Las Vegas Sands (LVS) stock has drawn increased attention lately, with its recent price movement sparking fresh conversation among investors. Many are now taking a closer look at what is driving interest in the company this month.

After a strong run-up this past month, Las Vegas Sands is starting to look like a stock with momentum on its side. The company’s 30-day share price return of 16.1% and year-to-date gain of 36.8% have outpaced many in the gaming and hospitality sector. A 1-year total shareholder return of 31.4% signals that both recent enthusiasm and long-term performance are turning heads among investors.

With such strong performance numbers on display, some investors are asking whether Las Vegas Sands shares still have room to run or if current prices already account for all that future growth. Could this be a genuine buying opportunity, or has the market already priced it in?

Advertisement

Most Popular Narrative: 4% Overvalued

With Las Vegas Sands closing at $68.25, the most widely tracked narrative fair value estimate comes in slightly lower at $65.38. This suggests minor overvaluation attributed to high recent performance. This context provides an opportunity to examine the rationale behind the narrative’s calculations and future projections.

The full opening and ramp-up of The Londoner in Macao, with its 2,405 rooms and suites, is expected to boost revenues and cash flows significantly as the property leverages its scale and quality in a competitive market. Marina Bay Sands in Singapore reported record EBITDA from high-value tourism and is expected to continue its growth trajectory supported by increased visitor capacity post-renovations, directly impacting revenue and EBITDA growth.

The real story focuses on bold expansion and profit forecasts that are uncommon in this sector. Do you know which financial pillars support this premium price? Explore the strategic bets and analyst assumptions that underpin the fair value, as these factors are shaping market sentiment.

However, ongoing volatility in Macau’s visitation figures and intensifying competition in the region could quickly change the outlook for Las Vegas Sands.

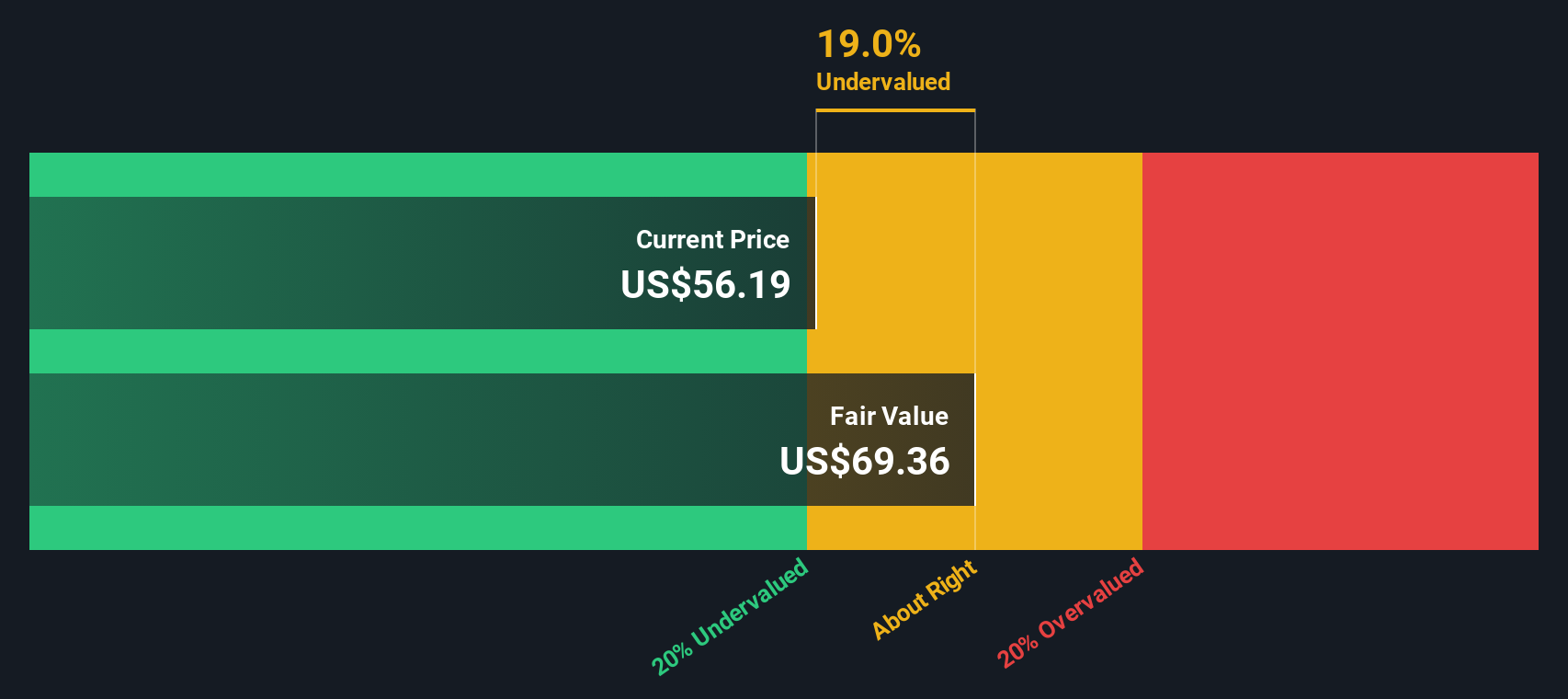

Looking beyond recent multiple-based valuations, our SWS DCF model presents a very different perspective. It estimates Las Vegas Sands’ fair value at $134.08 per share, which is nearly double the current market price. This suggests the stock may be significantly undervalued based on projected future cash flows. Could this model be highlighting an overlooked opportunity, or is it overly optimistic about future performance?

If you see the numbers differently or want to take a hands-on approach, you can easily craft your own narrative in just a few minutes. Do it your way

A great starting point for your Las Vegas Sands research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Don’t wait on the sidelines while smart investors jump on new trends. Let the Simply Wall Street Screener point you toward dynamic opportunities beyond the obvious picks.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield) • Undervalued Small Caps with Insider Buying • High growth Tech and AI Companies