- United States

- /

- Consumer Services

- /

- NYSE:HRB

Is H&R Block’s Recent 21% Slide Creating a Long Term Opportunity for Investors

Reviewed by Bailey Pemberton

- Wondering if H&R Block is quietly becoming a bargain, or if the market is signaling deeper issues with the business? This breakdown will help you decide whether HRB deserves a spot on your watchlist.

- The stock has slipped recently, down 2.4% over the last week, 12.5% over the past month, and 21.4% year to date. However, longer term holders are still sitting on gains of 9.2% over 3 years and 209.2% over 5 years.

- Some of this pullback reflects shifting sentiment around consumer services and tax-related names in a higher rate environment, with investors reassessing how resilient H&R Block's business model is outside of peak tax season. There has also been ongoing debate around the long term impact of digital tax solutions and regulatory changes on traditional preparers like H&R Block, which is feeding into the volatility.

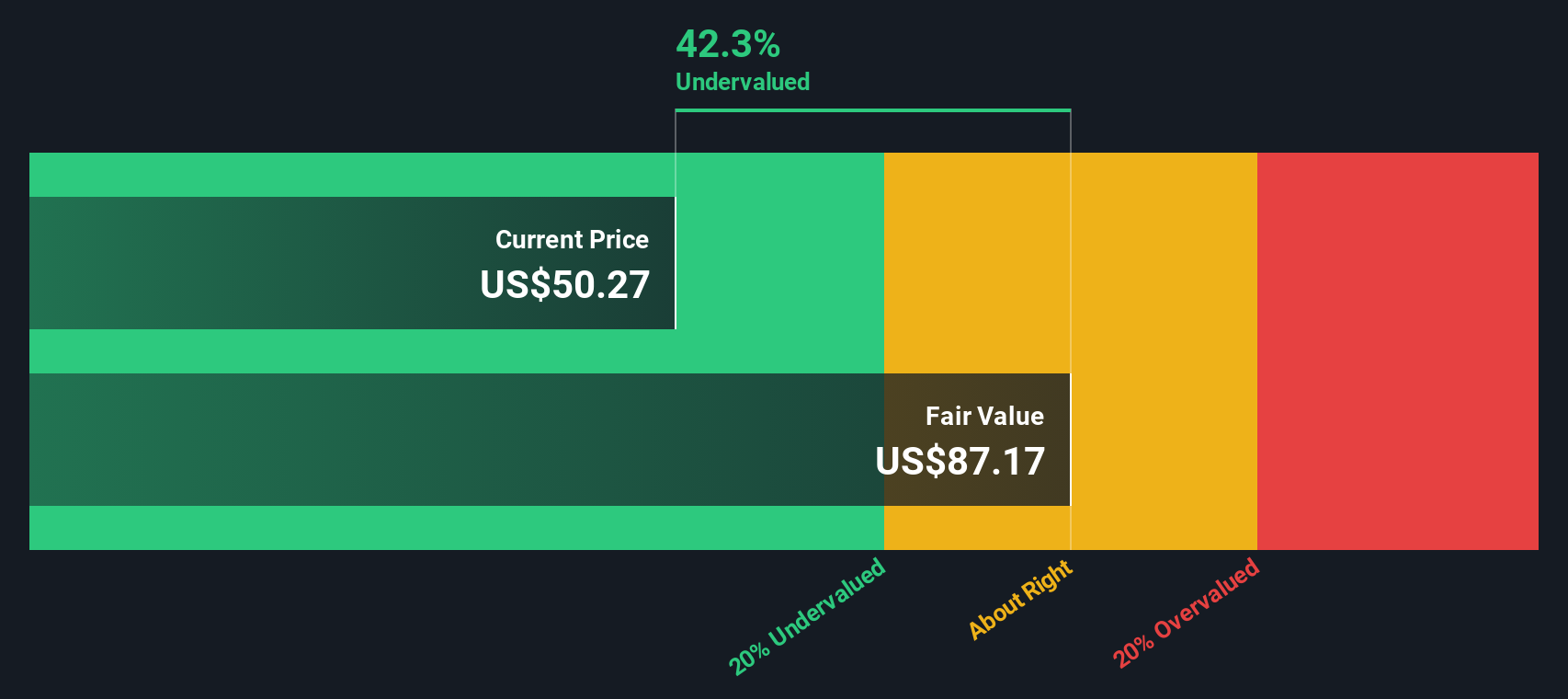

- Despite the recent weakness, H&R Block currently scores a solid 5/6 valuation score, indicating it screens as undervalued on most of our checks. Next, we will walk through the key valuation approaches behind that number, and then finish with a more holistic way to think about HRB's true worth beyond the usual metrics.

Find out why H&R Block's -23.6% return over the last year is lagging behind its peers.

Approach 1: H&R Block Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model estimates what a business is worth by projecting the cash it can generate in the future and then discounting those cash flows back into today’s dollars.

For H&R Block, the latest twelve month Free Cash Flow is about $579 million, rising to an expected $638 million in 2023. From there, Simply Wall St uses a two stage Free Cash Flow to Equity model, blending analyst estimates for the next few years with more gradual, extrapolated forecasts. By 2035, annual Free Cash Flow is projected to be roughly $570 million, with modest declines in the near term followed by low single digit growth.

When all these projected cash flows are discounted back, the model arrives at an intrinsic value of $75.37 per share. With the DCF implying the stock is trading at a 44.7% discount to this fair value estimate, H&R Block currently looks materially undervalued on cash flow fundamentals.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests H&R Block is undervalued by 44.7%. Track this in your watchlist or portfolio, or discover 907 more undervalued stocks based on cash flows.

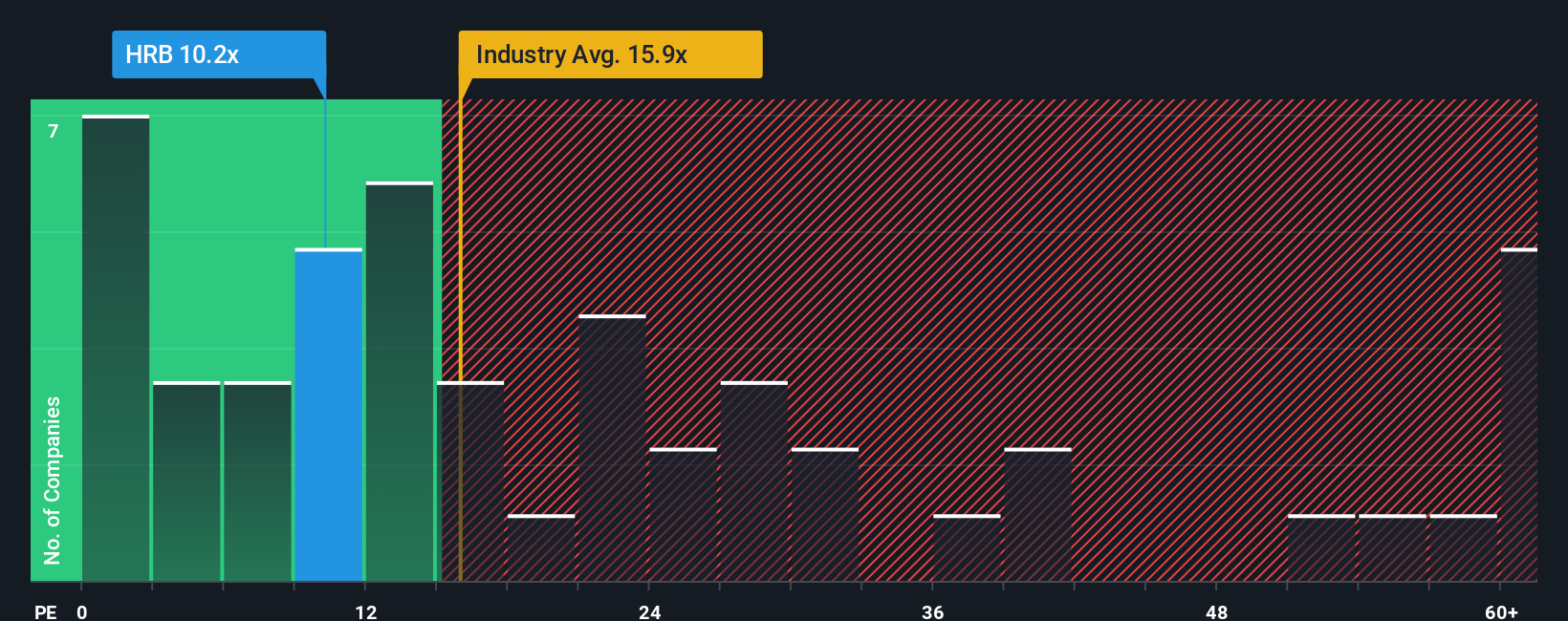

Approach 2: H&R Block Price vs Earnings

For consistently profitable companies like H&R Block, the Price to Earnings (PE) ratio is a straightforward way to judge value, because it directly links what investors pay today to the profits the business is generating right now.

What counts as a normal or fair PE depends on how fast earnings are expected to grow and how risky those earnings are. Higher growth and lower perceived risk generally justify a higher PE, while slower growth or more uncertainty usually push it lower.

H&R Block currently trades on a PE of about 8.6x, a steep discount to both the Consumer Services industry average of roughly 16.1x and the broader peer group average of around 16.1x. Simply Wall St also calculates a proprietary Fair Ratio of 16.4x, which reflects what investors might reasonably pay for HRB given its earnings growth outlook, margins, industry, size and risk profile.

This Fair Ratio is more tailored than a simple peer or industry comparison, because it adjusts for company specific strengths and weaknesses rather than assuming all Consumer Services stocks deserve the same multiple. Comparing HRB’s current 8.6x PE to the 16.4x Fair Ratio suggests the market is pricing the stock well below what its fundamentals warrant.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1446 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your H&R Block Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, a simple way to attach a clear story and set of assumptions to the numbers behind a company’s fair value, including your expectations for future revenue, earnings and margins.

A Narrative links what you believe about a business, for example how tax complexity, digital adoption or small business services will evolve for H&R Block, to a concrete financial forecast and then to an estimated fair value per share.

On Simply Wall St, Narratives live on the Community page and are designed to be easy to create and compare. They can help investors think about whether their Fair Value sits above or below today’s market price.

Narratives are also dynamic, automatically updating when fresh information such as earnings releases, guidance changes or major news arrives. This can help keep your valuation view aligned with the latest available data instead of going stale.

For example, one H&R Block Narrative might lean bullish and see fair value closer to $62 based on steady revenue growth and resilient margins, while a more cautious view might anchor around $48. Comparing those to the current price can help clarify which story you find more convincing.

Do you think there's more to the story for H&R Block? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if H&R Block might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:HRB

H&R Block

Through its subsidiaries, provides assisted and do-it-yourself (DIY) tax return preparation services in the United States, Canada, and Australia.

Undervalued established dividend payer.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

Deep Value Multi Bagger Opportunity

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Trending Discussion