Paysign, Inc. (NASDAQ:PAYS) insiders still own 38% despite recent sales, but recent decline may have cost them

Key Insights

- Paysign's significant insider ownership suggests inherent interests in company's expansion

- A total of 5 investors have a majority stake in the company with 52% ownership

- Insiders have sold recently

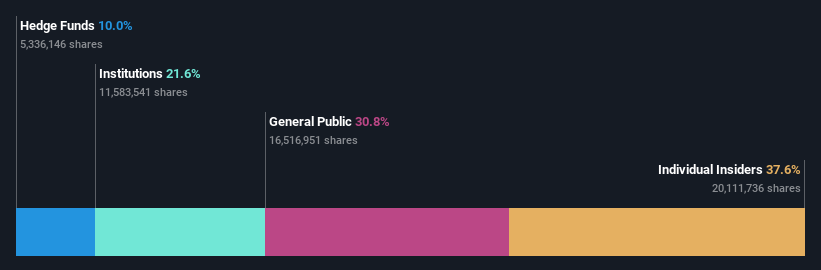

A look at the shareholders of Paysign, Inc. (NASDAQ:PAYS) can tell us which group is most powerful. The group holding the most number of shares in the company, around 38% to be precise, is individual insiders. That is, the group stands to benefit the most if the stock rises (or lose the most if there is a downturn).

Despite recent sales, insiders own the most shares in the company. As a result, the group bore the brunt of last week’s US$19m market cap loss.

In the chart below, we zoom in on the different ownership groups of Paysign.

See our latest analysis for Paysign

What Does The Institutional Ownership Tell Us About Paysign?

Institutional investors commonly compare their own returns to the returns of a commonly followed index. So they generally do consider buying larger companies that are included in the relevant benchmark index.

As you can see, institutional investors have a fair amount of stake in Paysign. This suggests some credibility amongst professional investors. But we can't rely on that fact alone since institutions make bad investments sometimes, just like everyone does. If multiple institutions change their view on a stock at the same time, you could see the share price drop fast. It's therefore worth looking at Paysign's earnings history below. Of course, the future is what really matters.

Our data indicates that hedge funds own 10.0% of Paysign. That's interesting, because hedge funds can be quite active and activist. Many look for medium term catalysts that will drive the share price higher. The company's CEO Mark Newcomer is the largest shareholder with 17% of shares outstanding. With 17% and 10.0% of the shares outstanding respectively, Daniel Spence and Topline Capital Management, LLC are the second and third largest shareholders.

To make our study more interesting, we found that the top 5 shareholders control more than half of the company which implies that this group has considerable sway over the company's decision-making.

While it makes sense to study institutional ownership data for a company, it also makes sense to study analyst sentiments to know which way the wind is blowing. Quite a few analysts cover the stock, so you could look into forecast growth quite easily.

Insider Ownership Of Paysign

While the precise definition of an insider can be subjective, almost everyone considers board members to be insiders. The company management answer to the board and the latter should represent the interests of shareholders. Notably, sometimes top-level managers are on the board themselves.

I generally consider insider ownership to be a good thing. However, on some occasions it makes it more difficult for other shareholders to hold the board accountable for decisions.

Our information suggests that insiders maintain a significant holding in Paysign, Inc.. It has a market capitalization of just US$163m, and insiders have US$61m worth of shares in their own names. It is great to see insiders so invested in the business. It might be worth checking if those insiders have been buying recently.

General Public Ownership

The general public-- including retail investors -- own 31% stake in the company, and hence can't easily be ignored. While this group can't necessarily call the shots, it can certainly have a real influence on how the company is run.

Next Steps:

I find it very interesting to look at who exactly owns a company. But to truly gain insight, we need to consider other information, too. Be aware that Paysign is showing 2 warning signs in our investment analysis , and 1 of those is potentially serious...

If you are like me, you may want to think about whether this company will grow or shrink. Luckily, you can check this free report showing analyst forecasts for its future.

NB: Figures in this article are calculated using data from the last twelve months, which refer to the 12-month period ending on the last date of the month the financial statement is dated. This may not be consistent with full year annual report figures.

Valuation is complex, but we're here to simplify it.

Discover if Paysign might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.