Advertisement

- United States

- /

- Consumer Finance

- /

- NYSE:COF

How Recent Credit Headlines Could Affect Capital One’s True Value in 2025

Simply Wall St

Reviewed by Bailey Pemberton

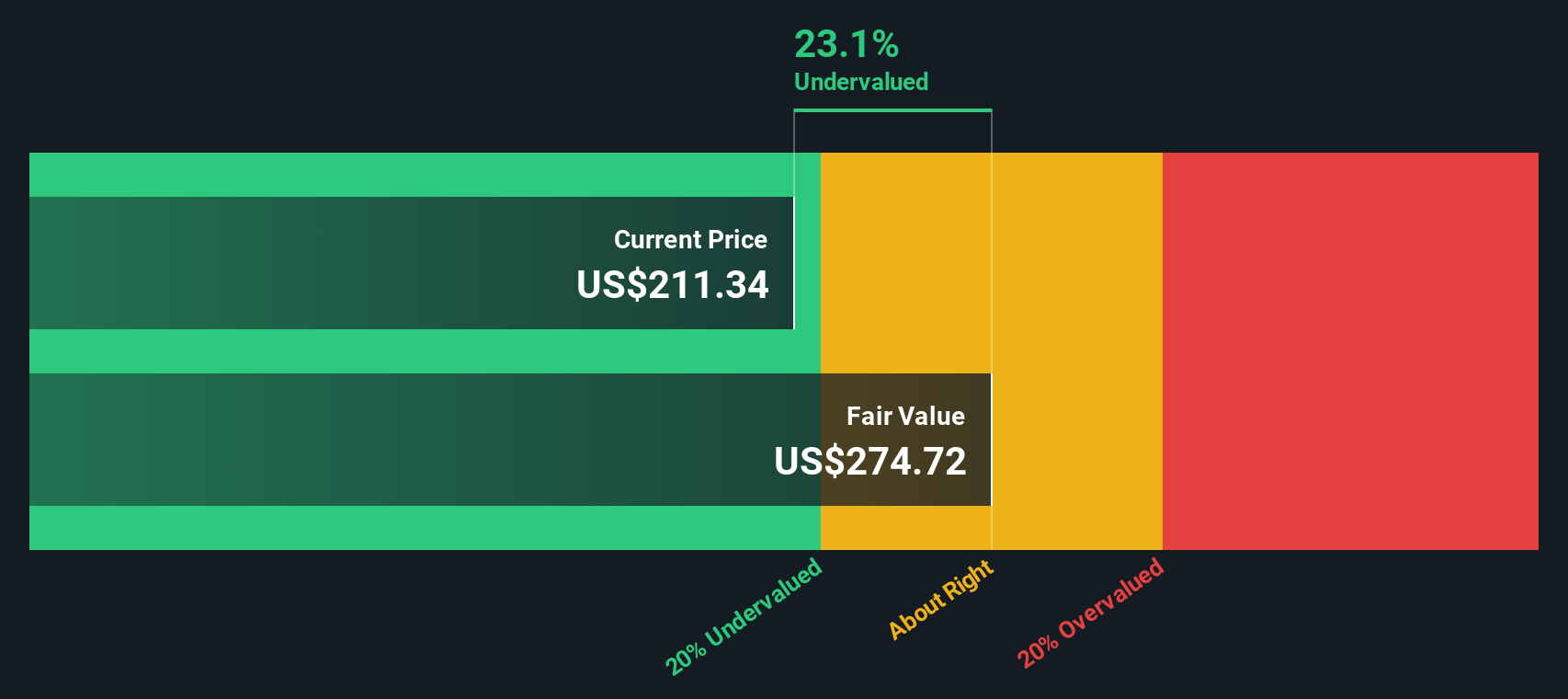

- Wondering if Capital One Financial is a steal at today’s price, or if you might be better off looking elsewhere? You are not alone. There are some fresh numbers and factors to consider.

- The stock has delivered a robust 21.7% gain year-to-date and is up 15.1% in the past year. It has seen some recent swings with a 7.4% bump in the last week and a slight dip of -2.7% over the last month.

- Market sentiment has been shifting for Capital One. Analysts and investors have taken notice after a series of headlines spotlighted credit trends and shifts in consumer lending. Regulatory changes and evolving fintech competition are also in focus, sparking discussion about the company’s position in a changing industry landscape.

- On our valuation scoreboard, Capital One earns a 2 out of 6. This suggests there may be some overlooked aspects, but it also raises important questions. In this article, we will break down what goes into that score, compare the major valuation approaches, and show you a powerful perspective on value you will not want to miss by the end.

Capital One Financial scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Capital One Financial Excess Returns Analysis

The Excess Returns model offers a straightforward approach to valuation by examining whether the company is earning a return above its cost of equity. In other words, the model tracks how efficiently Capital One Financial generates profits with shareholder capital after accounting for the minimum rate investors expect as compensation for risk.

Key inputs for this analysis include a current Book Value per share of $170.52 and a Stable EPS (earnings per share) of $22.15, supported by forecasts from nine analysts. The company’s Cost of Equity stands at $16.12 per share, while the calculated Excess Return per share is $6.03. This suggests that Capital One is generating a 12.03% average Return on Equity, exceeding the required rate and highlighting a consistent profitability advantage. Looking forward, the Stable Book Value is projected at $184.10 per share based on input from eight analysts.

Using these projections, the Excess Returns model estimates an intrinsic value for Capital One Financial that implies the shares are currently 26.0% undervalued compared to the market price. This indicates there may be meaningful upside potential if these profitability trends hold.

Result: UNDERVALUED

Our Excess Returns analysis suggests Capital One Financial is undervalued by 26.0%. Track this in your watchlist or portfolio, or discover 926 more undervalued stocks based on cash flows.

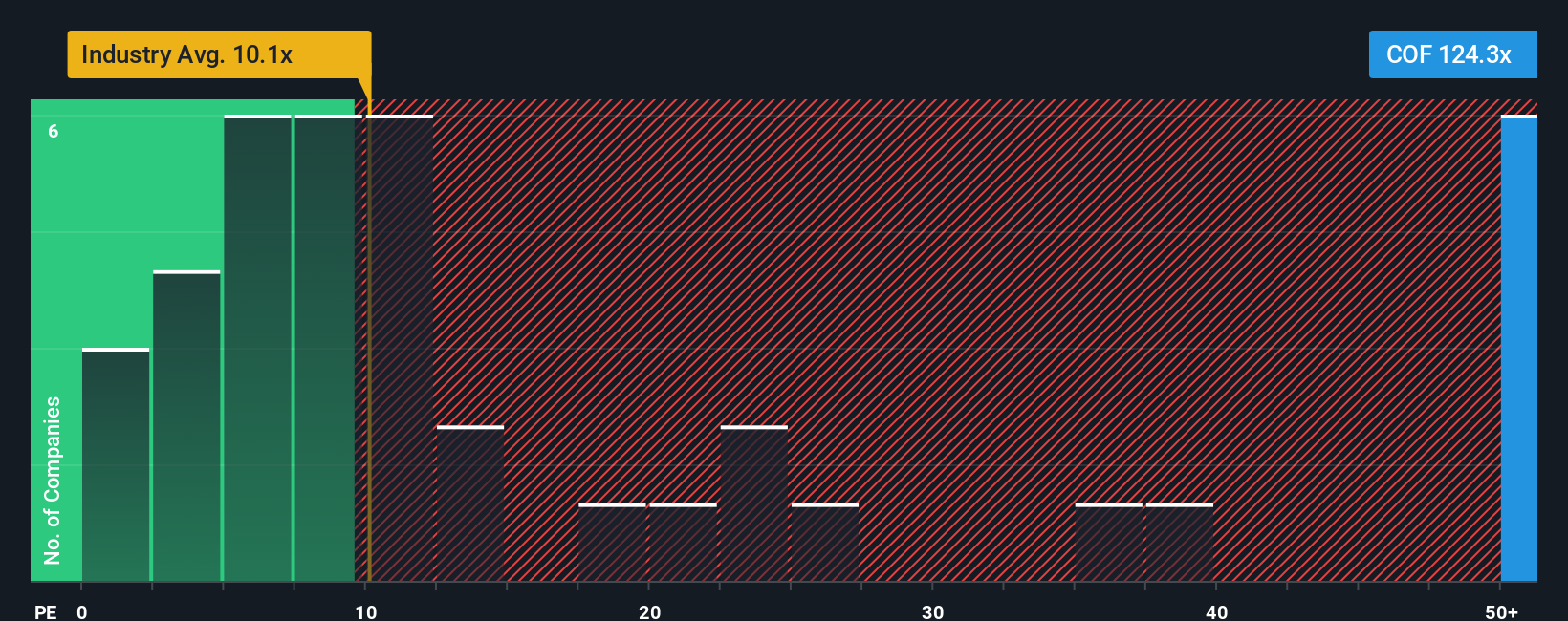

Approach 2: Capital One Financial Price vs Earnings

The Price-to-Earnings (PE) ratio is a favored metric for valuing profitable companies such as Capital One Financial because it directly connects a company’s market price to its ongoing earnings power. This approach helps investors gauge how much they are paying for every dollar of current earnings, making it a clear lens for understanding valuation, especially among companies with consistent profits.

Industry norms suggest that the "right" PE ratio depends on expected growth and risk factors. Companies with brighter growth prospects or lower perceived risks typically command higher PE multiples, while slower growers or riskier businesses are valued on the lower end. For Capital One, the current PE ratio stands at 120.12x, which is considerably higher than both the industry average of 9.72x and the peer group’s average of 27.47x.

Instead of relying solely on crude comparisons, the Simply Wall St Fair Ratio offers a more tailored benchmark. It incorporates not just industry and peer comparisons but also considers Capital One’s unique growth outlook, profit margins, market size, and risk profile. For Capital One Financial, the Fair Ratio is estimated at 34.53x. This provides investors with a nuanced assessment that reflects the specifics of the business, rather than just a surface-level comparison.

With Capital One’s PE ratio of 120.12x compared to its Fair Ratio of 34.53x, the stock appears meaningfully overpriced based on current earnings and outlook.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1433 companies where insiders are betting big on explosive growth.

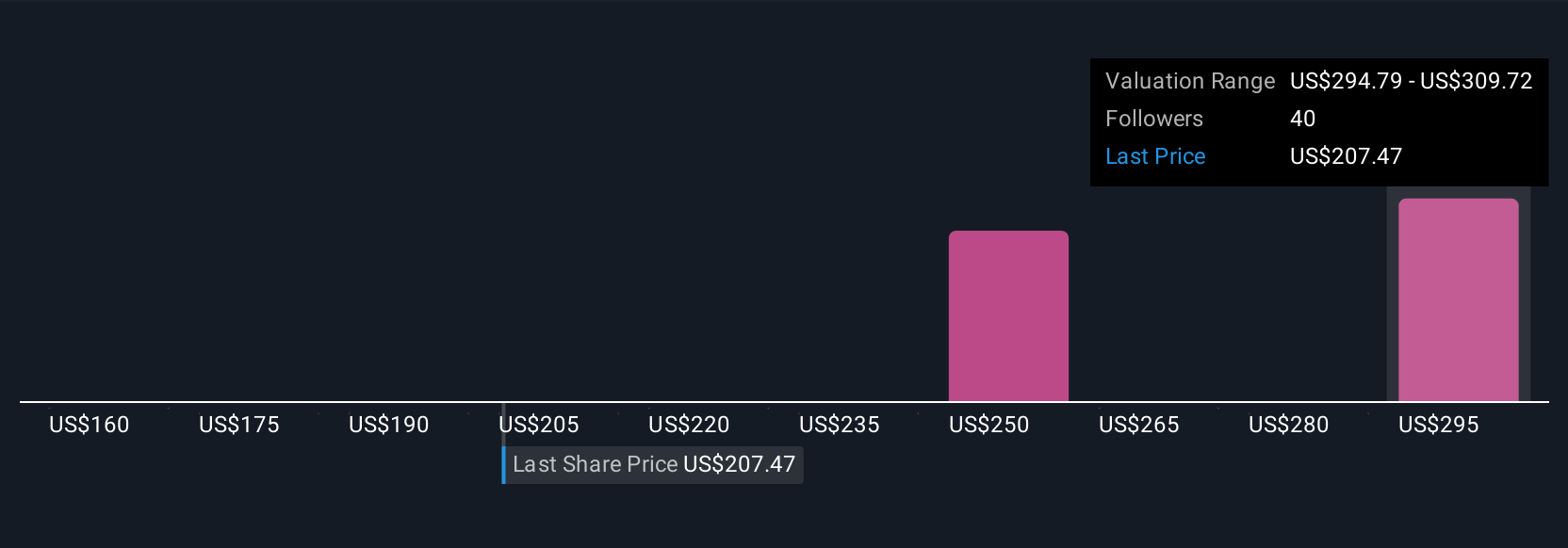

Upgrade Your Decision Making: Choose your Capital One Financial Narrative

Earlier we mentioned that there is an even better way to understand valuation. Let us introduce you to Narratives. A Narrative is your own perspective about a company’s future, linking the company’s story directly to the numbers: your fair value estimate and expectations for revenue, earnings, and margins. Instead of relying just on formulas or static forecasts, Narratives let investors map out what they believe is likely to happen and see how those beliefs convert into fair value estimates in real time.

With Simply Wall St’s Community page, millions of investors can build, refine, and share Narratives for companies like Capital One Financial. Narratives are easy to create and keep up to date. Whenever new reports or news come in, the numbers refresh automatically, so your story always matches the latest reality. This tool helps you decide whether to buy or sell by showing you the “Fair Value” from your Narrative compared with today's market price, making it clear if your expectations line up with opportunity or risk.

For Capital One Financial, for instance, some investors believe earnings and revenue will exceed expectations, setting a fair value above $265, while others worry about challenges like integration risks or margin pressure, resulting in a fair value as low as $160. Narratives make it easy to see and act on the story that fits your outlook.

Do you think there's more to the story for Capital One Financial? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:COF

Capital One Financial

Operates as the financial services holding company for the Capital One, National Association, which engages in the provision of various financial products and services in the United States, Canada, and the United Kingdom.

Flawless balance sheet with high growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.6% undervalued

TI

Community Contributor

Recently Updated Narratives

BL

BlackGoat on Alphabet ·

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value:US$324.481.3% undervalued

76 followersusers have followed this narrative

3 commentsusers have commented on this narrative

1 likeusers have liked this narrative

BE

Bejgal on MINISO Group Holding ·

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value:US$26.6926.7% undervalued

45 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TI

TickerTickle on Oracle ·

The Quiet Giant That Became AI’s Power Grid

Fair Value:US$389.8147.4% undervalued

9 followersusers have followed this narrative

1 commentusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

89 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

927 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative