Advertisement

- United States

- /

- Capital Markets

- /

- NasdaqGS:ETOR

eToro (NasdaqGS:ETOR) Share Slide Prompts Fresh Look at Valuation

Simply Wall St

Reviewed by Kshitija Bhandaru

eToro Group (NasdaqGS:ETOR) shares have experienced notable volatility this past month, pulling back nearly 11% as broader market sentiment toward fintech names remains cautious. Investors are now weighing recent performance in addition to eToro’s ongoing profitability trends.

See our latest analysis for eToro Group.

ETORO’s share price return has slumped 42% year-to-date, reflecting how quickly sentiment can shift for fast-growing fintechs as investor risk appetite fades. While some recent swings have been sharp, the longer-term trend signals fading momentum despite continued sector buzz around digital finance.

If you’re thinking about your next move in a market that doesn’t stand still, this could be the right moment to broaden your search and discover fast growing stocks with high insider ownership

With shares down sharply and trading well below analyst price targets, investors must now ask: Is eToro Group undervalued, or has the market already factored in all of the company’s future growth prospects?

Price-to-Earnings of 17.2x: Is it justified?

eToro Group currently trades at a Price-to-Earnings (P/E) ratio of 17.2x, meaning investors are paying $17.20 for each $1 of the company's earnings. This figure is based on the last reported close of $38.55 per share alongside its recent earnings results.

The P/E ratio indicates how much the market is willing to pay for each dollar of profit generated. For eToro, the figure reflects expectations for continued profit growth relative to the earnings it recently reported, which is a key consideration in the tech-enabled capital markets sector.

With a P/E of 17.2x, eToro is valued as less expensive than the broader US Capital Markets industry average of 25.8x. This suggests that despite recent price declines, the market is not pricing in future growth for eToro as aggressively as it is for industry peers. This could signal potential opportunity for patient investors.

However, compared to its immediate peer group, eToro appears expensive, as the average peer P/E is just 6.1x. This significant difference highlights the market assigning a premium to eToro's recent earnings acceleration and its position as a growth-oriented fintech.

Result: Price-to-Earnings of 17.2x (ABOUT RIGHT)

See what the numbers say about this price — find out in our valuation breakdown.

However, sluggish revenue growth and eToro’s significant discount to analyst targets could challenge optimism if results continue to fall short of investor expectations.

Find out about the key risks to this eToro Group narrative.

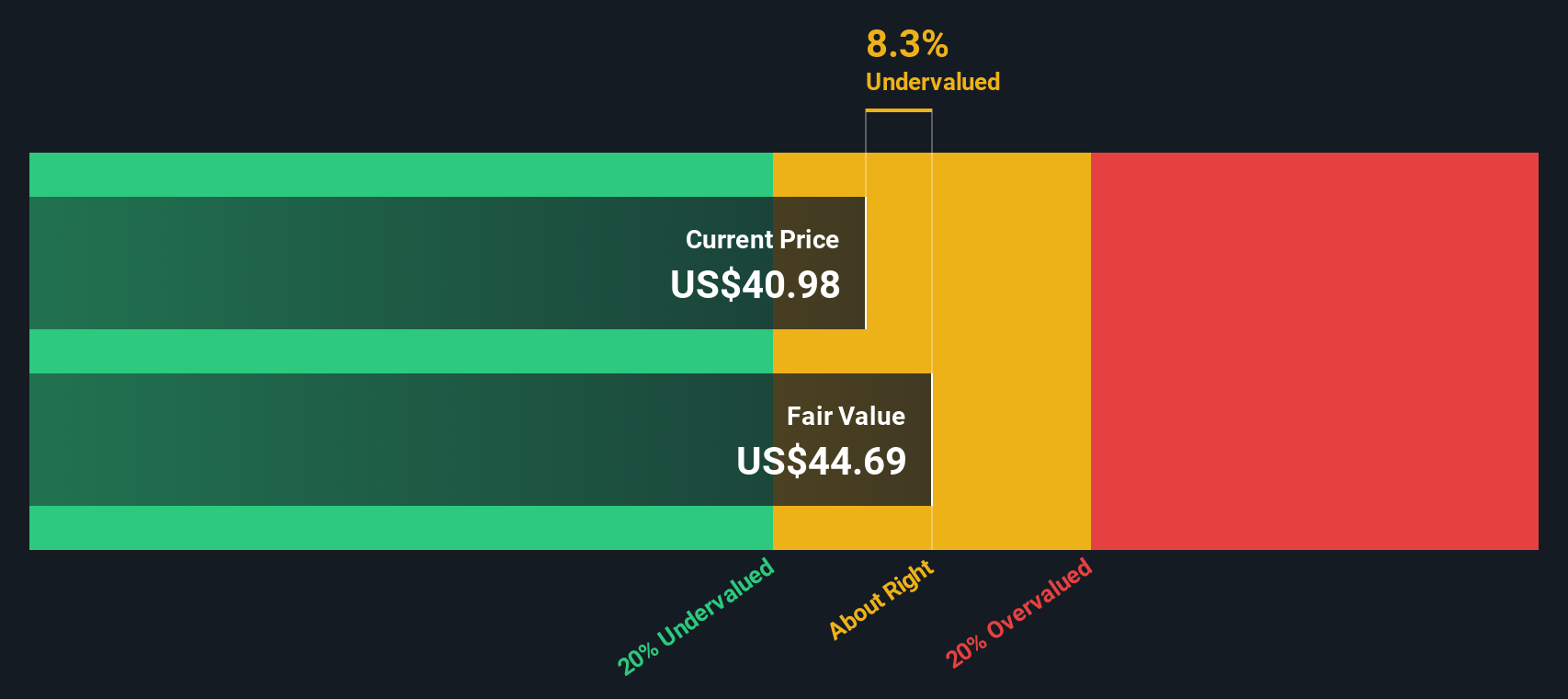

Another View: SWS DCF Model Suggests Undervaluation

Taking a different approach, our SWS DCF model estimates eToro's intrinsic value at $44.94 per share, which is about 14% higher than its current price. This method suggests eToro is undervalued at the moment. The question remains whether this gap will close as market conditions change.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out eToro Group for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own eToro Group Narrative

If you see things differently or want to explore the data firsthand, you can build your own perspective in just a few minutes. Do it your way.

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding eToro Group.

Ready for More Smart Investment Opportunities?

Bold moves start with powerful information. Don’t limit yourself to just one stock when there’s a world of fresh opportunities waiting. These handpicked lists can lead you to your next winning idea.

- Supercharge your returns and uncover attractive value with these 870 undervalued stocks based on cash flows for stocks trading below their fair value.

- Capture growth from innovation and check out these 24 AI penny stocks transforming industries with artificial intelligence breakthroughs.

- Enhance your passive income strategy by reviewing these 18 dividend stocks with yields > 3% featuring companies offering attractive yields above 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:ETOR

Flawless balance sheet with solid track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|13.6% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$89.00|23.6% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|40.6% undervalued

TR

Community Contributor