Advertisement

- United States

- /

- Consumer Finance

- /

- NasdaqGS:EZPW

Is EZCORP (EZPW) Still Undervalued After Its Recent Share Price Rally?

Simply Wall St

Reviewed by Simply Wall St

EZCORP (EZPW) has quietly delivered strong gains this year, and the move is catching investor attention. With the pawn and pre-owned retail business humming along, the recent rally raises fair questions about what is already priced in.

See our latest analysis for EZCORP.

The recent climb to a share price of $20.14, backed by a 30 day share price return of 11.89 percent and a 5 year total shareholder return of 294.90 percent, suggests momentum is still building as investors reassess EZCORP’s growth and risk profile.

If EZCORP’s run has you rethinking where to find the next mover, it might be worth exploring fast growing stocks with high insider ownership as a curated set of potential ideas.

With double digit growth in earnings and a share price that still sits below analyst targets, is EZCORP quietly setting up for another move higher, or is the current valuation already factoring in its next phase of expansion?

Most Popular Narrative: 14.7% Undervalued

With the narrative fair value set above EZCORP’s last close of $20.14, the story leans toward upside potential driven by execution and growth.

Enhanced operational efficiency through best practice adoption, advanced pricing and inventory systems, and disciplined cost management is generating recurring operating leverage, as evidenced by multi-quarter EBITDA margin expansion, improving net margins and driving outsized earnings growth relative to revenue.

Curious how steady, mid single digit revenue growth can still justify a richer future earnings multiple than today, even after share count rises and margins climb?

Result: Fair Value of $23.60 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, rising regulatory scrutiny and slower than expected digital adoption could compress margins and stall the operational momentum that underpins the current upside narrative.

Find out about the key risks to this EZCORP narrative.

Another Angle on Valuation

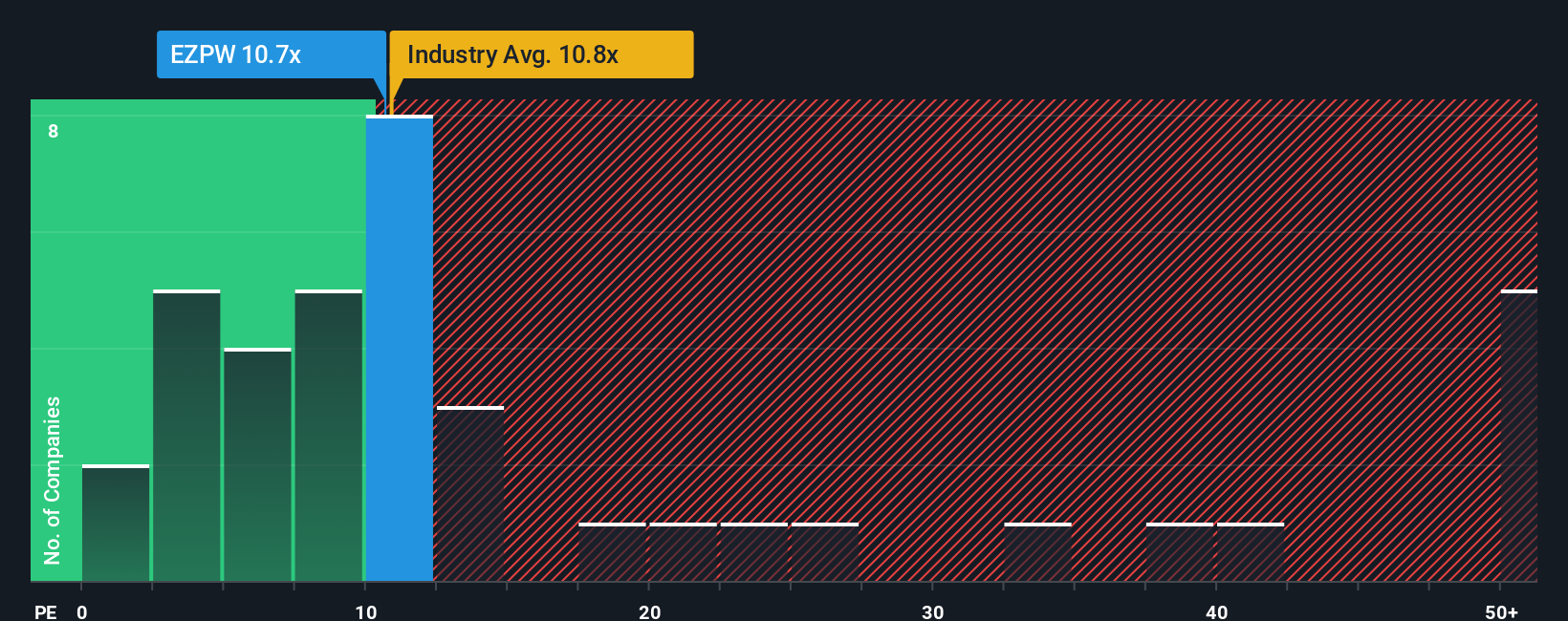

On a simple earnings basis, EZCORP looks less clear cut. Its 11.2x price to earnings ratio sits above both peer averages and the broader consumer finance industry, hinting that investors already pay a premium for its execution and growth story. If growth cools, how much of that premium could unwind?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own EZCORP Narrative

If this perspective does not fully align with your view, or you would rather dive into the numbers yourself, you can build a custom narrative in under three minutes, starting with Do it your way.

A great starting point for your EZCORP research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for your next smart move?

Before you move on, consider using the Simply Wall St screener to identify fresh opportunities that many investors still overlook.

- Explore smaller names with early momentum by scanning these 3577 penny stocks with strong financials that pair higher risk with improving fundamentals.

- Focus on technological change by targeting these 26 AI penny stocks that are linked to shifts in automation and data intelligence.

- Review these 15 dividend stocks with yields > 3% that aim to provide income through regular payouts alongside the potential for long term capital growth.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if EZCORP might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:EZPW

EZCORP

Provides pawn services in the United States, Mexixo, and Latin America.

Excellent balance sheet with proven track record.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

50 followersusers have followed this narrative

6 commentsusers have commented on this narrative

16 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$122.0% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$242.5% overvalued

10 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

MO

mo7md on ADNOC Gas ·

ADNOC Gas future shines with a 21.4% revenue surge

Fair Value:د.إ3.728.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

IN

IncomeAssets on Pulse Seismic ·

Watch Pulse Seismic Outperform with 13.6% Revenue Growth in the Coming Years

Fair Value:CA$4.4727.3% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VL

Vladislav on Galleon Gold ·

Significantly undervalued gold explorer in Timmins, finally getting traction

Fair Value:CA$481.5% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

116 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3927.2% undervalued

957 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

50 followersusers have followed this narrative

6 commentsusers have commented on this narrative

16 likesusers have liked this narrative