Advertisement

- United States

- /

- Diversified Financial

- /

- NYSE:NATL

NCR Atleos (NYSE:NATL): Assessing Valuation After Securing Moto Partnership and Expanding UK ATM Footprint

Simply Wall St

Reviewed by Kshitija Bhandaru

NCR Atleos (NYSE:NATL) just revealed that Moto, the largest motorway service operator in the UK, will continue relying on its Cashzone Network, which now supports over 16,000 ATMs nationwide. This development highlights NCR Atleos’ capacity to grow strategic relationships and strengthen its presence in the UK market.

See our latest analysis for NCR Atleos.

Following the Moto extension, NCR Atleos has maintained upward momentum, with a 36.6% share price return over the past three months and a robust 33.1% total return for investors over the past year. This performance suggests optimism around the company’s expanding UK presence and signals that growth potential remains in focus.

If strategic moves like this have you thinking about broader opportunities, now is a great time to check out fast growing stocks with high insider ownership.

With shares currently trading at a discount to analyst targets and strong earnings growth in recent quarters, the key question for investors is whether NCR Atleos represents an undervalued opportunity or if the market has already considered its future growth potential.

Most Popular Narrative: 14.7% Undervalued

With NCR Atleos closing at $38.08 and the most recent narrative giving a fair value near $44.67, there are clear expectations for future upside. The narrative’s valuation is closely tied to substantial shifts unfolding in how financial institutions adopt and grow ATM-as-a-Service revenues.

The rapid growth and backlog in NCR Atleos' ATM-as-a-Service business (32% revenue growth in Q2, 105% YoY backlog increase) signals accelerating demand for outsourced, integrated cash management as banks digitize and automate cash operations. This trend is setting up recurring, high-margin revenue growth into 2026 and beyond.

Want to know what powers this bullish view? The numbers behind this valuation hinge on aggressive growth in recurring revenue, expected margin boosts, and a major reset in the profit multiple. One framework and some very bold projections—see what they are.

Result: Fair Value of $44.67 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, increased competition from fintechs and greater adoption of digital banking could limit NCR Atleos' recurring revenue potential in the years ahead.

Find out about the key risks to this NCR Atleos narrative.

Another View: What Do the Multiples Say?

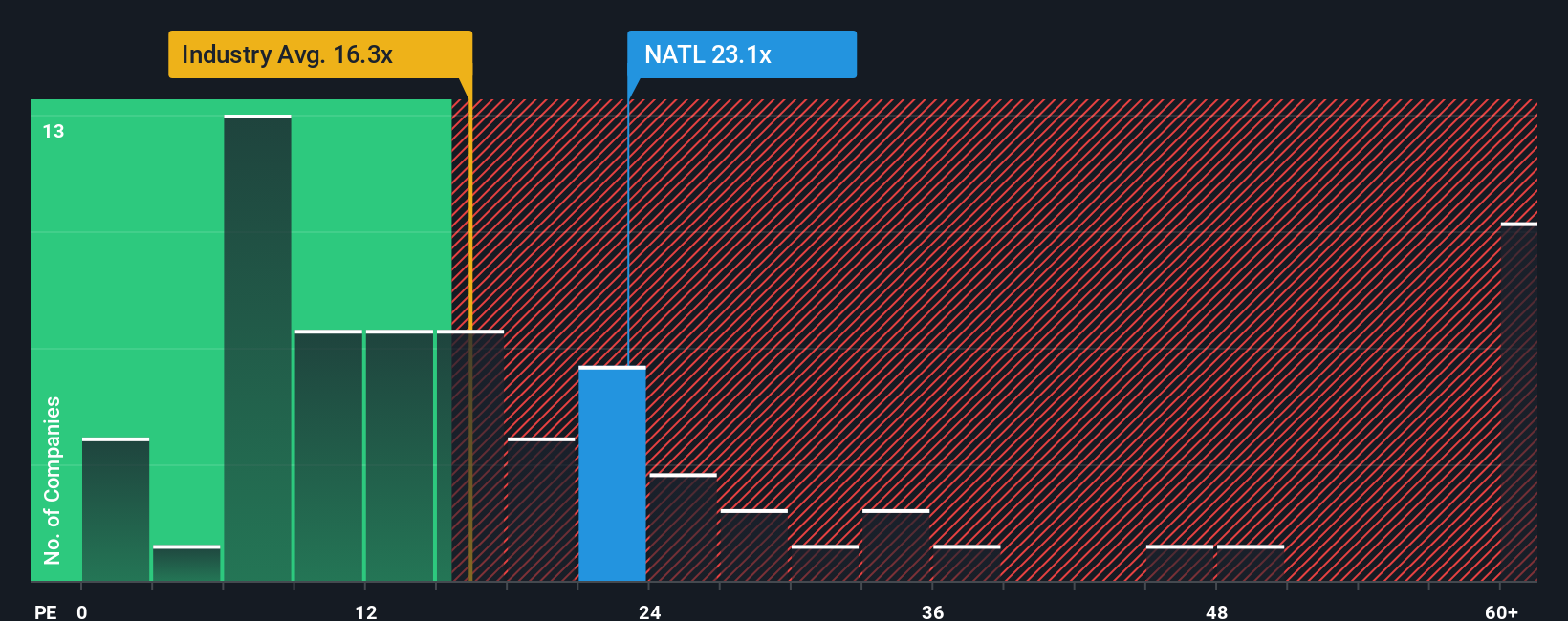

Looking from a price-to-earnings perspective, NCR Atleos trades at 21.9x, which is notably higher than both the US Diversified Financial industry average of 16x and its peer average of 11.3x. This premium may imply heightened expectations, especially since the fair ratio sits closer to 19.4x. Does the market see more upside, or is there valuation risk baked in?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own NCR Atleos Narrative

If the consensus doesn't match your outlook or you want to dig into the numbers yourself, it takes just a few minutes to shape your own view. Do it your way.

A great starting point for your NCR Atleos research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Act now to find investment opportunities you might be missing. The smartest investors expand their research beyond one company. Don’t let new possibilities pass you by!

- Find companies dominating AI innovation and technology breakthroughs by reviewing these 24 AI penny stocks, which could shape tomorrow’s leaders.

- Target attractive long-term yields and steady cash flow by checking out these 18 dividend stocks with yields > 3% returning over 3%.

- Tap into the potential of secure blockchain and digital asset growth by considering these 79 cryptocurrency and blockchain stocks, ready to transform the next wave of finance.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if NCR Atleos might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:NATL

NCR Atleos

A financial technology company, provides self-directed banking solutions to financial institutions, merchants, manufacturers, retailers, and consumers in the United States, rest of the Americas, Europe, the Middle East, Africa, and the Asia Pacific.

Reasonable growth potential with very low risk.

Similar Companies

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|13.6% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$89.00|23.6% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|37.6% undervalued

TR

Community Contributor