Advertisement

- United States

- /

- Hospitality

- /

- NYSE:EAT

Brinker International (EAT) Is Up 10.3% After Chili's Drives Standout Sales and Reaffirmed Guidance

Simply Wall St

Reviewed by Sasha Jovanovic

- Brinker International reported robust first quarter results, with CEO Kevin Hochman citing Chili's as a primary source of industry-leading sales and traffic growth despite ongoing macroeconomic challenges.

- This strong performance was matched by the company’s reaffirmed revenue guidance for fiscal 2026, underlining continued confidence in operational improvements and brand strength.

- We'll examine how Chili's standout sales growth and the company's confident outlook could influence Brinker International's future investment narrative.

This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

Brinker International Investment Narrative Recap

To be a Brinker International shareholder today, you need to believe in the company's ability to drive superior traffic and sales at Chili's while navigating industry-wide pressures like shifting consumer preferences and rising labor expenses. The recent surge in sales and traffic is a strong short-term catalyst, yet the accelerating move toward off-premise dining remains an ongoing risk. The upbeat earnings don't fundamentally alter this near-term risk profile, although they may provide some reassurance around operational execution.

The company's reaffirmed revenue guidance for fiscal 2026 is especially relevant, signaling leadership’s confidence in the durability of recent momentum. For investors, this continued commitment to revenue targets offers context for evaluating the consistency of Brinker’s performance against key industry headwinds and potential catalysts like digital and menu innovation.

However, before getting too comfortable with the sales momentum, consider that ongoing labor inflation, a challenge across hospitality, could still weigh heavily on future operating margins and that’s something investors should fully understand...

Read the full narrative on Brinker International (it's free!)

Brinker International's narrative projects $6.2 billion in revenue and $562.8 million in earnings by 2028. This requires 4.7% yearly revenue growth and a $179.7 million earnings increase from current earnings of $383.1 million.

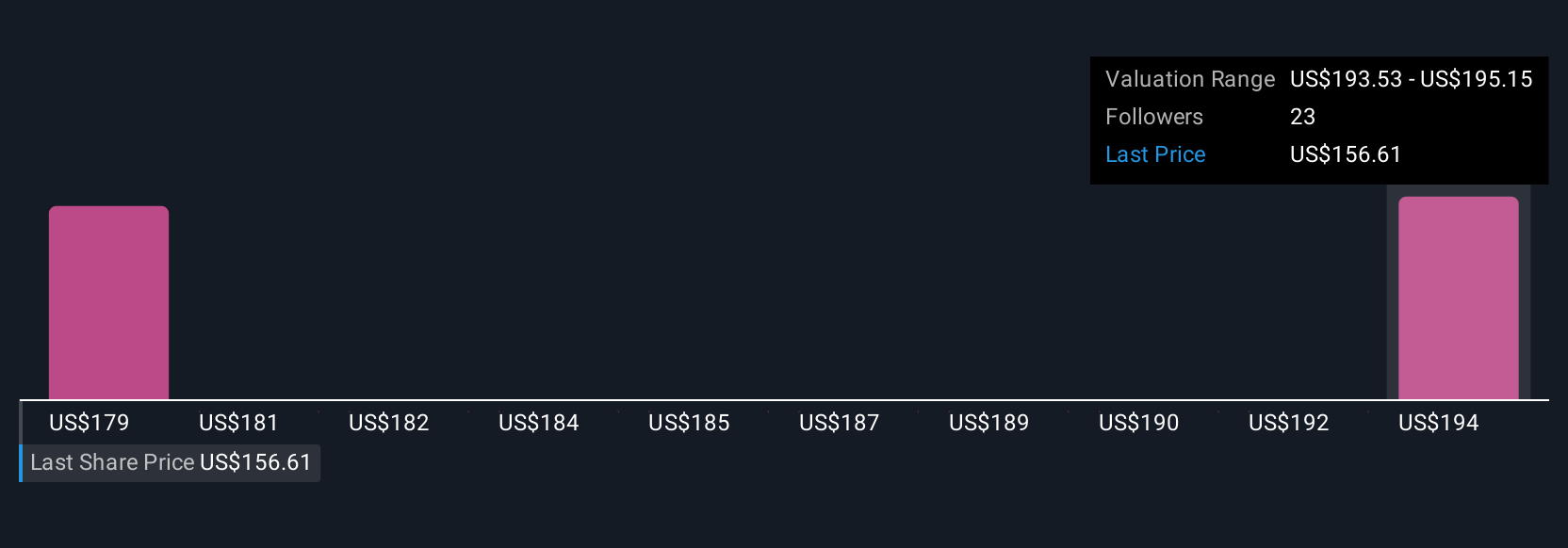

Uncover how Brinker International's forecasts yield a $159.41 fair value, a 41% upside to its current price.

Exploring Other Perspectives

Simply Wall St Community members estimate Brinker International’s fair value between US$159.41 and US$192.14, based on two independent models. While many focus on strong sales growth as a driver, you should also weigh ongoing risks like persistent labor cost pressures, since community outlooks can diverge sharply on what shapes future performance.

Explore 2 other fair value estimates on Brinker International - why the stock might be worth just $159.41!

Build Your Own Brinker International Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Brinker International research is our analysis highlighting 5 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Brinker International research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Brinker International's overall financial health at a glance.

Searching For A Fresh Perspective?

Our top stock finds are flying under the radar-for now. Get in early:

- Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Brinker International might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:EAT

Brinker International

Owns, develops, operates, and franchises casual dining restaurants in the United States and internationally.

Very undervalued with solid track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor