Advertisement

- United States

- /

- Hospitality

- /

- NYSE:SHCO

Analysts Are Updating Their Soho House & Co Inc. (NYSE:SHCO) Estimates After Its First-Quarter Results

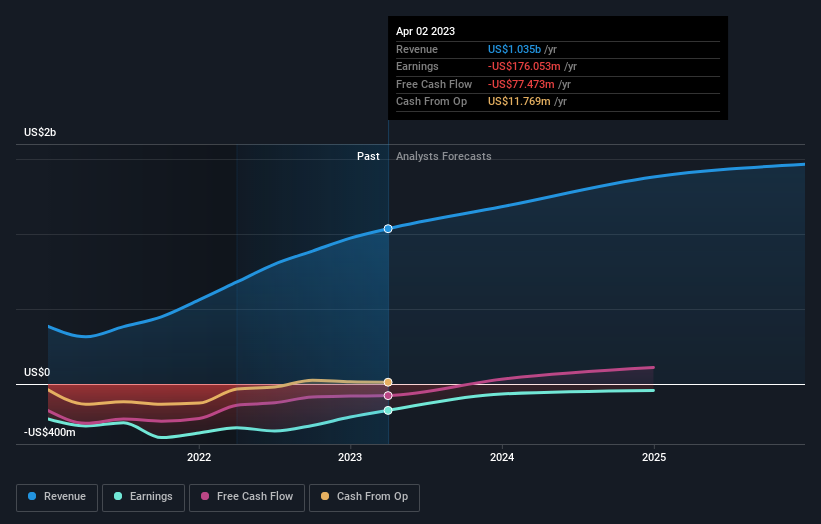

Last week, you might have seen that Soho House & Co Inc. (NYSE:SHCO) released its quarterly result to the market. The early response was not positive, with shares down 3.9% to US$6.93 in the past week. Results look to have been somewhat negative - revenue fell 2.1% short of analyst estimates at US$255m, although statutory losses were somewhat better. The per-share loss was US$0.08, 56% smaller than the analysts were expecting prior to the result. The analysts typically update their forecasts at each earnings report, and we can judge from their estimates whether their view of the company has changed or if there are any new concerns to be aware of. So we collected the latest post-earnings statutory consensus estimates to see what could be in store for next year.

View our latest analysis for Soho House & Co

Taking into account the latest results, the current consensus from Soho House & Co's seven analysts is for revenues of US$1.18b in 2023, which would reflect a solid 14% increase on its sales over the past 12 months. The loss per share is expected to greatly reduce in the near future, narrowing 53% to US$0.43. Before this latest report, the consensus had been expecting revenues of US$1.18b and US$0.45 per share in losses. So there seems to have been a moderate uplift in analyst sentiment with the latest consensus release, given the upgrade to loss per share forecasts for this year.

There's been no major changes to the consensus price target of US$8.25, suggesting that reduced loss estimates are not enough to have a long-term positive impact on the stock's valuation. The consensus price target is just an average of individual analyst targets, so - it could be handy to see how wide the range of underlying estimates is. The most optimistic Soho House & Co analyst has a price target of US$10.00 per share, while the most pessimistic values it at US$6.00. As you can see, analysts are not all in agreement on the stock's future, but the range of estimates is still reasonably narrow, which could suggest that the outcome is not totally unpredictable.

Looking at the bigger picture now, one of the ways we can make sense of these forecasts is to see how they measure up against both past performance and industry growth estimates. It's pretty clear that there is an expectation that Soho House & Co's revenue growth will slow down substantially, with revenues to the end of 2023 expected to display 19% growth on an annualised basis. This is compared to a historical growth rate of 53% over the past year. Juxtapose this against the other companies in the industry with analyst coverage, which are forecast to grow their revenues (in aggregate) 11% per year. So it's pretty clear that, while Soho House & Co's revenue growth is expected to slow, it's still expected to grow faster than the industry itself.

The Bottom Line

The most important thing to take away is that the analysts reconfirmed their loss per share estimates for next year. Fortunately, they also reconfirmed their revenue numbers, suggesting sales are tracking in line with expectations - and our data suggests that revenues are expected to grow faster than the wider industry. There was no real change to the consensus price target, suggesting that the intrinsic value of the business has not undergone any major changes with the latest estimates.

Following on from that line of thought, we think that the long-term prospects of the business are much more relevant than next year's earnings. We have estimates - from multiple Soho House & Co analysts - going out to 2025, and you can see them free on our platform here.

We don't want to rain on the parade too much, but we did also find 3 warning signs for Soho House & Co that you need to be mindful of.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:SHCO

Soho House & Co

Operates a global membership platform of physical and digital spaces that connects a group of members in the United Kingdom, the Americas, Europe, and internationally.

Good value with moderate growth potential.

Market Insights

Advertisement

Community Narratives

Kodiak AI - a potential 100 bagger opportunity?

Fair Value US$14.00|41.9% undervalued

DA

Community Contributor

A Fair Price for a Great Business Facing Real Threats

Fair Value US$383.06|14.1% undervalued

IM

Community Contributor

AXON And Shopify Integration Will Unlock Global Mobile Advertising

Fair Value US$613.59|1.3% undervalued

AN

Based on Analyst Price Targets