- United States

- /

- Hospitality

- /

- NYSE:QSR

Restaurant Brands International (NYSE:QSR) Reports Higher Sales, Lower Net Income; Dividends Affirmed

Reviewed by Simply Wall St

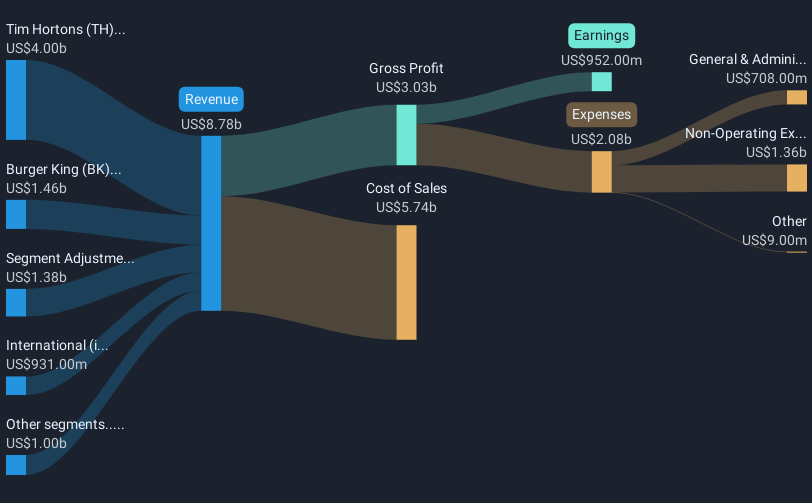

Restaurant Brands International (NYSE:QSR) recently reported a notable increase in sales and revenue for Q1 2025 but faced a decline in net income and earnings per share. Despite this mixed financial performance, the company confirmed a quarterly dividend. Over the past month, the stock surged 12%. This significant price movement aligns with broader market trends witnessing upward momentum, although it counterbalances concerns over economic fluctuations related to tariffs between the U.S. and China. The company's updates were likely influential in reinforcing shareholder confidence amidst mixed performances of market indices and ongoing tariff discussions.

Find companies with promising cash flow potential yet trading below their fair value.

While Restaurant Brands International's recent quarterly performance highlighted an increase in sales and revenue, its decline in net income and earnings per share could influence future revenue and earnings forecasts. The ongoing tariff discussions between the U.S. and China may pose further risks to profitability across its international operations. These geopolitical factors, combined with strategic moves like the acquisition of Carrols Restaurant Group and Popeyes China, could either mitigate or exacerbate revenue and margin fluctuations.

Over the past five years, the company's shares delivered a total return of 57.26%, reflecting a significant appreciation, including dividends, during this period. In comparison to the last year's performance, the company underperformed both the U.S. Hospitality industry, which returned 8.1%, and the broader U.S. market, which returned 8.2%. This longer-term view highlights the company's resilience and the value accumulated over time, despite last year's headwinds.

Furthermore, the recent 12% surge in the company's share price narrows the gap significantly compared to the consensus analyst price target of US$75.95. Currently trading at US$67.77, the stock still holds potential upside per the analyst estimates, highlighting investor optimism likely driven by expectations of enhanced digital capabilities and global expansion initiatives.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:QSR

Restaurant Brands International

Operates as a quick-service restaurant company in Canada, the United States, and internationally.

Undervalued established dividend payer.

Similar Companies

Market Insights

Community Narratives