Advertisement

- United States

- /

- Diversified Financial

- /

- NYSE:MA

Is Mastercard’s Premium Valuation Justified After Recent Digital Wallet Partnership?

Simply Wall St

Reviewed by Bailey Pemberton

Deciding what to do with your Mastercard shares right now? You are not alone, and for good reason. Mastercard’s journey in recent years reads like a highlight reel of steady gains, with a five-year return of 76.1% and a 92.4% return over three years. Even a quick glance at its one-year return of 12.6% shows resilient growth, despite modest stumbles in the past month and week, down 2.2% and 2.1% respectively. These short-term dips are drawing attention as investors weigh what is driving them: broader shifts in payment technology, ongoing debates about digital payment competition, and evolving consumer trends that keep Mastercard right at the center of financial conversation. Meanwhile, Mastercard’s year-to-date gain of 8.7% reflects ongoing optimism, even as sentiment about the sector has become a bit more cautious.

But with the stock closing most recently at $567.92, the question on many investors’ minds is whether Mastercard still offers good value or if future growth is already baked into the current price. Backed by a value score of just 1 out of 6 (meaning Mastercard is currently considered undervalued by only one method out of six), the numbers suggest this is far from a classic value play. So how does Mastercard measure up when you put its valuation under a microscope? Let’s break down the main valuation approaches most analysts use, and then take it a step further with an even more insightful perspective you will not want to miss.

Mastercard scores just 1/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Mastercard Excess Returns Analysis

The Excess Returns valuation model is designed to determine how much value a company creates above the minimum return required by its investors, based on return on equity relative to the cost of equity. In this approach, the focus is on how efficiently Mastercard converts shareholders' capital into profits and by how wide a margin over its cost of equity.

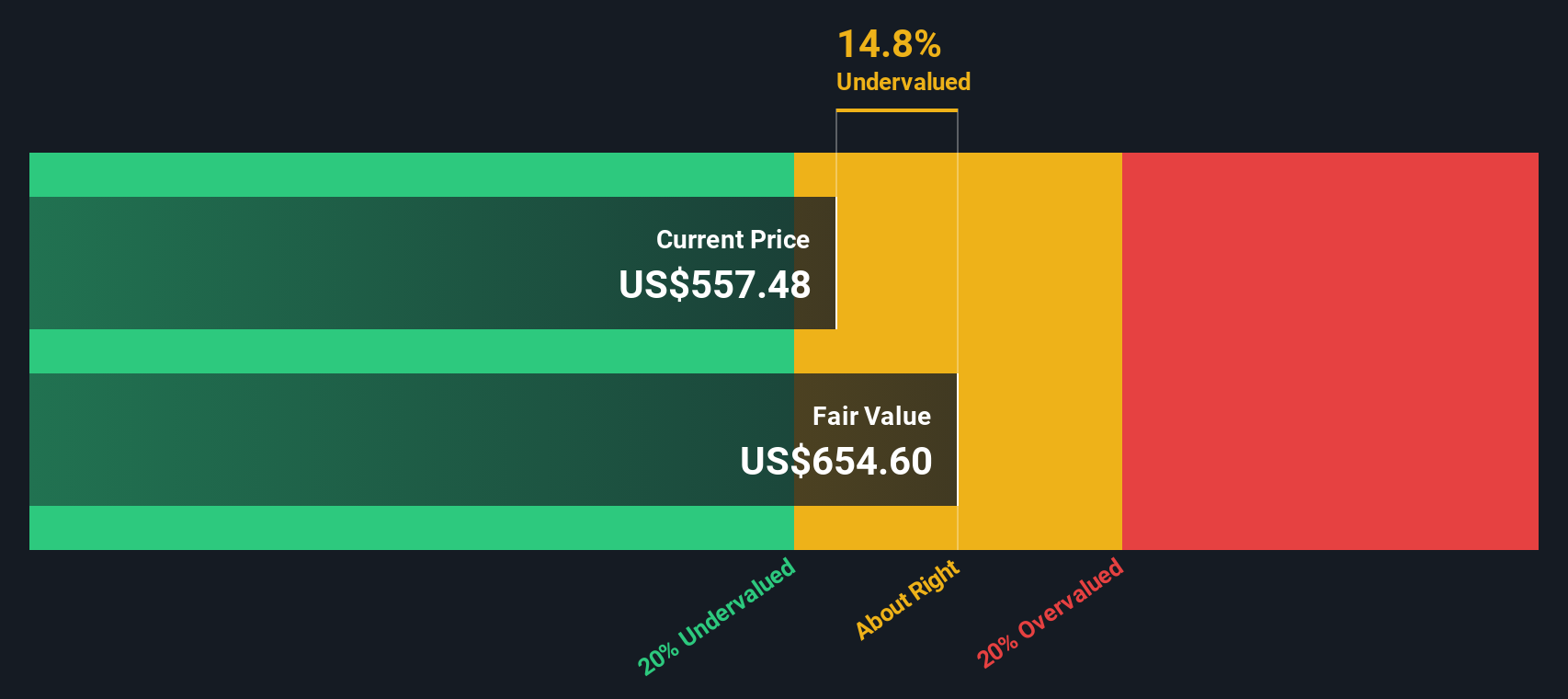

For Mastercard, the figures are striking. The company's average return on equity is exceptionally high at 195.26%, underpinned by a projected stable earnings per share of $28.96 (according to weighted future Return on Equity estimates from 12 analysts). The stable book value per share is estimated at $14.83, while the latest reported book value per share stands at $8.67. Importantly, Mastercard's cost of equity is calculated at just $1.10 per share. This means the company is producing an excess return of $27.85 per share each year.

Taking this into account, the Excess Returns model estimates Mastercard's intrinsic value at $654.35 per share. Given the recent market price of $567.92, this suggests the stock is trading at a 13.2% discount to its estimated fair value, indicating that Mastercard remains undervalued on this measure.

Result: UNDERVALUED

Our Excess Returns analysis suggests Mastercard is undervalued by 13.2%. Track this in your watchlist or portfolio, or discover more undervalued stocks.

Approach 2: Mastercard Price vs Earnings

The Price-to-Earnings (PE) ratio is often considered the go-to metric for valuing consistently profitable companies like Mastercard. This multiple provides a snapshot of how much investors are willing to pay for a dollar of the company’s earnings. It is a useful gauge for growth stocks with strong profit histories.

The “right” PE ratio depends on a company’s growth potential and its perceived risk. Typically, companies expected to grow faster or with more stable earnings can justify higher PE ratios. In contrast, slower growth or elevated risk tends to result in lower PE ratios.

Mastercard’s current PE ratio is 37.8x. For context, the broader Diversified Financial industry trades at an average of 15.6x, and Mastercard’s peer group averages 20.8x. By comparison, Mastercard’s PE is well above both benchmarks, which may suggest that the market is pricing in premium growth or quality.

The Simply Wall St Fair Ratio for Mastercard is 22.9x. This proprietary metric sets a fair-value anchor by considering specific company attributes such as anticipated earnings growth, profitability, industry profile, market capitalization, and relevant risks. Unlike a simple industry or peer comparison, this tailored measure reflects Mastercard’s unique combination of scale, quality, and growth potential.

Comparing Mastercard’s current PE of 37.8x with its Fair Ratio of 22.9x, the stock appears to be trading at a sizable premium to its fair value based on expected earnings growth and risk factors.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Mastercard Narrative

Earlier we mentioned there is an even better way to approach valuation, so let’s introduce you to Narratives. A Narrative is more than just a number; it is your story and perspective on a company, connecting how you see Mastercard’s future to specific forecasts of revenue, profits, and fair value. Rather than relying solely on static ratios, Narratives help you articulate your outlook and tie it together with a dynamic financial forecast that automatically updates with new earnings reports or breaking news.

On Simply Wall St’s Community page, Narratives are an easy and accessible tool used by millions of investors, enabling you to set your own assumptions for Mastercard and instantly see whether you would buy, hold, or sell based on the fair value compared to today’s market price. Narratives make your investing process smarter by adjusting to new information and letting you see how your view stacks up against thousands of others, highlighting investor consensus, optimism, or caution in real time.

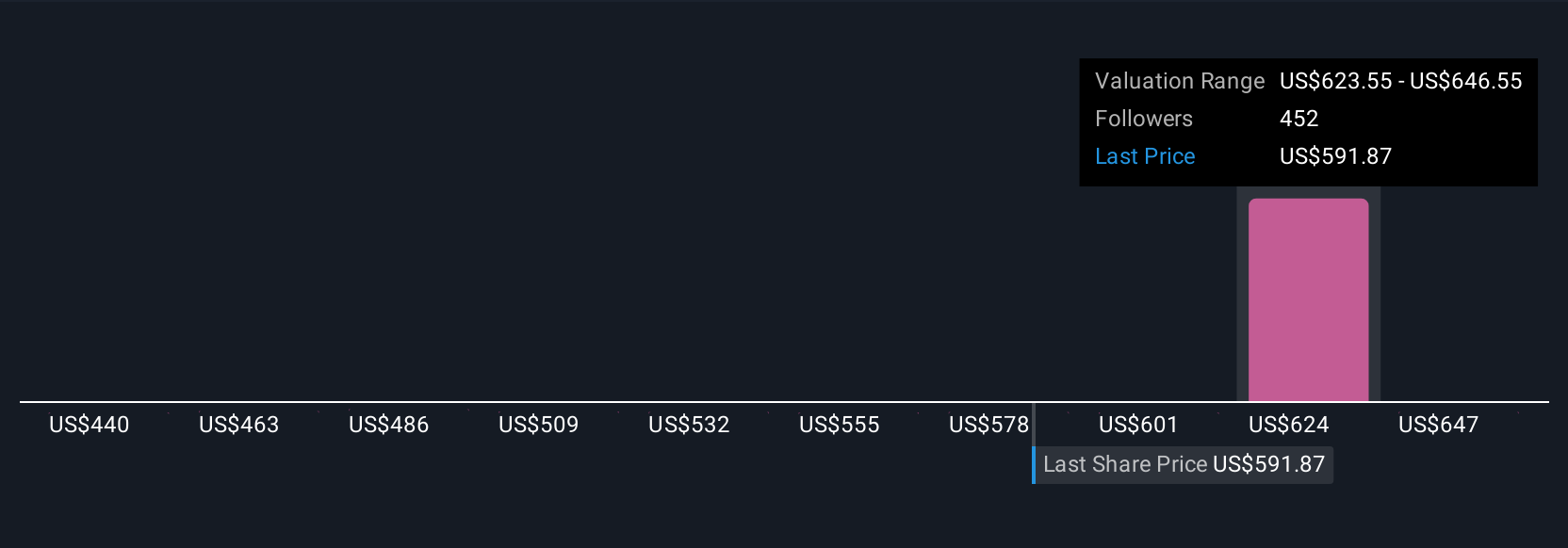

For example, some investors currently believe Mastercard’s fair value is as high as $690, focusing on its digital payments expansion, while others estimate just $520, emphasizing global competition and regulatory risks. This shows how your Narrative can reveal what matters most to you in your investment decision.

Do you think there's more to the story for Mastercard? Create your own Narrative to let the Community know!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:MA

Mastercard

A technology company, provides transaction processing and other payment-related products and services in the United States and internationally.

Moderate growth potential with acceptable track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|3.9% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|4.1% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|39.4% undervalued

TR

Community Contributor