Advertisement

- United States

- /

- Diversified Financial

- /

- NasdaqCM:SEZL

Sezzle (SEZL) Stock Rebounds: Revisiting the Valuation Case After Recent Share Price Strength

Simply Wall St

Reviewed by Simply Wall St

Why Sezzle Stock Is Back on Traders Radar

Sezzle (SEZL) has quietly climbed about 4% in a day and roughly 13% over the past week, putting the buy now, pay later player back in focus after a choppy past 3 months.

See our latest analysis for Sezzle.

With the share price now at $66.72 and a strong year to date share price return alongside only modest 1 year total shareholder return, Sezzle looks like a name where momentum is rebuilding as investors reassess its growth and risk profile.

If Sezzle’s rebound has you watching the broader payments and fintech space, it could be worth exploring fast growing stocks with high insider ownership for other fast moving opportunities.

With Sezzle trading well below analyst targets yet already boasting robust growth and profitability metrics, investors now face a key question: is this a mispriced fintech still catching up, or has the market already baked in its next leg of expansion?

Most Popular Narrative Narrative: 38.5% Undervalued

With Sezzle closing at $66.72 versus a narrative fair value of $108.50, the spread reflects ambitious growth assumptions that go far beyond recent share moves.

Ongoing investment in efficient, data-driven customer acquisition (marketing spend increase to $8.8 million with a targeted six-month payback and rapid ramp in high-LTV "mod" users) positions Sezzle to capitalize on the global shift toward digital payments, supporting expanding total addressable market (revenue growth) and potential for operating leverage (margin improvement) as investments mature.

Curious how aggressive growth, firm margins, and a richer earnings profile can still argue for a steep upside from here? The full narrative unpacks the bold revenue path, the profit runway, and the valuation multiple that ties it all together, but only if the projections hold.

Result: Fair Value of $108.50 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, elevated marketing spend and rising credit losses could quickly erode today’s margin story if user quality or repayment behavior deteriorates.

Find out about the key risks to this Sezzle narrative.

Another Angle on Valuation

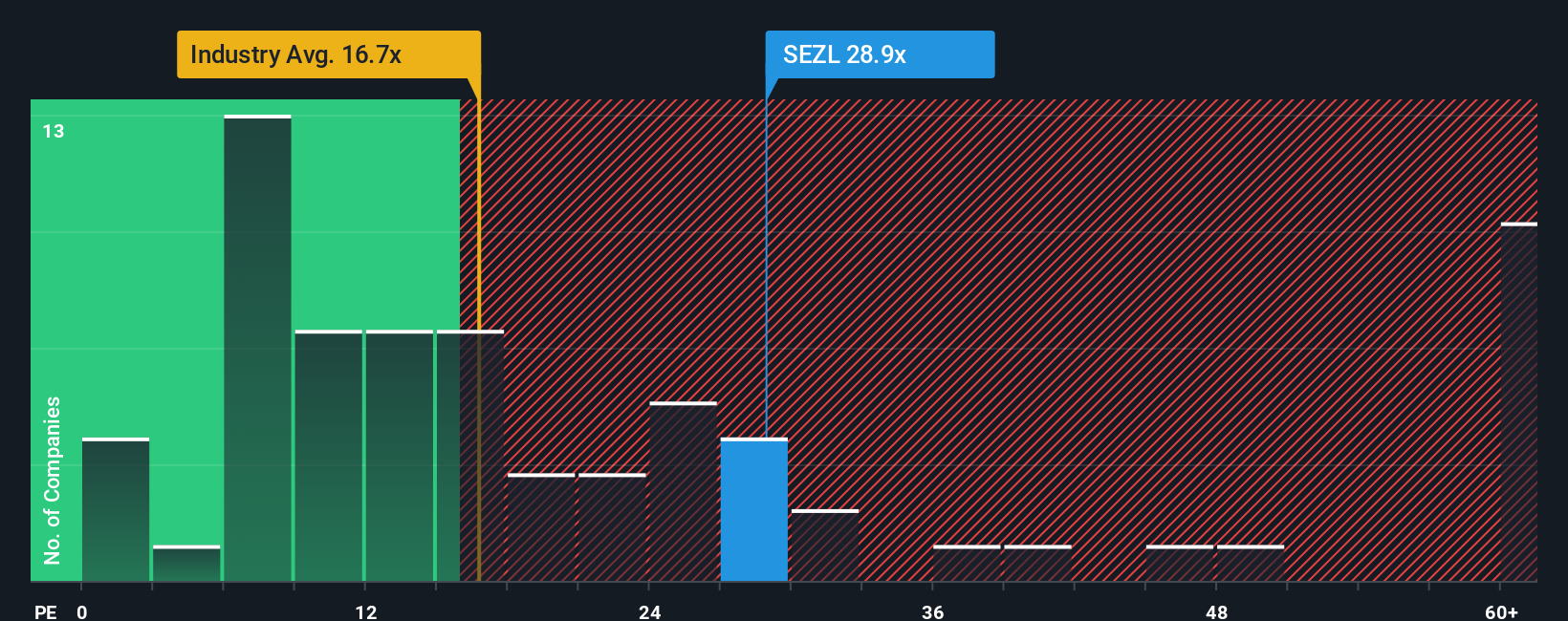

While the narrative fair value suggests Sezzle is meaningfully undervalued, its current price to earnings ratio of 19.7 times complicates the story. That is cheaper than peers at 49.3 times, yet richer than the US diversified financials average of 13.7 times and below a fair ratio of 30.6 times, which hints at both upside potential and re rating risk. Which way will sentiment break if growth stumbles or accelerates?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Sezzle Narrative

If you see the story differently or want to dig into the numbers yourself, you can build a custom view in just minutes. Do it your way.

A great starting point for your Sezzle research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Ready for your next investing move?

Before the market finds them first, use the Simply Wall St Screener to pinpoint fresh opportunities that match your strategy, risk appetite, and return goals.

- Explore potential opportunities in these 3571 penny stocks with strong financials that already show stronger balance sheets and fundamentals than most expect at this end of the market.

- Position ahead of the next wave of innovation by targeting these 26 AI penny stocks that are developing scalable AI driven business models.

- Seek long-term compounding potential through these 15 dividend stocks with yields > 3% that offer meaningful income today along with the possibility of future payout growth.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqCM:SEZL

Sezzle

Operates as a technology-enabled payments company primarily in the United States and Canada.

Flawless balance sheet with high growth potential.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

43 followersusers have followed this narrative

6 commentsusers have commented on this narrative

15 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$123.8% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$247.5% overvalued

8 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

SC

scm on Text ·

TXT will see revenue grow 26% with a profit margin boost of almost 40%

Fair Value:zł8049.8% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VL

Vladislav on Galleon Gold ·

Significantly undervalued gold explorer in Timmins, finally getting traction

Fair Value:CA$482.8% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

FU

FundamentallySarcastic on Credit Corp Group ·

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Fair Value:AU$12.6411.8% overvalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

116 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3928.3% undervalued

955 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3406.6% undervalued

147 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative