The board of SLM Corporation (NASDAQ:SLM) has announced that it will pay a dividend on the 15th of December, with investors receiving $0.11 per share. This payment means that the dividend yield will be 2.6%, which is around the industry average.

Our analysis indicates that SLM is potentially undervalued!

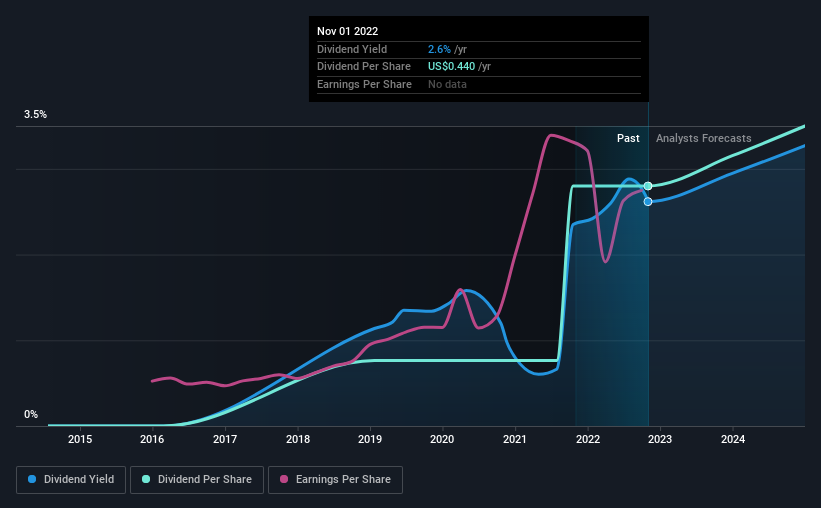

SLM's Payment Has Solid Earnings Coverage

We like a dividend to be consistent over the long term, so checking whether it is sustainable is important. Prior to this announcement, SLM's dividend was only 14% of earnings, however it was paying out 214% of free cash flows. The business might be trying to strike a balance between returning cash to shareholders and reinvesting back into the business, but this high of a payout ratio could definitely force the dividend to be cut if the company runs into a bit of a tough spot.

The next year is set to see EPS grow by 22.8%. If the dividend continues along recent trends, we estimate the payout ratio will be 16%, which is in the range that makes us comfortable with the sustainability of the dividend.

SLM Doesn't Have A Long Payment History

The company has maintained a consistent dividend for a few years now, but we would like to see a longer track record before relying on it. The dividend has gone from an annual total of $0.12 in 2018 to the most recent total annual payment of $0.44. This means that it has been growing its distributions at 38% per annum over that time. It is always nice to see strong dividend growth, but with such a short payment history we wouldn't be inclined to rely on it until a longer track record can be developed.

The Dividend Looks Likely To Grow

The company's investors will be pleased to have been receiving dividend income for some time. We are encouraged to see that SLM has grown earnings per share at 38% per year over the past five years. Earnings have been growing rapidly, and with a low payout ratio we think that the company could turn out to be a great dividend stock.

Our Thoughts On SLM's Dividend

Overall, it's nice to see a consistent dividend payment, but we think that longer term, the current level of payment might be unsustainable. While SLM is earning enough to cover the payments, the cash flows are lacking. Overall, we don't think this company has the makings of a good income stock.

It's important to note that companies having a consistent dividend policy will generate greater investor confidence than those having an erratic one. Still, investors need to consider a host of other factors, apart from dividend payments, when analysing a company. Case in point: We've spotted 3 warning signs for SLM (of which 2 don't sit too well with us!) you should know about. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:SLM

SLM

Through its subsidiaries, originates and services private education loans to students and their families to finance the cost of their education in the United States.

Undervalued with acceptable track record.