Advertisement

- United States

- /

- Consumer Finance

- /

- NYSE:ENVA

Enova International (ENVA): Assessing Valuation After Strong Q3 Growth and Liquidity Extension

Simply Wall St

Reviewed by Simply Wall St

Enova International (ENVA) just reported Q3 results featuring a 16% increase in revenue and a 29% jump in small business lending. The company is also taking steps to shore up liquidity by extending its OnDeck Receivables facility.

See our latest analysis for Enova International.

Momentum is clearly building for Enova International, as investors have rewarded the company’s double-digit lending growth and recent liquidity moves with a 36% year-to-date share price return. Enova’s one-year total shareholder return of 24% highlights both near-term enthusiasm and solid long-term performance. Executive confidence and favorable industry trends also remain important factors for the company.

If you’re interested in finding other companies with rapid growth and strong leadership, now’s a great moment to explore fast growing stocks with high insider ownership

With the stock up more than 35% so far this year and growth trends firmly in place, investors have to ask whether Enova International is trading below its potential, or if the market is already factoring in further gains.

Most Popular Narrative: 6.8% Undervalued

Enova International’s most widely followed narrative estimates fair value at $140.63, placing it around $10 above the last close. This suggests the consensus expects further upside, given the company’s recent performance surge and resilient sector position.

The ongoing migration of small businesses and consumers toward digital lending, supported by preferences for speed and convenience, continues to drive strong demand and originations for Enova. The company is well-positioned with its online-only business model, supporting sustained top-line growth as reflected in record origination and revenue increases.

What is the basis for this optimistic price target? The story connects digital dominance with bold financial projections, combining both scale and speed. Interested in the numbers backing these expectations? Only the full narrative reveals how analyst forecasts and efficiency assumptions generate this valuation outlook.

Result: Fair Value of $140.63 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, rising regulatory scrutiny or a major uptick in loan losses could quickly challenge these optimistic assumptions and shift the outlook for Enova International.

Find out about the key risks to this Enova International narrative.

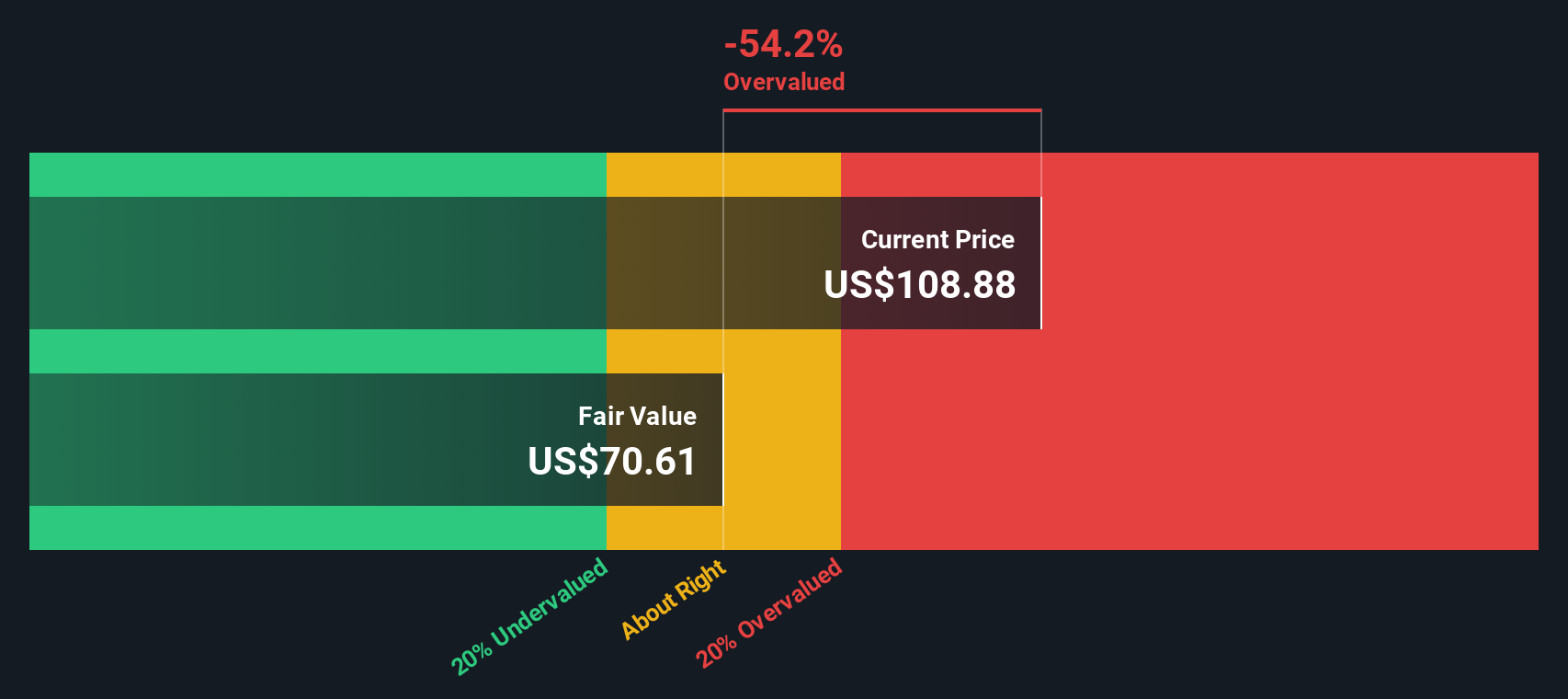

Another View: Our DCF Model’s Estimate

There is another angle to consider. The SWS DCF model, which analyzes Enova International’s forecast cash flows, arrives at a fair value of $77.77 per share. This is far below both the current price and the recent consensus. This approach suggests the stock may be overvalued if those cash flow assumptions hold. Could the DCF model be underestimating the upside, or does it highlight real risks that multiples miss?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Enova International for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 920 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Enova International Narrative

If you see the numbers differently or want to draw your own conclusions, you can investigate the details and build your own perspective in just minutes. Do it your way

A great starting point for your Enova International research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Thousands of investors are gaining an edge by spotting fresh trends before the crowd. If you want to broaden your approach and uncover the next big winners, check out these unique opportunities:

- Pinpoint stocks that could break out in 2024 by checking out these 920 undervalued stocks based on cash flows, which highlights cash flow bargains with hidden upside potential.

- Capitalize on the AI revolution and gain exposure to tomorrow’s high flyers with these 25 AI penny stocks, featuring companies with strong growth trajectories and real-world impact.

- Seize income opportunities by reviewing these 15 dividend stocks with yields > 3%, designed for investors seeking yields above 3% and solid fundamentals.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Enova International might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:ENVA

Enova International

A technology and analytics company, provides online financial services in the United States, Brazil, and internationally.

Reasonable growth potential with proven track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

30 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on IMPACT Silver ·

A case for for IMPACT Silver Corp (TSXV:IPT) to reach USD $4.52 (CAD $6.16) in 2026 (23 bagger in 1 year) and USD $5.76 (CAD $7.89) by 2030

Fair Value:CA$7.8996.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

138 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

930 followersusers have followed this narrative

6 commentsusers have commented on this narrative

23 likesusers have liked this narrative