Advertisement

- United States

- /

- Consumer Finance

- /

- NYSE:OMF

It Might Not Be A Great Idea To Buy OneMain Holdings, Inc. (NYSE:OMF) For Its Next Dividend

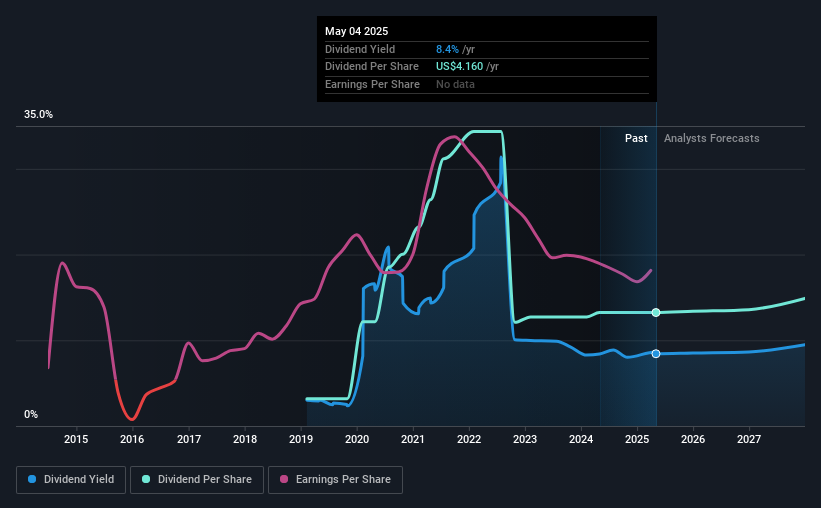

It looks like OneMain Holdings, Inc. (NYSE:OMF) is about to go ex-dividend in the next 4 days. The ex-dividend date is one business day before the record date, which is the cut-off date for shareholders to be present on the company's books to be eligible for a dividend payment. The ex-dividend date is important because any transaction on a stock needs to have been settled before the record date in order to be eligible for a dividend. Therefore, if you purchase OneMain Holdings' shares on or after the 9th of May, you won't be eligible to receive the dividend, when it is paid on the 16th of May.

The company's next dividend payment will be US$1.04 per share. Last year, in total, the company distributed US$4.16 to shareholders. Based on the last year's worth of payments, OneMain Holdings stock has a trailing yield of around 8.4% on the current share price of US$49.35. If you buy this business for its dividend, you should have an idea of whether OneMain Holdings's dividend is reliable and sustainable. As a result, readers should always check whether OneMain Holdings has been able to grow its dividends, or if the dividend might be cut.

We've discovered 2 warning signs about OneMain Holdings. View them for free.Dividends are typically paid out of company income, so if a company pays out more than it earned, its dividend is usually at a higher risk of being cut. Its dividend payout ratio is 88% of profit, which means the company is paying out a majority of its earnings. The relatively limited profit reinvestment could slow the rate of future earnings growth. We'd be concerned if earnings began to decline.

Generally speaking, the lower a company's payout ratios, the more resilient its dividend usually is.

See our latest analysis for OneMain Holdings

Click here to see the company's payout ratio, plus analyst estimates of its future dividends.

Have Earnings And Dividends Been Growing?

Companies with falling earnings are riskier for dividend shareholders. If earnings decline and the company is forced to cut its dividend, investors could watch the value of their investment go up in smoke. Readers will understand then, why we're concerned to see OneMain Holdings's earnings per share have dropped 5.4% a year over the past five years. Such a sharp decline casts doubt on the future sustainability of the dividend.

Another key way to measure a company's dividend prospects is by measuring its historical rate of dividend growth. In the past six years, OneMain Holdings has increased its dividend at approximately 27% a year on average. That's intriguing, but the combination of growing dividends despite declining earnings can typically only be achieved by paying out a larger percentage of profits. OneMain Holdings is already paying out a high percentage of its income, so without earnings growth, we're doubtful of whether this dividend will grow much in the future.

The Bottom Line

Is OneMain Holdings worth buying for its dividend? Earnings per share have been declining and the company is paying out more than half its profits to shareholders; not an enticing combination. This is not an overtly appealing combination of characteristics, and we're just not that interested in this company's dividend.

Although, if you're still interested in OneMain Holdings and want to know more, you'll find it very useful to know what risks this stock faces. For example, OneMain Holdings has 2 warning signs (and 1 which makes us a bit uncomfortable) we think you should know about.

Generally, we wouldn't recommend just buying the first dividend stock you see. Here's a curated list of interesting stocks that are strong dividend payers.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:OMF

OneMain Holdings

A financial service holding company, engages in the consumer finance and insurance businesses in the United States.

High growth potential average dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|40.3% undervalued

JO

Community Contributor

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|7.9% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|31.6% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$359.72|12.3% undervalued

BL

Community Contributor