industry at 4.4x, the valuation implies that investors expect positive revenue growth or improved earnings quality. However, with recent revenue decline and ongoing challenges, the market may be overestimating the company’s ability to rebound.

However, a surprise rebound in revenue growth or a sharp recovery in net income could challenge the current negative outlook for Two Harbors Investment.

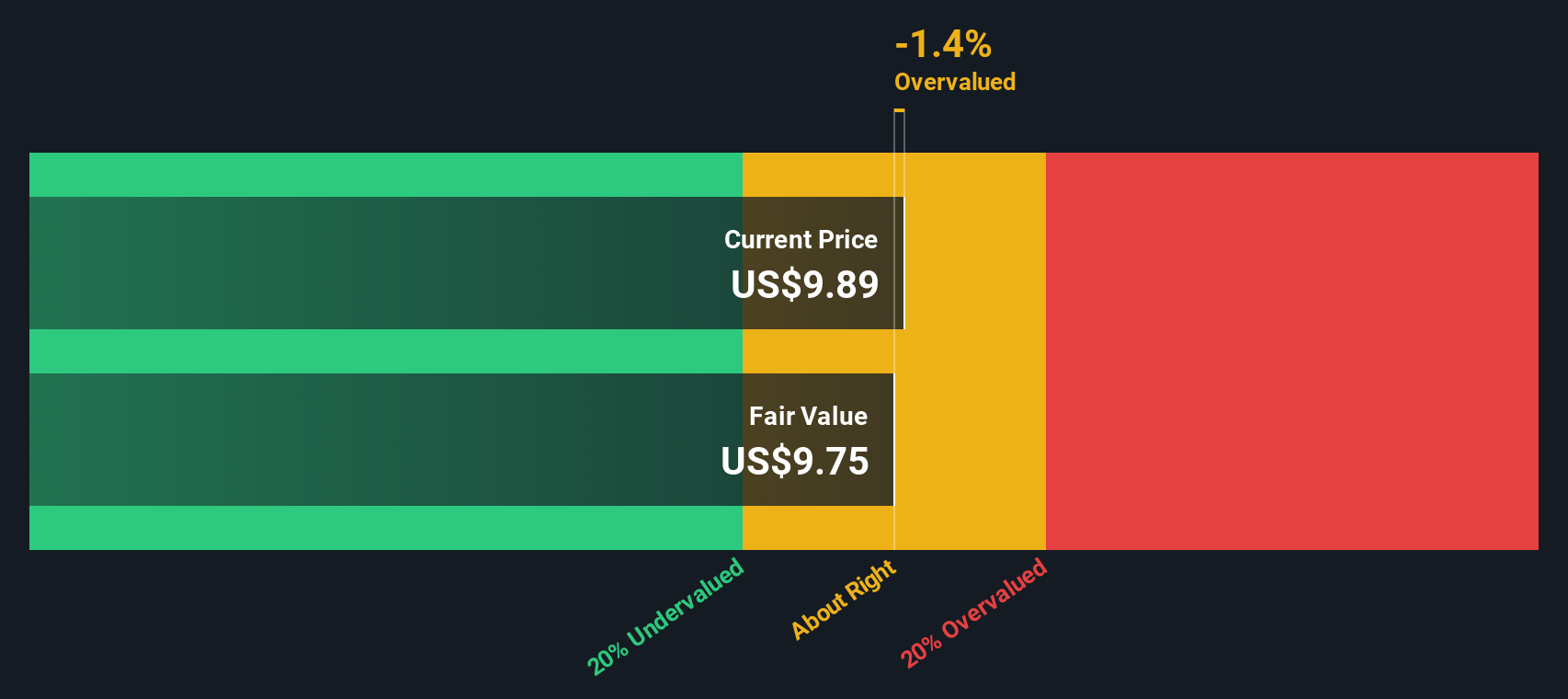

While the price-to-sales multiple shows Two Harbors Investment as expensive, our DCF model presents a similar outlook and suggests the shares are trading above fair value. Could the market be missing a potential turnaround?

If you want to look beyond this analysis or prefer to dig into the numbers yourself, you can easily develop your own view in just a few minutes. do it your way.

A great starting point for your Two Harbors Investment research is our analysis highlighting 1 key reward and 1 important warning sign that could impact your investment decision.

Looking for More Smart Investment Opportunities?

Don’t let great stocks or emerging trends pass you by when your next winning idea could be just a few clicks away. Use the Simply Wall Street Screener to uncover standout companies and fresh angles. Here are three exciting paths you can act on today:

Target secure income and beat the market by seeking out dividend stocks with yields > 3%. These can reward you with healthy yields and a track record of reliable payouts.

Ride the innovation wave and capture growth by tapping into booming AI penny stocks. These companies are powering advances in artificial intelligence and automation.

Capitalize on strong businesses with hidden value by searching for undervalued stocks based on cash flows. This can help you unlock stocks trading below their potential and primed for future upside.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Two Harbors Investment might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Invests in, finances, and manages mortgage servicing rights (MSRs), agency residential mortgage-backed securities (RMBS), and other financial assets through RoundPoint in the United States.