Advertisement

- United States

- /

- Mortgage REITs

- /

- NYSE:RITM

Is Rithm Capital Still Attractive After Its Strong Multi Year Share Price Climb?

Simply Wall St

Reviewed by Bailey Pemberton

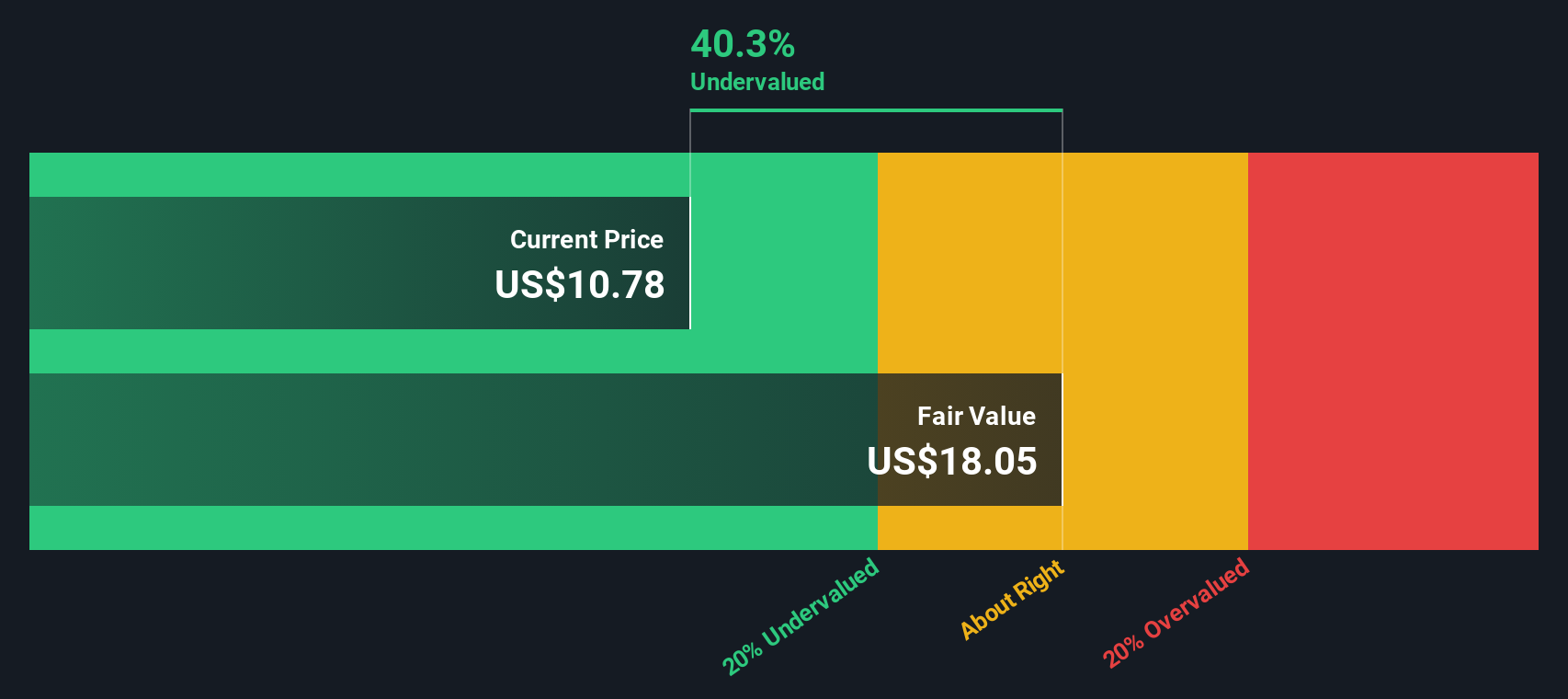

- If you have been wondering whether Rithm Capital is still good value after its recent run, you are not alone. This stock is starting to pop up on a lot more radar screens.

- Over the last year Rithm is up about 12.0%, building on a strong multi year climb of roughly 71.6% over three years and 94.7% over five years, even though the past week has seen a mild pullback of around 0.9% after a 3.2% rise over the last month.

- That climb has come alongside a steady repositioning of the business toward capital light, fee driven platforms and ongoing portfolio reshuffling in response to shifting interest rate expectations. Together, these moves have helped reshape how investors think about both Rithm's growth potential and its risk profile.

- Despite that re rating, Rithm currently scores a full 6/6 on our valuation checks, suggesting it still screens as undervalued across all our standard metrics. Next we will walk through the different valuation approaches behind that score and then finish with a more complete way to think about what Rithm is really worth.

Approach 1: Rithm Capital Excess Returns Analysis

The Excess Returns model asks whether Rithm Capital is earning more on its equity than investors require, and then capitalizes that surplus into an intrinsic value per share. In simple terms, it compares the company’s profitability on shareholder funds with its cost of equity.

For Rithm, the starting point is a Book Value of $12.83 per share and a Stable EPS of $1.36 per share, based on the median return on equity over the past five years. Against a Cost of Equity of $1.13 per share, this implies an Excess Return of about $0.23 per share, supported by an Average Return on Equity of 11.06%. The model then assumes a Stable Book Value of $12.31 per share, again anchored to the five year median, and projects these excess returns forward.

Aggregating those future excess returns gives an intrinsic value of roughly $16.15 per share, implying the stock is about 29.3% undervalued versus the current market price.

Result: UNDERVALUED

Our Excess Returns analysis suggests Rithm Capital is undervalued by 29.3%. Track this in your watchlist or portfolio, or discover 915 more undervalued stocks based on cash flows.

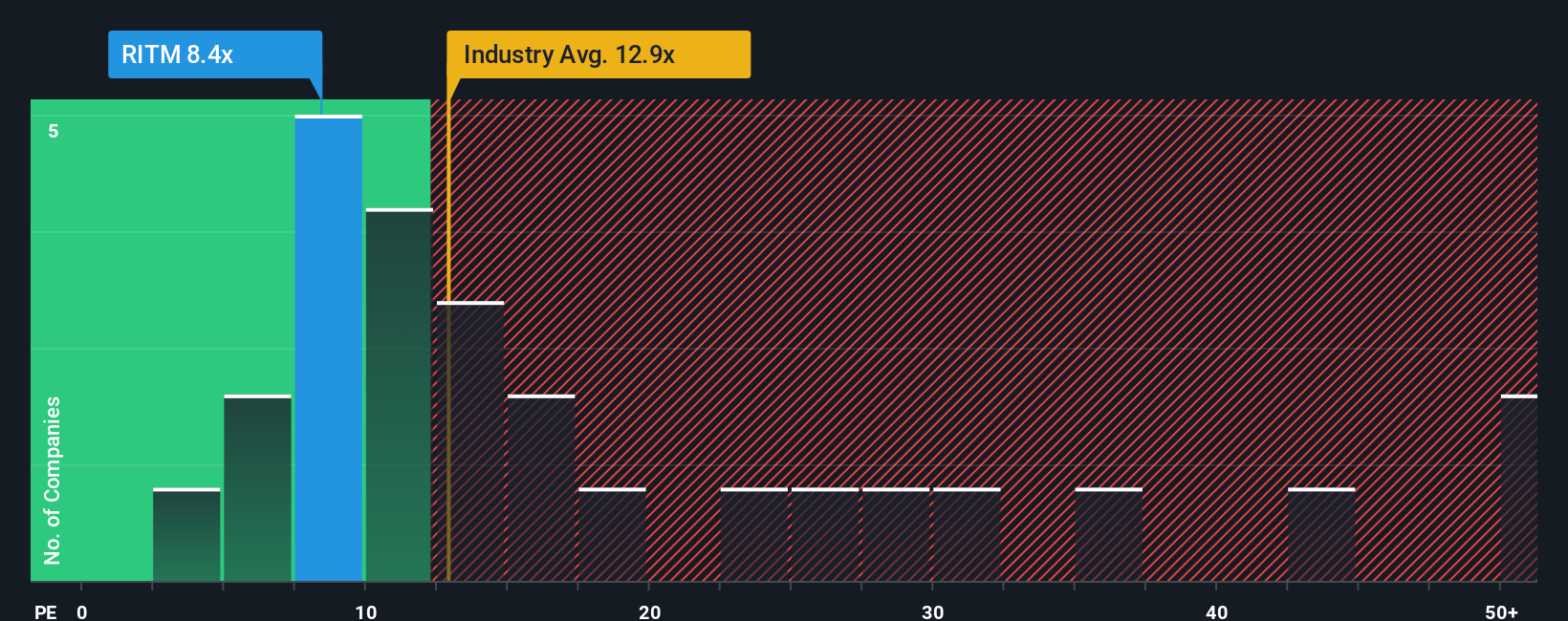

Approach 2: Rithm Capital Price vs Earnings

For a profitable company like Rithm Capital, the price to earnings, or PE, ratio is a straightforward way to gauge how much investors are willing to pay for each dollar of current earnings. In general, faster growth and lower perceived risk justify a higher PE multiple, while slower growth or higher risk should translate into a lower, more conservative PE.

Rithm currently trades on a PE of about 8.1x, which sits well below both the Mortgage REITs industry average of roughly 13.1x and a broader peer average of around 13.5x. At first glance, that gap suggests the market is pricing Rithm more cautiously than its sector, despite its solid track record.

Simply Wall St’s Fair Ratio framework goes a step further by estimating what a “normal” multiple should be for Rithm, given its earnings growth, risk profile, profit margins, industry and market cap. On this basis, Rithm’s Fair PE Ratio is 14.6x, meaning that, once these company specific factors are accounted for, the stock appears meaningfully discounted versus where it ought to trade.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1443 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Rithm Capital Narrative

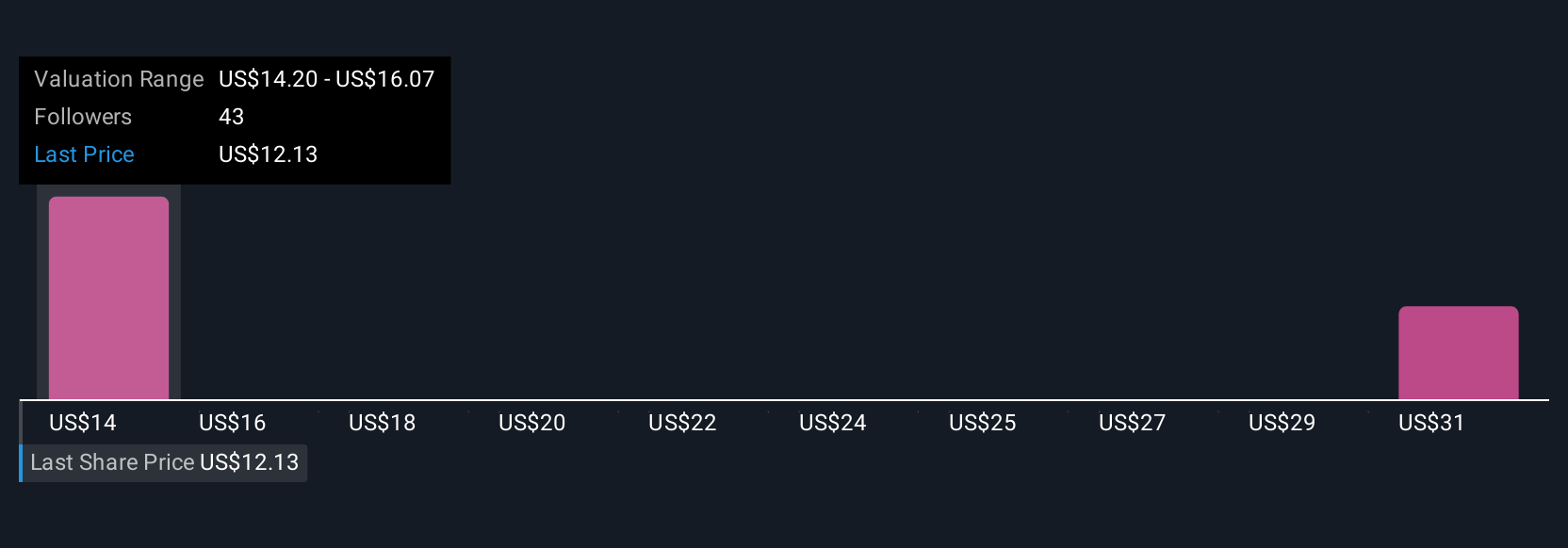

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, a simple framework that lets you attach a clear story to the numbers behind your investment thesis.

A Narrative is your structured view of a company, where you spell out what you think will happen to its revenue, earnings and margins, connect that view to a financial forecast, and then translate it into a fair value per share.

On Simply Wall St’s Community page, used by millions of investors, Narratives are an easy to use tool that show you, in one place, the link between a company’s story, its projected financials and the resulting Fair Value. You can then compare this directly with today’s share price to decide whether it looks like a buy, hold, or sell.

Because Narratives update dynamically when fresh information arrives, such as new earnings or major news, your fair value view can evolve in real time. For Rithm Capital, that means you can quickly see why one investor’s bullish Narrative might point to a fair value near $16.0 while a more cautious Narrative lands closer to $12.5.

Do you think there's more to the story for Rithm Capital? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:RITM

Rithm Capital

Operates as an asset manager focused on real estate, credit, and financial services in the United States.

Very undervalued with solid track record.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.4% undervalued

41 followersusers have followed this narrative

6 commentsusers have commented on this narrative

12 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$123.8% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$244.5% overvalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

SC

scm on Text ·

TXT will see revenue grow 26% with a profit margin boost of almost 40%

Fair Value:zł8048.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VL

Vladislav on Galleon Gold ·

Significantly undervalued gold explorer in Timmins, finally getting traction

Fair Value:CA$482.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

FU

FundamentallySarcastic on Credit Corp Group ·

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Fair Value:AU$12.6411.8% overvalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

115 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3928.3% undervalued

954 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3406.0% undervalued

147 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative